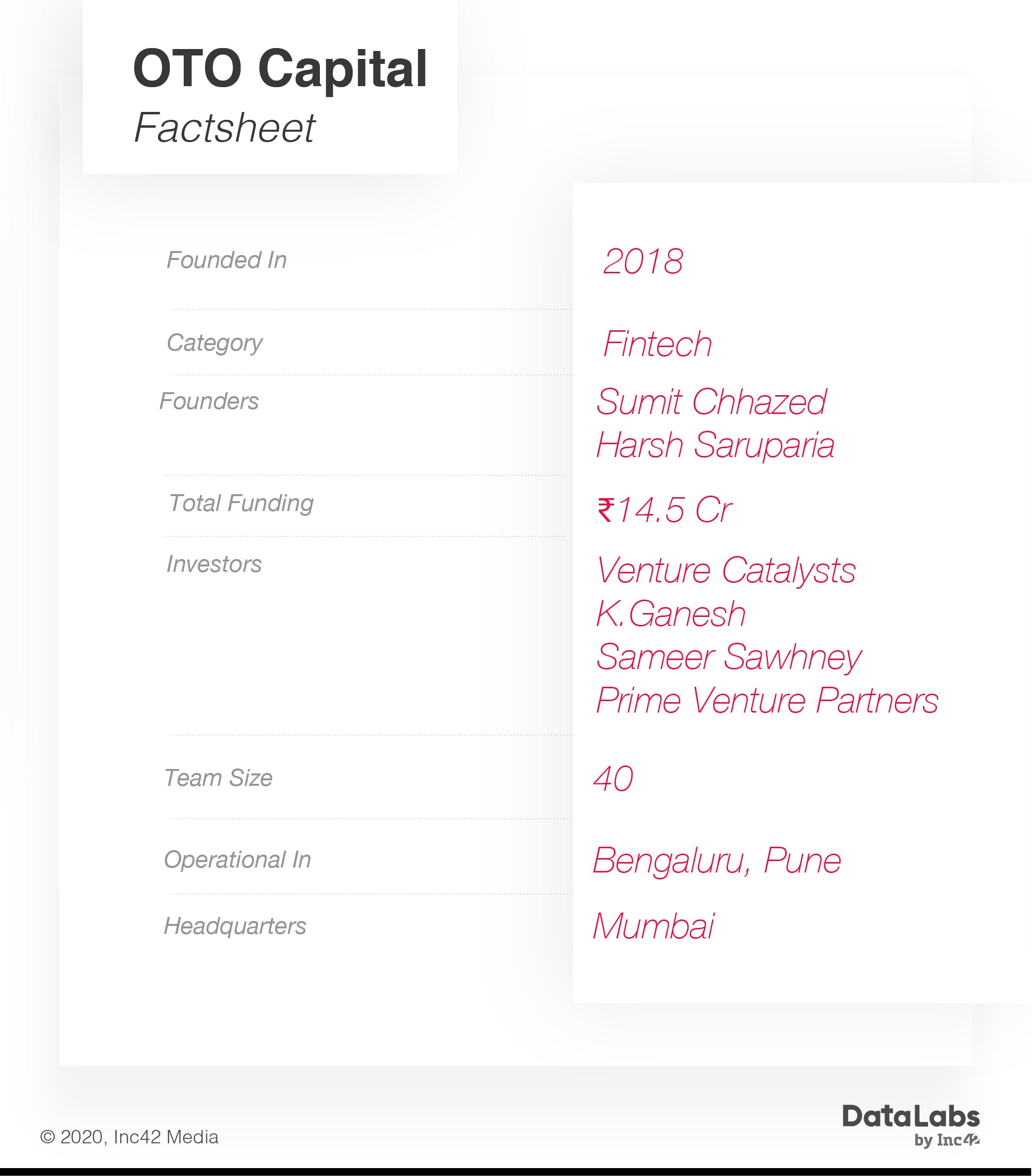

Vehicle leasing startup OTO Capital was founded in 2018 by Sumit Chhazed and Harsh Saruparia

The automobile financing company is introducing leasing and deferred ownership as an alternative for bank loans

The company is targetting 1000+ monthly transactions by mid-2020

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

Every year in India, more than 3.25 Mn new cars and 20 Mn new two-wheelers are sold, of which more than 60% are financed or bought on loans. Yet, loan processes are tedious and not exactly consumer-friendly.

