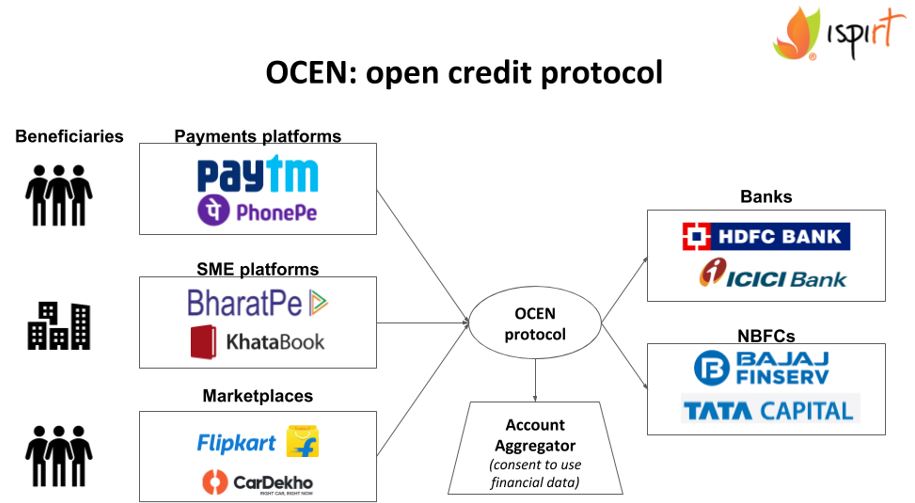

On July 25, iSPIRIT announced Open Credit Enablement Network (OCEN )

India has all the “building blocks” for open financial protocols

OCEN, on the other hand, operates as a layer of APIs that standardise the loan disbursal, monitoring and collection process.

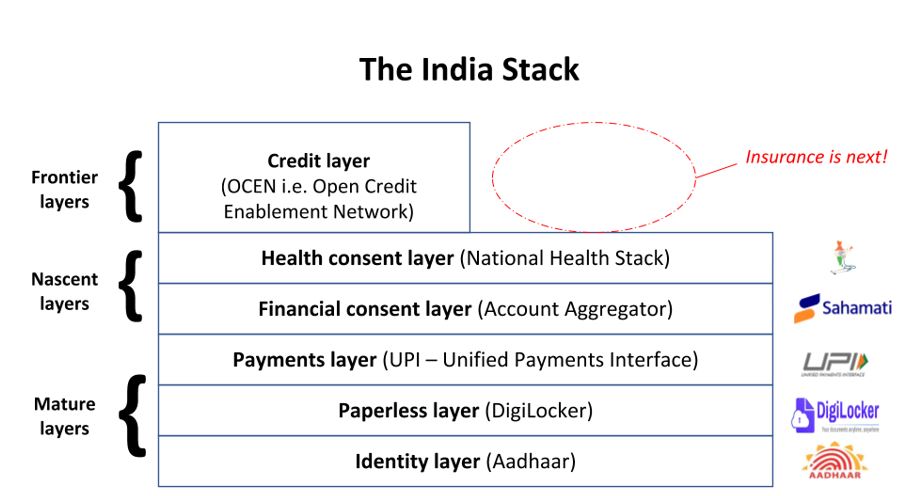

The India Stack has been a work-in-progress since 2009 when UIDAI (the Aadhaar issuing authority) was founded. Aadhaar was the foundation for successive “layers” of the India Stack to built.

The Initial Focus Was On The “Less” Layer:

- Aadhaar: Presence-less layer

- DigiLocker: Paperless layer

- UPI: Cashless layer

In anticipation of adoption of the Personal Data Protection (PDP) bill being passed, volunteers at iSPIRIT began work on a privacy-first framework called DEPA (Data Empowerment & Protection Architecture).

As a framework, DEPA formed the bedrock for two important consumer use-cases:

- Consensual sharing of financial information (via the Account Aggregator framework)

- Consensual sharing of health information (via the National Health Stack)

However, sharing financial information is a “tool” and not a “product” – on July 25, iSPIRIT announced OCEN (Open Credit Enablement Network) i.e. “UPI for credit” – an open protocol that acts as the “single API/integration for credit”.

OCEN Draws Upon:

- The Account Aggregator framework – to access financial customer data for:

- Loan underwriting (decision to lend)

- Loan monitoring (pre-emptive diagnosis of future NPAs to take corrective action)

- End-use control (i.e. ensuring funds disbursed are used for the stated purpose)

- The LSP framework

- LSP stands for Loan Service Provider – a new class of entities focused on origination of loans on behalf of NBFCs and banks who offer the risk capital for lending.

- LSP was a recommendation in the UK Sinha MSME report to the RBI

Therefore, India has all the “building blocks” for open financial protocols. Credit now has its open protocol via OCEN – is insurance next?

