In 2018, I started exploring the possibility of floating an early-stage fund focussed on India

The target raise for the fund was set at $100 Mn

My advice to emerging managers would be to hold at least 3 closes, if not more, for their first fund

I hope you are all keeping safe and healthy in these strange times. The last couple of months have given us a lot to introspect on. If anything the Covid19 pandemic has taught us that no nation, institution or individual is immune to failure. But together we can pull through this with renewed spirits and profound strengths.

In my case, this lockdown has allowed me time to write about a failure I’d been meaning to share for a while. My career in venture capital started in 2012 with a short spell at Startup Leadership Program where I led marketing and admissions for four of its chapters. This was my first exposure to the startup ecosystem — till then I didn’t know what an investment pitch deck looked like.

A chance encounter then led to an investment role with Unilazer Ventures, the PE arm of the family office of Ronnie Screwvaala. During my time at the firm, I was fortunate to get involved in investments like Lenskart, Zivame, Maroosh, Dogspot among others. While I didn’t lead these investments, I did learn a lot about investing and venture building which prepared me well for my next role – investing for Accel.

During the three year spell at Accel, I co-led the fund’s investments in Swiggy, Agrostar, HolidayME and Bicycle.AI (predecessor to AppSmith) among others. I was also given the opportunity to work with the fund’s broader portfolio companies.

Over the years, I have had the good fortune of meeting and working alongside some of the brightest & smartest entrepreneurs in the ecosystem — Sriharsha, Nandan, Rishabh, Vijay, Abhishek, Karan, Geet, Shardul,, Sitanshu, Anjana, Adarssh, Vaibhav — among many others. My time in the ecosystem has also helped me forge meaningful relationships with some of the most cordial fellow co-investors. For that, I feel immensely grateful.

After moving out of Accel, I felt a strong urge to build something ground up. It was outside my comfort zone but I guess working with so many fantastic entrepreneurs can have that effect on you.

So in 2018, as a young investment professional with less than half a decade of investment experience under his belt, I started exploring the possibility of floating an early-stage fund focussed on India. This is a summary of my fundraising journey and the learnings acquired in the process. I hope it helps those going through a similar stage in their professional lives.

Some context about the fund :

Investment Strategy

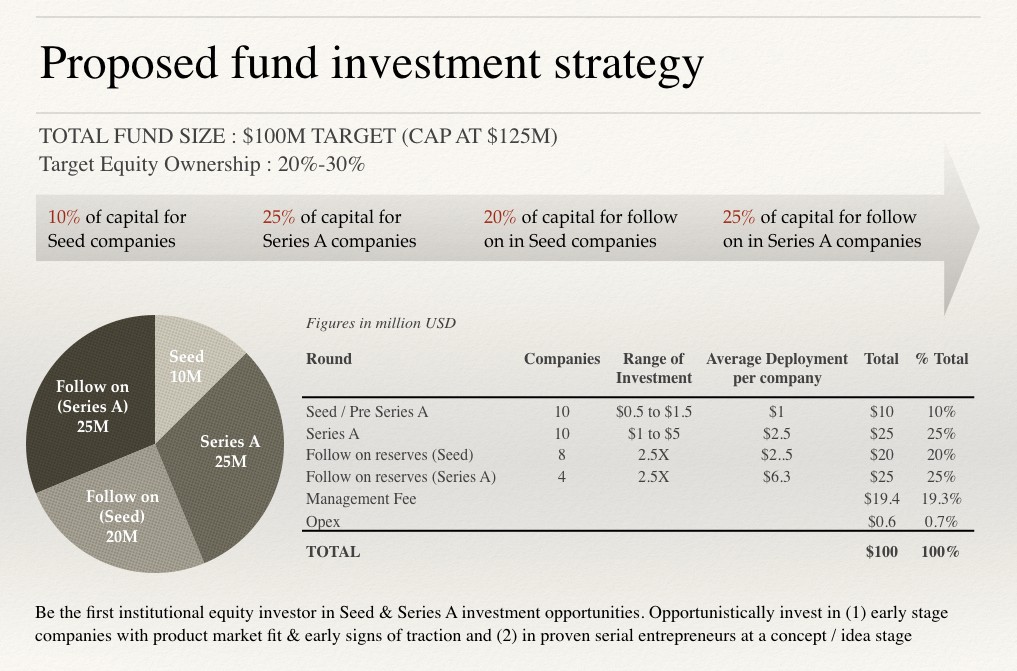

Fund Size: The target raise for the fund was set at $100 Mn with provision for another $25 Mn. under the greenshoe option.