While financing organisations claim paperless and digitised processes, anyone who has bought or sold cars knows the reality of lengthy paperwork involving multiple documentation and the back-and-forth with many agencies. Vehicle loans typically take 3-5 days to be approved. But what if there was a way to get new cars/bikes without paying the full amount and without taking a loan? Mumbai-based OTO Capital says vehicle leasing is that alternative.

OTO, apart from the obvious reference to “auto”, also stands for ‘Owning Together’. Offering an alternative model to bank financing for vehicle ownership in India, OTO has introduced an option to take two-wheelers or four-wheelers on leases, in association with partner banks.

Although, there are older companies that provide this kind of financing model, only for four-wheelers and that too only to corporates and none of them is operating in the two-wheeler segment and there’s no focus on individual consumers.

From his own experience of dealing with two-wheeler buyers at his previous startup CredR, OTO cofounder and CEO Sumit Chhazed realised that the consumer mindset has now changed where more and more consumers are opting for finance and upgrading their vehicles much faster — almost every three years compared to every five years for older generations.

There’s a great need to solve the hassle of applying for finance for this audience, take responsibility to maintain the vehicle and put the effort of resale each time by themselves.

“Most of the car and bike buyers are in the age group of 21-35 who are young, progressive and aspirational. They believe in owning what they desire and not what they can afford along with the minimum commitment. The main problem we are trying to solve is the unavailability of flexible and affordable ownership models for the Indian auto consumer,” Chhazed told Inc42.

How Does Vehicle Leasing Work?

OTO’s instant-approval model allows customers to choose the desired vehicle from the partnered showrooms. At present, OTO Capital’s primary focus is on two-wheelers and it has partners such as Hero, Bajaj, Honda, Yamaha, Suzuki, TVS, Royal Enfield among others.

OTO’s proprietary algorithms generate a true score basis various personal and income parameters of the applicants which helps in instant approval. The team has also digitised the complete journey for the customer from inquiry to application and agreement closure. All this requires zero paperwork, OTO claims.

Buyers can make a down payment of INR 5000 and sign up for all-inclusive EMI offers that include vehicle insurance and maintenance costs. At the end of the chosen tenure, users have the flexibility to walk away with no obligation, or lease a brand new bike or make a simple balloon payment to retain the same bike. In case, a user wants to reduce the tenure, they can do so by paying a nominal prepayment penalty fee.

The process is similar for leasing four-wheelers, with the exception of the down payment amount, which varies for category and size.