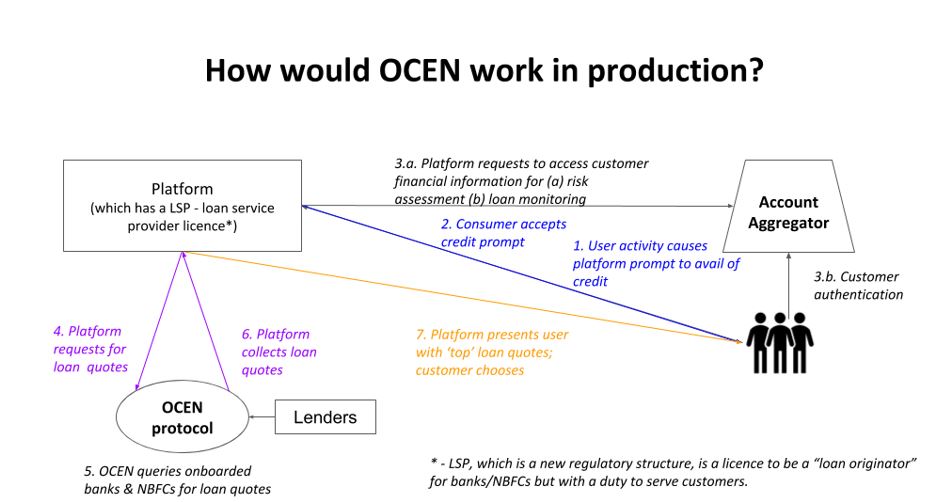

Before we jump into the ‘UPI for Insurance’ – OPEN (Open Protection Enablement Network), it is important to review how OCEN is expected to operate to understand how OPEN & OCEN are likely to be very similar.

OCEN operates as a layer of APIs (Application Programming Interfaces) that standardize the loan disbursal, monitoring and collection process.

Let’s Walk Through The Loan Origination Process Enabled By OCEN:

- You select your new sunglasses from Lenskart (who has the LSP license).

- When you arrive at the checkout screen, you have an opportunity to avail of a consumer loan. You select “Yes”.

- You’re redirected to your Account Aggregator login and you give consent to Lenskart to query your ICICI bank account for

- Details on your income/payments/assets etc (one-time)

- Occasional access to assess your financial position (loan monitoring; optional)

- Lenskart takes details regarding (a) Your financial position & (b) your purchase; these details get posted to the OCEN protocol.

- 17 banks respond with loan quotes i.e. interest rate and loan covenants (repayment structure, default criteria etc)

- Lenskart collects these quotes & applies its discretion in showing you the top choices.

- You make your choice (or don’t and just pay upfront!)

If you choose to pay your loan up midway through its lifetime, you have the opportunity to revoke your consent to let Lenskart monitor your financial statement too!

For further information on OCEN; do check out the iSPIRIT blog. This brings us to the insurance analogue to OCEN – OPEN (which is at the idea stage).

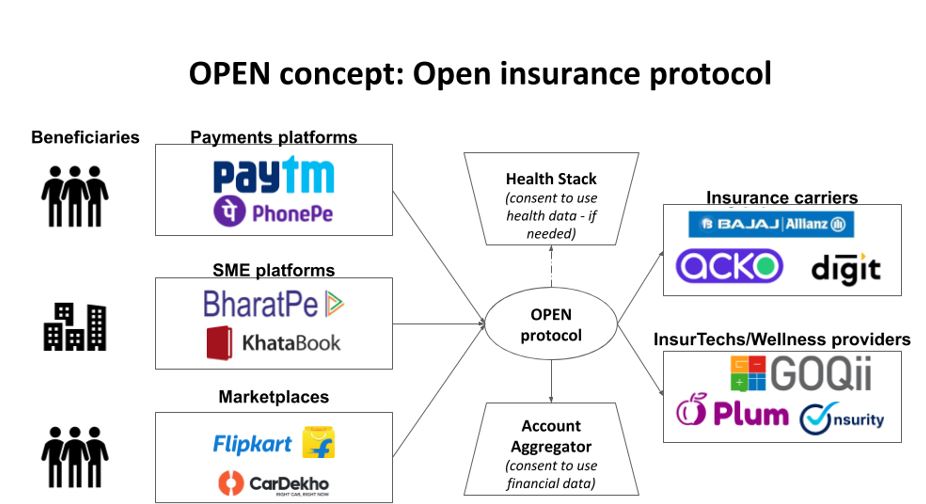

OPEN would operate as a layer of APIs to standardise the insurance underwriting, distribution & claims process. For technology platforms and consumer-facing apps, OPEN would act as a “single API for insurance distribution.”

