Prime Venture Partners explains the reasoning behind its recent OTO investment

Car leasing has fixed monthly payments and no lumpsum payments for insurance or maintenance

OTO has crossed more than 150 cars under its programme

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

More than 20 years ago, I finally decided to graduate from the $1000 student car I had bought in Seattle, to a brand new car. And yes, it was one of those memorable moments in life. As I walked into the Nissan showroom in San Jose to buy that stunning looking black Nissan 240SX, the dealer asked me, “Sir, would you want to buy it, finance it or lease it?” I didn’t have the money to buy it but I asked the question,

“What’s the difference between financing and leasing”?

“About $150 (INR 10,000) per month,” was his smug response before he explained how it worked.

“Young man,” he said, “Of course, you could buy this car today or take a loan, but why would you? Over the next few years, car models will rapidly change, your affordability will increase and your tastes and needs will evolve. Instead of paying such a high EMI, pay 2⁄3rd of that amount, enjoy the same car for the next 3-5 years”

And at the end of it he left me with three options:

- I could still buy the car by paying out the residual value

- I could trade it in and lease or buy a new car

- I could walk away from it and not have ANY obligation

It seemed too good to be true! While I liked the concept, almost nobody I knew had leased a car. But the math simply made sense to me. I just couldn’t see why it wasn’t a good deal. After all, I still had all the options but I delayed my decision to actually buy the car and at that stage in my life, the $150/month I saved was very significant. As it turned out, I really enjoyed the car and had a very lucky stint with it, so for emotional reasons, at the end of the four years, I paid out the residual value and bought the car.

Eventually, I sold the Nissan before I moved back to India in 2003. When I started to look for cars to buy in India, I simply couldn’t find the option of leasing and was forced to “buy” all my cars thereafter. Yes, there was some way I could potentially do it through my employer but it was too complicated to do so.

I was therefore thrilled to meet Sumit and Harsh, serial entrepreneurs with an incredible passion for “all things auto”. They had been working on car leasing for retail consumers and albeit early in the journey, the road ahead was clearly exciting.

As a first-hand beneficiary of this kind of a program, I was already convinced of its value. Add to it the fact that the average age in India is 28, and many of the working class are just starting to get to be able to afford their first new car! Despite the recent downturn in the industry that is much talked about, as I dug in, I realised that new car sales have been growing even outside the metros and the option to lease versus buy makes a lot of sense for a lot of buyers. These days, people rarely keep their first car for longer periods and a three-five year lease makes a lot of sense.

Most people first buy the car they can and not the car they want!

As I spent more time with Sumit, I realised that OTO Capital has really improved the process to make it not just affordable, but also quick with their 30-minute approval process. It is a super high-tech, ongoing experience and extremely convenient in all regards. Not only does one end up with a much smaller EMI (about a 30% lower amount) but it includes bumper-to-bumper comprehensive insurance as well as a regular maintenance program with authorised service centres — a true white-glove service for car buyers. And it still has the flexibility that allows users to buy the car or walk away from it with zero obligation at the end of the lease period!

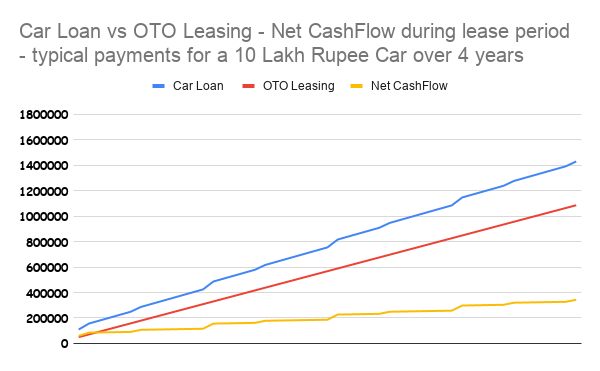

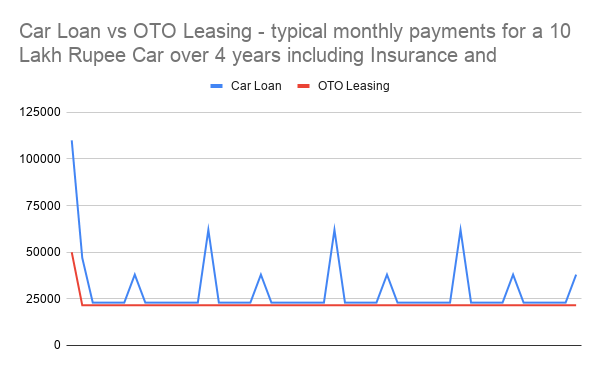

The graphs above and below illustrate typical cash flow made it a compelling value proposition, even if one doesn’t take into account any potential tax savings. As you can see from the graphs, car leasing offers a lower down payment, fixed monthly payments and no lumpy payments for insurance or maintenance. The net cash flow also is so much better over the four-year period that even simple bank-based recurring deposit investment for the delta means that one comes out ahead even if one were to pay the INR 4 Lakh at the end of the fourth year. Over and above that the idea that one could walk away from the car and not have to worry about resale etc. makes it a no-brainer.

OTO has been growing nicely and has crossed more than 150 cars under its programme. By partnering with banks and NBFCs, the OTO team has ensured that they have infinitely large access to capital and can rapidly expand the service around the country and to various sectors. The company aims to grow 10X rapidly from here. The beauty of their model is a partnership approach which is a win-win for all. Banks can now diversify their car financing business by partnering with OTO and bringing in car leasing to their portfolio, without having to worry about maintenance, insurance and eventual resale of cars at the end of the lease.

From a consumer perspective, it’s not that the car is cheaper; at a macro-level, it will cost you about the same if you decide to keep it and make a balloon payment. Most importantly it will give you the option to make that decision later on, at virtually no incremental cost.

While all this sounds simple, we all know that the devil is in the details and the team at OTO has worked very hard to bring consumers a delightfully simple experience. Auto Sales in India have struggled in recent quarters and although it’s early days, OTO can change the fortunes of the industry in a material way.

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.