Encrypted social media platforms have fuelled the money mule pandemic by allowing users to exchange information with little accountability

Social media has provided fraudsters with the tools they need to commit fraud on devastating scales

We can stop money mule activity even before it starts, only when there is an extra augmented layer of protection to traditional identity verification methods

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

Social media has allowed the global village to shrink. In a country like India, where every third person has a smartphone, social media adoption rates are globally the highest. On Facebook, India boasts a user base of nearly 387 Mn people; Instagram has 362 Mn users and 462 Mn YouTube users.

Global commentators are often quick to assign rural India a biased reputation of poverty, illiteracy, and helplessness. Anybody who has done some fieldwork would know just how warped that perception is. 50% of these social media users come from rural areas, reflecting significant digital engagement and technological advancement across the country.

The highly rapid inclusion of the Indian population into using these platforms has had a two-fold effect. On one side, social media has allowed for a more democratic dissemination of information. Some information has been lifesaving, such as guidelines on public health, digital public goods, government alerts, and more.

But the other side of social media is where fraudsters thrive. These platforms offer you the luxury of anonymity – and that is all a fraudster needs. This pervasion of social media into people’s daily lives has also actively allowed the erosion of previously sacred elements like “privacy.”

Social Media: A Haven For Fraudsters

With unregulated use of social media and limited awareness of the lurking dangers, users often overshare on their social streams. It’s easy for fraudsters to scrape personal data from public profiles or just literally find it disclosed on certain social profiles.

This data is sold to bad actors who use it to create synthetic data, conduct account takeovers of unaware victims, or directly use it to open multiple accounts. These accounts that have been hacked or taken over are called ‘money mules’ because of their role in money laundering and terror financing.

Encrypted social media platforms have fuelled the money mule pandemic by allowing users to exchange information with little accountability. For example, Telegram’s policies of voluntary anonymity in chats have made it a fraudster’s haven, and considering 55% of India’s internet users have a Telegram account, identifying fraud rings on it is a never-ending cat-and-mouse chase.

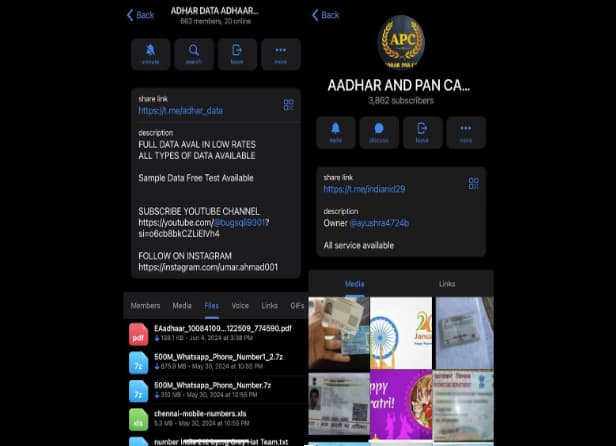

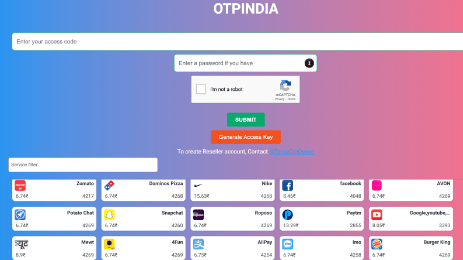

Some screenshots show how scraped/stolen PII data is sold over a social media platform in bulk.

There are platforms like these where you can inject OTPs to conduct account takeovers for a mere ₹7-₹10. That’s the cheap value of an identity today.

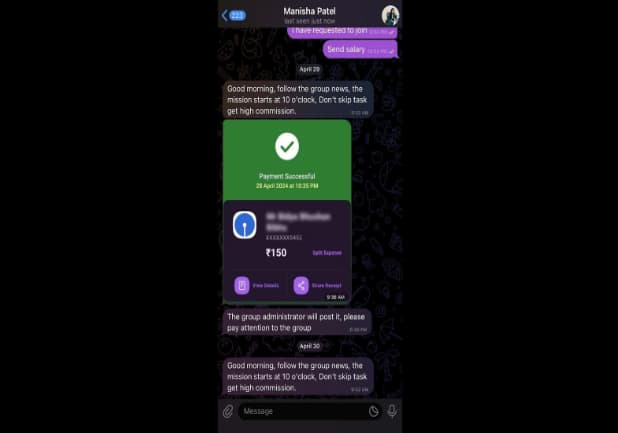

You must have received texts from “job recruiters” who offer money in exchange for minor tasks. Other common fraud types seen are a ‘love interest’ extorting money, citing emergencies or blackmailing.

All these are pig butchering scams where the fraudsters build a relationship with the victim, create enough trust for the victim to increase the amount of money they invest gradually, and eventually disappear leaving the victim behind with massive losses.

Cyber Hubs For Money Mule Recruitment

Most of these frauds have been traced back to cyber fraud hubs operating mainly from India’s hinterland. After Jamtara gained a reputation as a global phishing centre, we hear stories of upcoming fraud centres nationwide. How are these able to sprout up with such industrial vigour?

For instance, on paper, the villages of Jurehera and Ghamdi in Rajasthan’s Bharatpur district have an average daily income of INR 368. But what’s interesting is not on paper. Deep within their fields, you will find small concrete structures fully equipped with electricity, phones and other devices. Individuals from this village have been running sophisticated fraud scams targeting individuals nationwide, bringing their earnings up to between INR 1,000 and INR 1 Lakh on any given day.

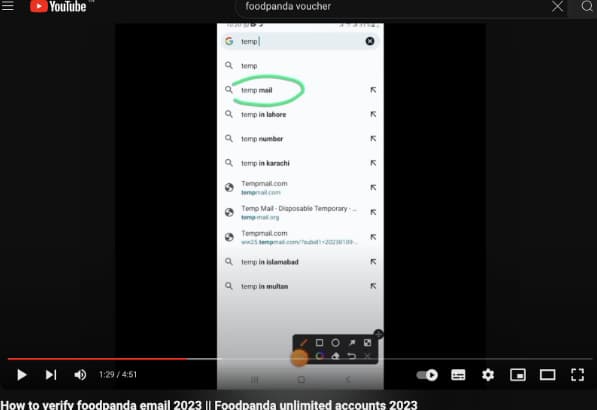

The motivation for the rural youth turning to fraud is easy enough to understand – easy money. Social media has provided these willing individuals with the tools they need to commit fraud on devastating scales. YouTube is flooded with videos that teach you how to use stolen data to hack accounts, create fake accounts, or conduct mass promotion abuses.

Who Is Accountable?

Social media platforms cannot and should not shirk away from the heavy burden on their shoulders. While social media platform spokespeople try to build confidence in their content regulation methods, data privacy laws and other necessary barriers for user protection, some gaps need to be addressed urgently.

If content with derogatory language and hate speech is flagged, how does sensitive private information about individuals get circulated so easily?

Historically, social media giants have shown an intent towards user protection, but let’s be practical here. These fraud rings thrive not just because of social media but because of an intricate web of actors operating locally, nationally, and globally.

Since identity thefts have become effortless, money mule victims must be protected at the financial extraction stage.

Most banks and fintech tackle the money mule and, consequently money laundering issue during transaction monitoring. But, that is a reactive model that seeks to get the money back once it has passed through the system.

As experts in fraud prevention and identity decisions, we have seen the most powerful results when we can stop money mule activity even before it starts. That can only happen when there is an extra augmented layer of protection to traditional identity verification methods. So, stop before losses, not after.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.