Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

Continuing along the same lines of thought as my last post regarding a funding winter, I decided to dive deeper into the Indonesian funding environment and check what’s been keeping the market down for some time now. How do I know the market is down? Well apart from the numbers that I present below, we are just not getting enough interesting deal flow and have funded only one company in Indonesia last year despite all our efforts.

A sign of a healthy startup ecosystem is its angel activity. Angels are faster at writing cheques as they do not have to get IC approvals and are also not bound by fund timelines and capital constraints. They usually do not follow on into the next round, but have clearer risk-return structures. As a result, angel funding usually kickstarts an entrepreneur’s dream — a small amount of capital that the entrepreneur uses to build the dream team, launch an MVP and go to a fund with some numbers behind its back.

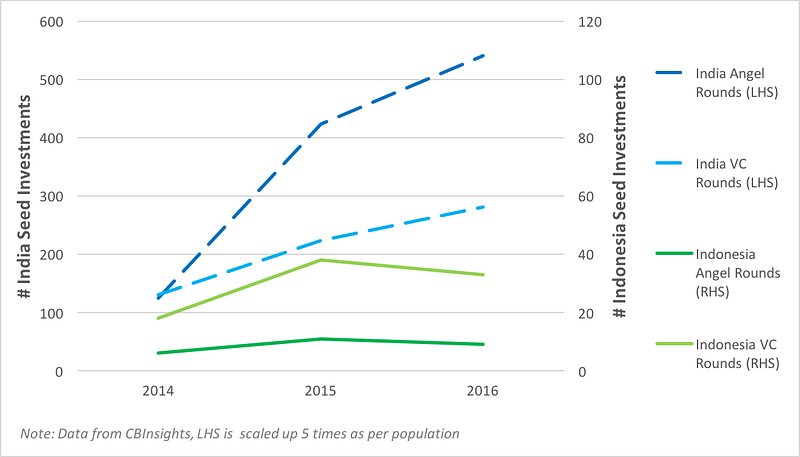

India, as you can see from the chart, has seen massive angel activity in the last couple of years. Who are these angels and why the sudden bullish environment? More than half of the 25 most active angels in India are actually angel groups. These are groups of high net worth individuals, who came together under an umbrella and decided to co-invest by forming syndicates.

The angel group usually identifies a few people to manage the deal sourcing and operations, but in the end each angel makes his/her own decision on each startup investment. India has multiple such groups such as Indian Angel Network, Mumbai Angels, Chennai Angels, and so on.

But what is interesting to note is that in the last couple of years, some super angels have emerged i.e. individual investors who have been writing cheques very frequently.

Think Rajan Anandan (VP Southeast Asia, India of Google), Anupam Mittal (founder of Shaadi.com), Pallav Nadhani (founder of FusionCharts), Amit Patni (from Patni family), Kunal Bahl (founder of Snapdeal), Vijay Shekhar Sharma (founder of PayTM) and so on. These angels either found liquidity through secondary share sales of companies they founded themselves or were rich enough regardless. But they have been the true backbone of the ecosystem and have kept the market alive in a time when the VCs tightened up.

Further, there is an immense amount of dry powder (capital with VCs/PEs) waiting on the sidelines in India. According to Preqin, this number is now more than $7B, ready to be deployed as soon as investors see a positive uptick in the market. Both the increased activity by angels and large dry powder give me hope that the market in India will continue to do well in the near term.

Turning our attention to Indonesia, the angel activity in the last couple of years has been abysmal. As seen in the chart, the number of announced seed investments by angels in India was 50 times higher than that in Indonesia. In fact, both the angel and Seed fund activity fell in Indonesia in 2016, which is now leading to a shortage of investable deals in the Series A section.

Funds focussing on Series A deals in Indonesia only (such as Venturra Capital) are likely going to have a tough time finding enough good quality deals in the market this year, and this is the reason these funds are already starting to move earlier and earlier into Seed or Pre-Series A rounds. This gap has been noticed by Seed funds in the region as well, and more and more of them are starting to focus on Indonesia. 500 Startups’ Khailee Ng is now based in Jakarta, and many fund managers are flying in every month to source the first cheque opportunities.

While individual investors have stayed away from investing in personal capacity, the country has also suffered from very few angel networks being formed. As of now, I only count two announced angel networks in Indonesia: Angin and Angeleq, the latter of which has yet to become very active.

Meanwhile, dry powder with VC firms is also increasing. More and more funds are being announced every month to focus on venture grade investments in Indonesia. From Kejora to East Ventures to Wavemaker, most Seed/Series A funds have been busy raising the last year, and are now ready with fresh capital to be deployed.

For the market to really see a turn, the angels in Indonesia now need to dive in. The market is, in my opinion, at its best timing. M&A activity is picking up and Indonesia is definitely on the global map with deals such as that of Go-Jek and Grab. With

With a shortage of capital in the seed stage, the valuations have come down and entrepreneurs are reasonable. This is a once in a lifetime opportunity for a few individuals to not only make a windfall for themselves but lay a foundation for their own brand and capital before the market heats up.

[This post first appeared on Medium and has been reproduced with permission.]

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.