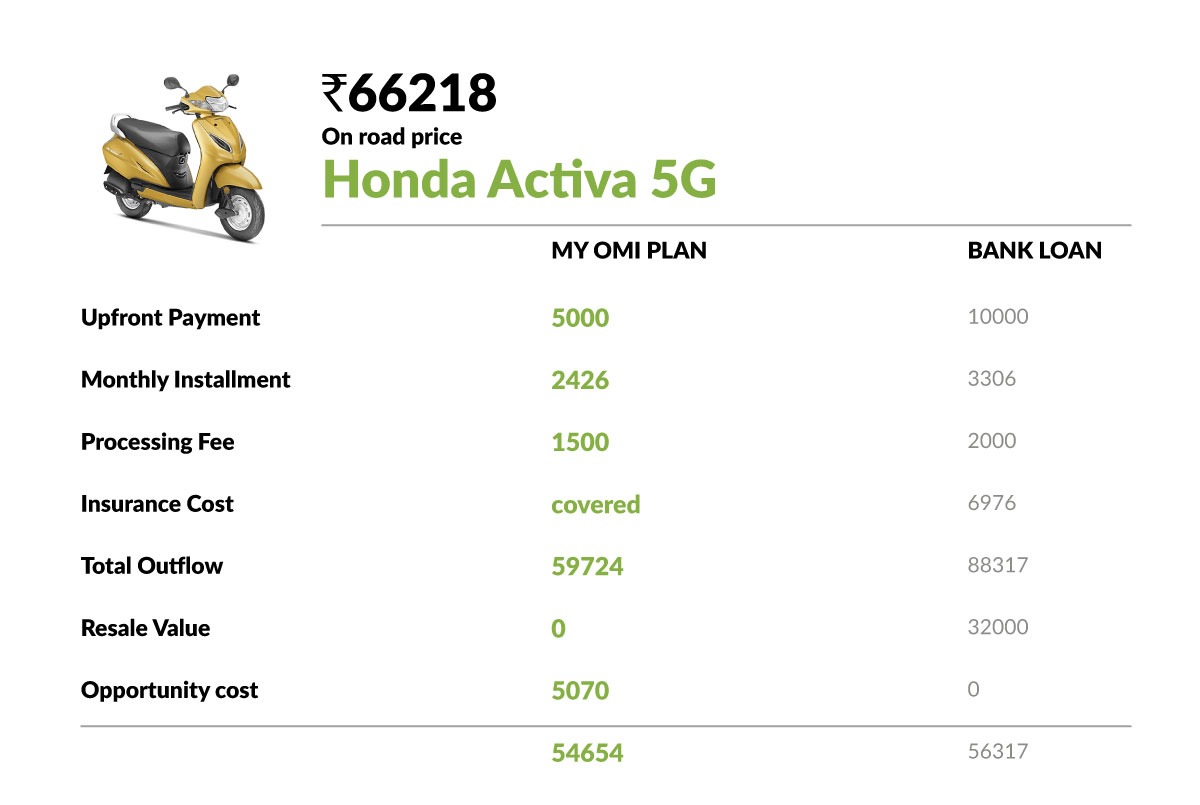

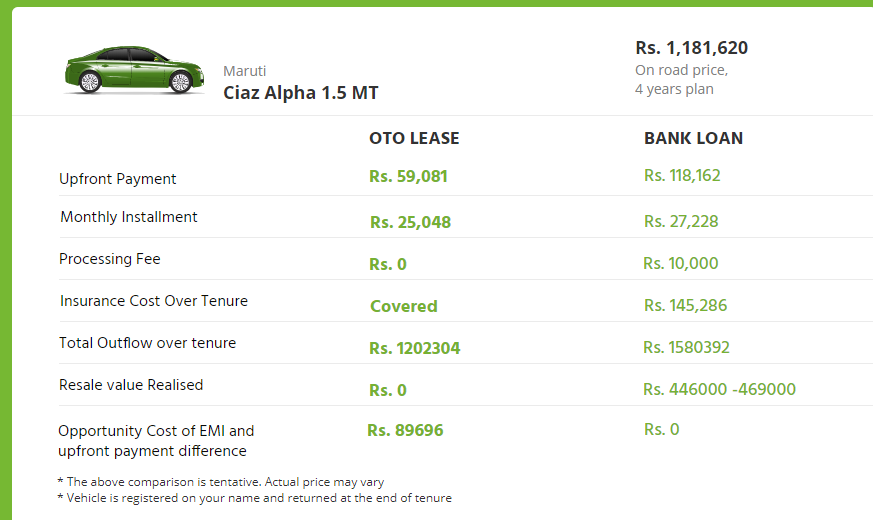

Here’s a breakup of the instalments and how far vehicle leasing deviates from a typical bank loan on a yearly basis.

The vehicles are issued in the owner’s name and are returned to OTO after the selected tenure of 1-3 years. This allows the user to avoid paying EMIs on complete asset value as in the case of conventional loans from banks and other financing institutions.

The monthly OMI (OTO monthly instalment) payments are also flexible and can be personalised as per the monthly budget of the user. The company further claims a 30-minute loan approval, up to 30% lower monthly cost and assurance of a vehicle change within 1-3 years.

Hurdling The Bumps In The Growth Path

At CredR, Chhazed worked closely with the second-hand two-wheeler market. However, there were new challenges with OTO, as he was working on a completely new product.

“The concept of automotive leasing or flexible financing was not known to most vehicle buyers or dealers when we started. We had to visit many dealerships and showrooms to introduce our product to them. We need to speak to customers, understand their concern and reiterate our product pitch for the first 50 customers multiple times,” he said.

Talking about competition from traditional lenders, Chhazed called them “stone-age financing options” hinting at how OTO is differentiating through tech.

But he is right about calling them serious competition. According to a November 2018 Money Control report, NBFCs have up to 40% share in the two-wheeler financing market. Finance arms of companies like Bajaj Auto (Bajaj Finance), Hero Motocorp (Hero Fincorp), and TVS Motor Company are pulling in significant sales for their companies. In the banking space, HDFC is the primary player owning the majority market share in two-wheeler financing space.

OTO Capital is now planning to focus on penetrating deeper in the Indian market for the next 18 months and create its dominance in 10 cities. The company claims to be adding 150+ new customers monthly now and aiming to achieve 1000+ monthly transactions by mid-2020. It also claims to have disbursed vehicles finances worth $2 Mn till now.

Chhazed said the target in the future is to focus on spreading awareness about individual vehicle leasing options in the market to gain customers organically.

“In the West, auto leasing is the first option that is given to all buyers while in India it has been still limited to larger corporations and its employees. Customers in India are not aware of such options hence educating the consumers is really important.”

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.