Fund Strategy: To invest in 18–20 Seed, Pre-Series A and Series A consumer tech, tech-enabled and direct to consumer brand startups in exchange for target ownership of 20%-30%.

Ticket Size: The ticket size for Seed investments was between $500K and $1.5Mn. with an average deployment of $1Mn and for Series A investments was between $1Mn. and $5Mn. with an average deployment of $2.5Mn.

Follow-on Reserves: A healthy follow-on reserves ratio of 2.5X was allocated for the winners in the portfolio. One of the biggest learnings for the VC firms operating in India over the last decade has been that the consumer businesses in India, even the scalable tech ones, have longer exit cycles and are far more capital intensive than their global peers.

Therefore, it is not only important to spot an opportunity early but also to have significant dry powder (reserve capital) for doubling and tripling down on the winners. While the exit cycles have been reducing significantly lately, I assumed a modest average liquidation period of 7 years in the modelling.

Investment Thesis

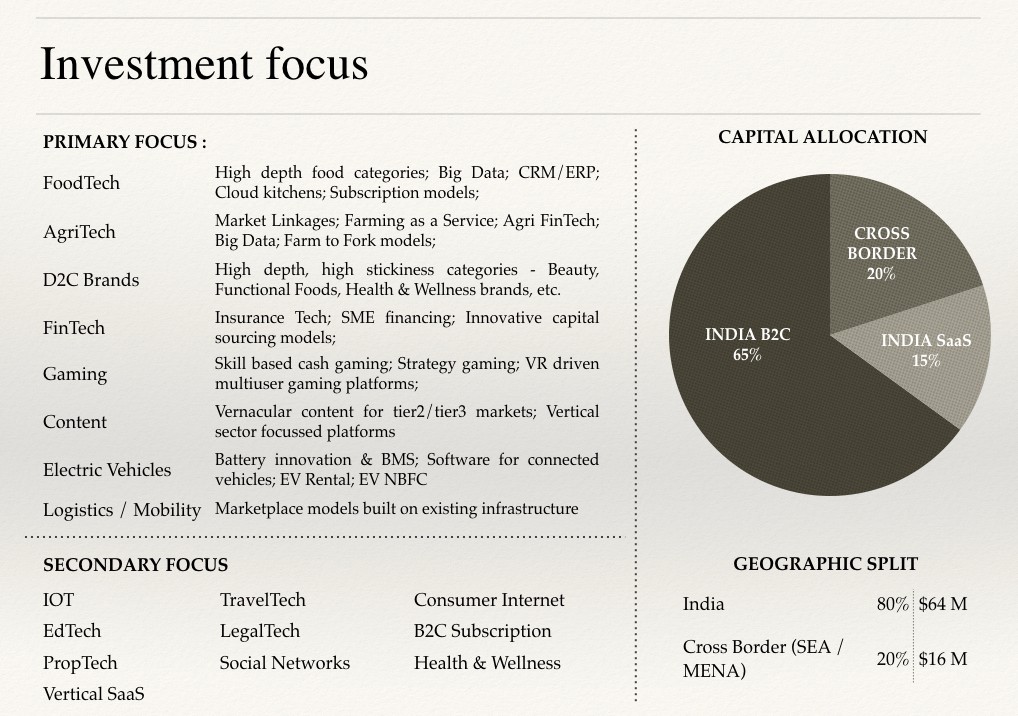

I am a strong advocate for picking a Generalist thesis over a Domain-specific thesis for emerging managers unless the manager has a couple of decades of domain expertise. As such, my investment thesis was fairly diverse under the broad Consumer theme. For brevity sake, I have only shared the introductory slide of the thesis here. Each of the focus sectors had an underlying thesis with an associated deal pipeline. I might write a separate blog to shed light on the same at a later point.

Portfolio Construction & VC Modelling

I have published a simplified version of the entire model here. Will make a template out of this later for readers to use. Also, shared a few model screenshots at the end of the post.