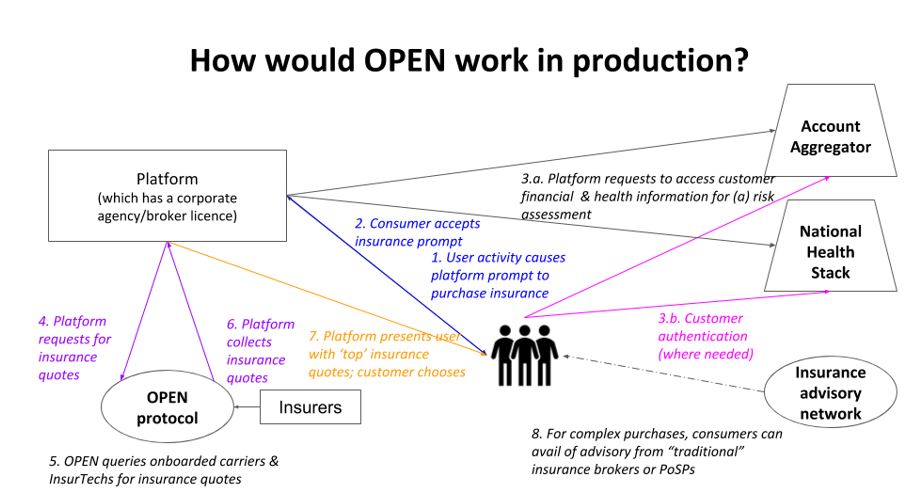

Let’s Walk Through The Insurance Sales Process Enabled By OPEN:

- You decide to book a trip to Maldives on Yaatra.com (who has a corporate agency licence to sell insurance).

- When you arrive at the checkout screen, you have an opportunity to avail of Overseas Medical cover for your trip; you say “Yes”

- You’re redirected to a Consent Manager login & you give consent to Yaara.com’s insurance partner to query Apollo Hospitals for your medical records.

- Your trip and medical details are posted to OPEN to collect insurance quotes regarding:

- Premium payment (& structure)

- Policy benefits, exclusions and value-add services 12 insurers respond with insurance quotes

- Yaatra.com collects these quotes & applies its discretion in showing you the top choices.

- You make your choice (or choose not to buy!)

- If you want, you can get advice on your policy purchase from a qualified individual (e.g. insurance broker)

Matters such as claims handling and mid-term adjustment of policies are yet to be fleshed out.

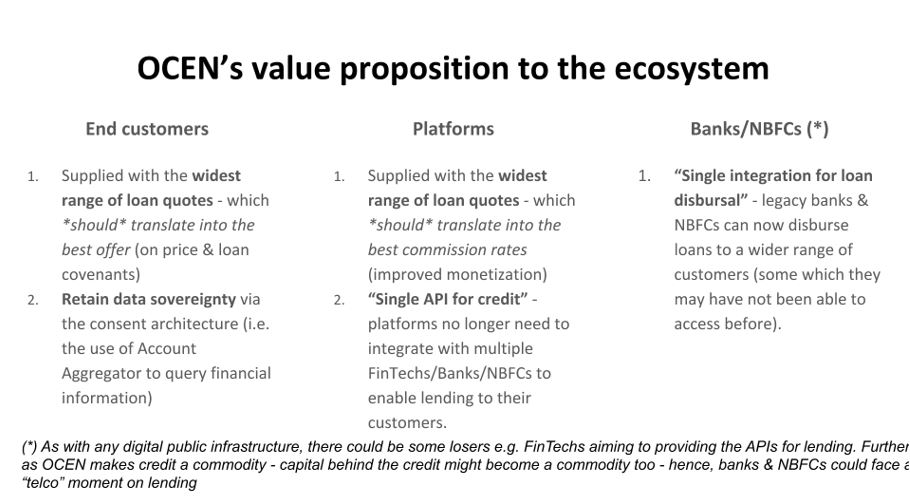

Benefits of OPEN For The Ecosystem:

For Insurance Companies

- Distribution arrangements typically occur via group products often involve a high degree of opacity on membership composition; leveraging the India stack can lead to a “fairer” pricing structure via:

- Viewing PEDs of members (via the National Health Stack)

- Viewing financial position of members (via Account Aggregator)

- Access to new sources of distribution (technology companies can tap into different audience pools)

For Distributors (Or Platforms)

- No new regulatory structure is required since the existing corporate agency license is sufficient.

- Access to the best commission rates by originating business for a broad range of carriers (no partner lock-in)

For Customers

- Better product selection (tailored to their needs)

- Best price

On The Health Side Of Insurance, iSPIRIT Has Been Working On:

- The National Health Stack (which includes an electronic claims switch)

- The Gamifier policy (a new kind of outcomes-based health insurance policy)

It is likely that the combination of the Health Stack and Account Aggregator will enable a version of OPEN for health insurance in India in the coming years.