Imagine buying a financial product becoming as simple as buying a sachet of shampoo. Sounds too simple when you think of the current complexities involved in understanding and buying a financial instrument? But, if last mile utilities such as the shampoo sachet can be made easily accessible to all, can’t the same thing be done to create a last mile utility in finance? Is it possible to dumb down financial products, create a trusted last mile utility, as well as provide universal access to it?

It might have sounded like a far-fetched idea years ago but with democratization of technology, the idea of a last mile utility is very much feasible. And that’s what exactly the Bharosa Club aims to do. Founded by Sanjay Bhargava, Anita Bhargava, and Prakash Pai, the Delhi-based Bharosa Club takes inspiration from kirana stores for the idea of a shared utility for financial products. The platform built on an easy to use, high technology framework, will address the issue of financial literacy and offer customers easy access to financial products such as Mutual Funds, Term Insurance and Loans. By cutting down on the middlemen, and selling these utilities on a no-commission basis & providing unbiased advice, the club wants to be a game changer in potentially empowering millions of households by providing universal financial access.

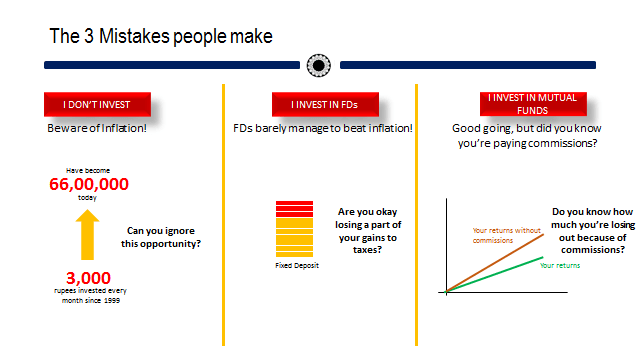

Says Sanjay, “Customer unfamiliarity, relative absence of unbiased advice, high commission structures and systemic inefficiencies in the distribution mechanics have collectively resulted in the current under penetration. As a result, an entire generation has lost out on a great wealth creation opportunity in the last 15 years – by not investing in mutual funds. By choosing to invest in FDs, they have lost out on the enormous benefits of investing in equity. Through the club, we want to bring households and businesses on the same platform, reduce costs and middlemen, eradicate poverty, and make billions by serving millions.”

Bhargava’s confidence about providing universal financial access to all stems from his experience in the industry. He was on the founding team of X.com, that later went on to become PayPal. After leaving Paypal, he started the Universal Financial Access (UFA) movement in India with the goal of securing financial inclusion for all Indians, followed by cofounding the IIC Fellowship with the University of Chicago. He was also the Co-Founder & Chairman of Eko India Financial Services which again focussed on financial inclusion.

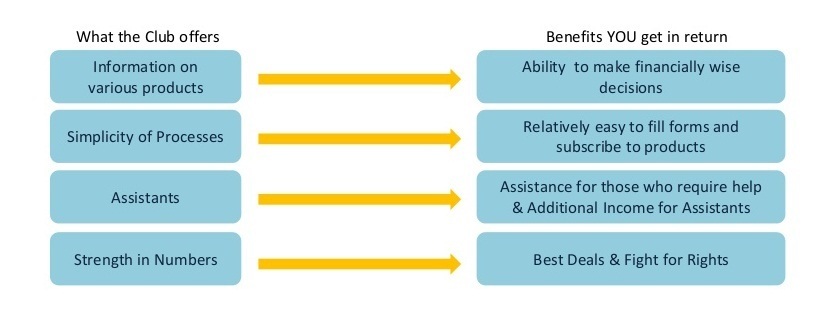

In order to address the problem of financial inclusion for all and eradicate poverty, Bhargava founded the Bharosa Club with the aim of dramatically increasing the penetration of high quality financial products in India. Bharosa Club will follow a regular club format, where members will have access to high quality products across domains. These will be augmented with access to customized products and member only deals.

How It Works

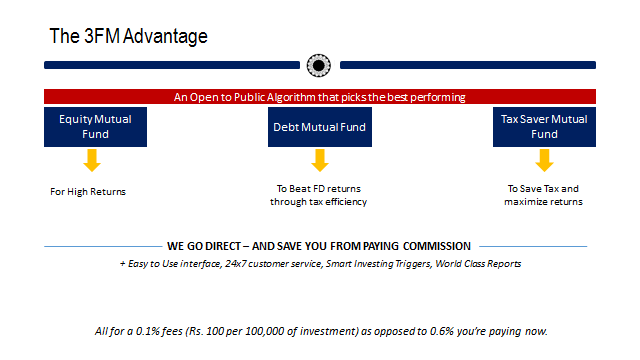

Both households and businesses can become members of the club. The members will need to pay a small convenience fee to the club but need not pay for any marketing costs. Poor households can start their subscription with as low as $0.3 (INR 20) per month, median ones with $0.75(INR 50), and the well-to-do ones with $1.5 (INR 100). Similarly businesses would pay amounts starting from $180 (INR12K) for a small business and moving on to $900 (INR60K ) for a large business. In order to simplify the process of investing in mutual funds, the club offers a 3 Fund Model, or 3FM. or The Club’s algorithm picks the best performing fund in each of the three categories – Equity Mutual Funds, Debt Funds and Tax Saver Funds. These become the recommended picks for those interested in investing in 3FM.