Proposed Fund Terms

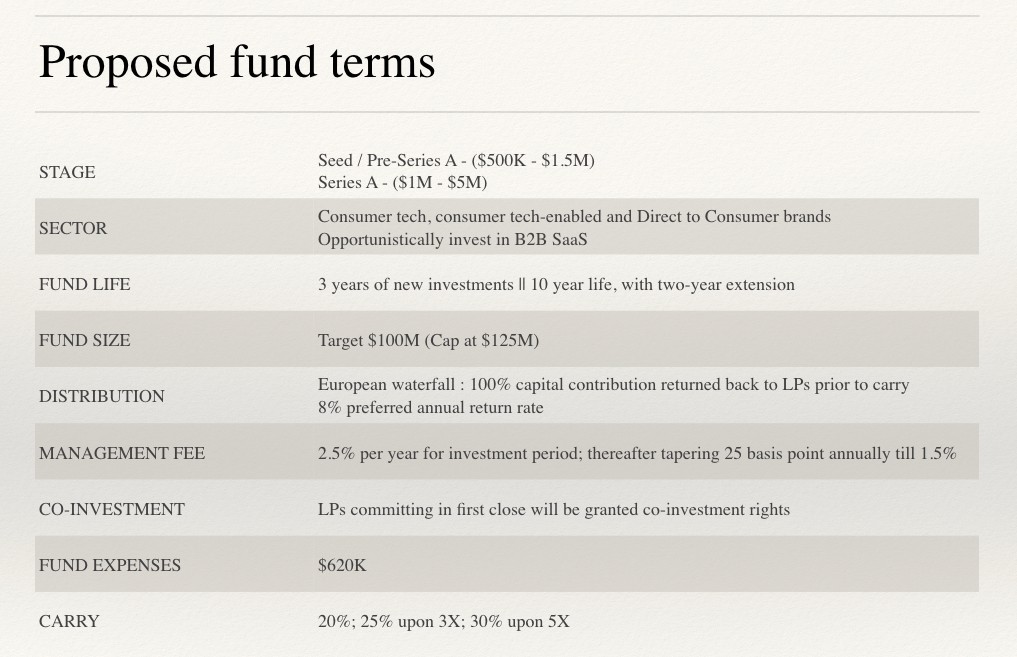

Like any first-time manager, I was flexible going into meetings with the fund terms. As a proposal, I had included following slide in my pitch deck :

An explanation of some of the unfamiliar terms & my rationale behind the proposal :

- Fund Life: It’s the sum of the investment period and the liquidation period. In my model, I had included three years of new investments and seven years of average liquidation period for investments considering the India market. Naturally, LPs prefer shorter liquidation periods.

- Distribution: proposed a waterfall distribution with 8% hurdle rate. As such, the entire capital needs to be returned plus an additional 8% interest compounded annually on the capital calls before any GP could draw any carried interest. Post-meeting the hurdle obligations, carried interest to be split as per the proposal.

- Management fee: this is the annual fee charged by the fund on LP capital commitments. A bulk of it goes towards salaries and fund operations. Typically, it’s between 2%-3%, depending on fund size and number of vintages. Large funds typically charge 2% while Micro/ Nano funds are able to justify a 3% fee given the small fund size. Top tier funds with the legacy of established returns can charge 3% regardless of how large the fund is. I had included a 2.5% management fee for the 3 year investment period in my model. For each subsequent year, the fee would taper by 25 basis point until it reaches 1.5% in the 7th year of the fund life.

- Fund Expenses: These are expenses that are allocated towards services like Fund Administration, Fund formation counsel, Banking, Audit / Tax, Insurance and other misc. expenses. The fund expenses is a one-time allocation for the entire fund cycle towards these expenses. Typically funds may require anywhere between 500K and 1M depending on the service providers they use.

Key Learnings From The Experience

-

Understanding the LP pool — targeting the right set of LPs

The global Limited Partners (LP) pool comprises of large institutional funds, family offices and (U)HNIs. Endowment funds, Pension funds, Sovereign Wealth Funds, Hedge Funds and Fund of Funds collectively constitute the Institutional LP set. In the first few months, I reached out to a few institutional LPs for exploratory chats to understand their outlook towards India / emerging managers and exchange notes on the VC fundraising process.

To give you some context, although my role at Accel was not responsible for managing LP relationships, I did end up forging some warm relationships with institutional LPs (outside of Accel ecosystem) through my personal rigour and outreach. As such, these guys were my first port of call when I decided to venture on my own. Through these conversations, I learnt the following :

- The minimum ticket size for most such institutional LPs is $25Mn and they seek no more than 10% exposure in one fund. There are a few who may stretch this to 20% but that’s very rare. As such, only managers with a fund size >$250M. should reach out to such LPs.

- Although the global institutional capital amounts to trillions of dollars, the allocation towards India Venture Asset class is a very small fraction. Anecdotally speaking, if there are a 100 institutional LPs in the world. And of these, if 20 invest in the venture asset class, maybe 5 would invest in emerging managers and at best 2 looks at India as target geography. The overlap of emerging managers and India allocation hence is a very small LP pool.

- Lastly, most of the institutional LPs who invest in India focussed funds have already committed capital to 2–3 top tier funds operating in the country based on relationships built over decades. As such, these LPs have access to 80% of the deal pipeline from the country already. It would take an extraordinary ‘existing’ relationship between the emerging manager & the LP to get the LP to commit. As I see it, some of the institutional funds that may invest in emerging VC managers from India are Adam Street Partners, ADIA, KAUST, LGT, ADIC, HillHouse among others.

- Family offices, UHNIs & HNIs — first Believers for an emerging manager: More than 70% of the capital for emerging managers comes from family offices, UHNIs & HNIs. So after initial months of disappointment, I reevaluated my strategy and started reaching out to such investor pool. My network in this set of LPs was limited to a few family offices in MENA and HK. One of the key learnings from this LP set was — they expected the emerging manager to allocate a significant percentage of the total capital commitments towards their domestic market. This was especially the case in MENA, where most family offices want to increase their participation & create a legacy in the region’s emerging tech landscape.

2. Too ambitious a target for an emerging manager from India

While I have witnessed my global peers successfully raise a first time fund of this size, it turned out to be a bit of a tough sell for me given the Indian market landscape and my limited investment experience. When I set the fund target of a $100Mn, I did so on the back of an investment strategy that allowed for significant capital reserves for follow-on rounds in portfolio winners.

I continue to believe that in India if you wish to build a successful VC franchise, you need to have at least a $100Mn corpus to write meaningful cheques in select companies. Else, you will end up becoming a feeder fund capping out on your potential outsized returns from the portfolio winners. The typical spray and pray strategy just does not work in India.

3. Going solo

When I started, I was aware of the LP affinity for picking Partnerships over solo GPs. However, I made a conscious decision to go solo for the first close and then on-board a co-GP. Partnerships in Venture Capital can be very tricky. Picking the right co-GP is as important a decision as picking the right life partner.

I wanted a co-GP who had similar value systems, an alignment in DNA and a personal-professional journey that’s seen some struggle. One with complementary skill sets, perhaps someone from an operating background with whom I have worked with for a while. I am certain most young emerging managers will relate to this challenge given the short investment career overlaps we have with fellow investors.

While I did identify a potential co-GP, a seasoned entrepreneur with a decade-plus operating experience, we both wanted to spend some time investing together before we signed up for such a commitment. We didn’t want to partner up solely for LP optics to accelerate the fundraising prospects. In hindsight, going solo was a bad idea. Your co-GP needs to be by your side meeting the LPs on day zero. Period!

4. Not having multiple closes

My advice to emerging managers would be to hold at least 3 closes, if not more, for their first fund. I was targeting a first close of $40M with a final close of $100M which in hindsight was not a very wise decision given my little understanding of (& access to) the LP universe at the time. Having a small first close helps build momentum and sends out positive signalling to the LP ecosystem. Further, it allows one to start investing in startups which indeed brings more joy than fundraising. 🙂

5. GP Contribution

GP contribution is the amount of capital a GP commits to the fund at the time of closing. The minimum amount the LPs expect from the GPs is 1%–2% of the fund. There is, of course, no upper limit to the number but most emerging managers commit 1%.

Since I come from very humble beginnings and had little personal savings, my biggest concern when I first started thinking of floating a fund was the GP contribution. While I had included a 1% GP contribution in my model, my proposal to pay the same was rather unusual/innovative (a combination of a sponsor, pay as you go and salary clawbacks).

The entire fundraising journey was incredibly challenging and humbling but added significantly to my learning curve. I am sure as a young investor, going out on a herculean task of raising my own fund, there are a lot of things I could have done better, but life is long and I am sure this experience will come in handy in the years to come.

The fundraising also took a big personal toll as I lost touch with lots of near & dear ones. But thankfully, I was fortunate to meet some equally great folks along the way who helped in ways I can only hope to repay someday. I am thankful to everyone who has been a pillar of support for me during the last few years. I hope my experience will inspire a new set of investors who want to set up their own funds and hopefully some of my learnings will help them raise their own funds.

As for what’s next for me, I am taking some time to explore options, continue some conversations which have been ongoing in the investment and the entrepreneurial world. Super excited (and equally scared) as I write the next chapter of my professional life. And of course happy to help anyone (be it on the entrepreneur or investing side) who might benefit from my experience.

{The article first appeared on LinkedIn and has been reposted with permission.}