A relatively less known fact is that every Mutual Fund scheme has two distinct avatars – Regular and Direct. An investor who invests via an intermediary – a banking or trading platform or an advisor, automatically gets assigned the Regular Avatar. And an investor who invests directly with the fund house is assigned the Direct Avatar. The difference lies in expenses. Every fund pays a commission to an intermediary or the fund advisor for getting them business, and this gets factored into the price of a fund purchased through the regular route. The fund house doesn’t have to pay a commission to anyone for an investor who invests direct, and hence the direct avatar doesn’t need to factor in those costs. This difference causes a vast difference in returns over time.

It is these marketing costs the Bharosa Club aims to mitigate by tying up with MFs to increase penetration and offer commission-free selling to its customers. The Club makes its customers invest only in the “Direct Plans” of mutual funds in order to save them between 0.6%-1.0% commission in Equity Funds and 0.1%-0.4% in the case of Debt Funds. Additionally, since there is no broker or commissions involved, there is no one else who stands to gain from the customer’s investment. While the club will make only one recommendation per category, investors are free to invest in as many funds as they like through the Bharosa Club platform.

The Club has its own proprietary algorithm for selecting funds that incorporates data driven analysis. While it monitors funds on a daily basis, it reviews the fund recommendations every three months. By the first quarter of 2016, the club intends to make its algorithm public – in the larger interest of transparency. At this stage, the club is only running a setup for those interested in getting started by investing in Bharosa Club’s 3FM picks with transactions in other funds to follow soon.

Target Market

Bhargava believes that the target market is universal as the club aims to bring financial freedom and security to all and sundry, be it a poor household or a conglomerate in India. The club aims to create a community of like-minded people bound together by their desire to improve their well-being.

Monetisation, Funding, And Traction

The Club will charge a one-time fee of $1.5 (INR 100) and a convenience fee of just 0.1% annually once a customer’s investments cross $1.5K (INR100, 000). Adds Sanjay, “We are not doing it for the money. Our motto is to make billions by serving millions. Also the constitution of the club strictly lays down that you cannot charge commissions.”

The Club, started earlier this year in June, is bootstrapped. Founders have personally invested over $301k (INR 2 Cr). With its motto of providing universal financial access, it aims to target about 100 Mn households and 1 Mn businesses by 2020. Initially, for the year ending December 2015, it aims to bring about 1 Mn households under its fold.

Competitive Landscape

The democratization of technology and rise of smartphones have also led to evolution of startups that are trying to make investment a simpler process for customers. For instance, App and web based investment management platform, Tavaga, which enables retail investors to access technology, processes, and advice and investment products by providing a personalised, innovative technology interface between the two. It is targeting the age group of 25 to 35 year olds by gamifying the process of risk assessment and investment decision-making. The startup is currently testing the first release of its product, and has customers who have committed assets of over $767K (INR 5 Cr) for management. The product is expected to be launched in December and Tavaga has raised an undisclosed amount in seed-round from angels through TracxnSyndicate.

Similarly, there is Bangalore-based Scripbox, an online mutual funds investment platform which by employing principles of portfolio theory and behavioral finance, recommends the right portfolio of mutual funds and an easy one-click method of investing in them. Scripbox also aims to simplify investing by eliminating the confusion created by many choices. In August this year, it raised about $2.5 Mn in Series A round of funding led by existing investor Accel Partners.

Then there are other online trading platforms such as RKSV and Zerodha which have been gaining traction. Competition in this space is likely to increase on account of the fact that market regulator Securities and Exchange Board of India (Sebi) is in the last lap of finalising guidelines for the sale of mutual funds on ecommerce platforms. This would allow Flipkart, Snapdeal and a host of other online marketplaces to sell financial products which have so far been the domain of brokers and banks.

As of now the Club is offering the 3FM which it plans to augment with more funds. Later it aims to add products such as term insurance and loans and in the range of 8-15% depending on the income class of the household.

Editor’s Note

Bharosa Club stands out with its unique philosophy and motto of empowering households by providing universal financial access to all. The differentiating factor here is that unlike other startups, its focuses significantly on making the benefits of equity investing available to even the lowest of income groups. Another differentiating feature is that mandates are an important feature of Bharosa Club. If one is uncomfortable transacting for a variety of reasons such as lack of internet access or discomfort with using technology, one can nominate upto 3 trusted individuals who can hold one’s mandate, and will be permitted to transact on the individual’s behalf. The idea is to make the benefits of investment possible to everyone. The real test will be to gather this audience, and to provide effective recommendations to the same. It will be interesting to note how Bharosa Club wins the trust of its target audience in these aspects.