SUMMARY

Globally, the neobanking revolution began a few years ago and is in full swing with companies like Monzo, Revolut, N26, Chime and others

Neobanking leads the second wave of disruption, termed Fintech 2.0, based on customer-centric, personalisation principles

Neobanking, which is virtual, branchless banking, in India may still be in its infancy, but it is already at the forefront of the second wave of disruption in the fintech sector

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

Making decisions related to your finances, be it savings, investments and loans is hard. It takes hours of comparing various products on your part to know if you are getting the best returns out there. And then there are micro-decisions. Should you invest in a mutual fund or in gold? Which loan would fit in best with your lifestyle and financial situation?

Now, imagine if someone – or something – could sort out all of this for you. A single platform to take full control of your finances with the aid of powerful AI that personalises offerings.

If you could experience banking that recognises you as an individual with your own set of preferences and choices?

Neobanking promises to do just that. Globally, the neobanking revolution began a few years ago and is in full swing with companies like Monzo, Revolut, N26, Chime and others flexing algorithms that bend to customers’ needs.

Albeit a nascent idea, India is not too far behind. The MEDICI India Fintech report 2020 says that neobanking leads the second wave of disruption, termed Fintech 2.0, based on customer-centric, personalisation principles. Neobanking players target the current pain points plaguing traditional banking in India, which include a lack of proactive customer service, unnecessary bank fees, lengthy resolution times, reliance on legacy systems, and no real-time support, among others.

India’s Need For Neobanking

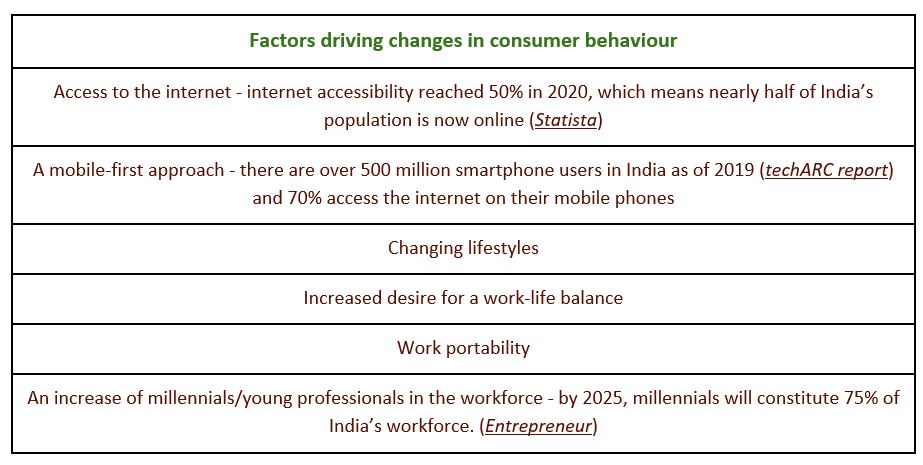

The Reserve Bank of India defines financial inclusion as the act of providing a “wide range of financial services at a reasonable cost.” Clearly, traditional banking has struggled to make these services accessible, unable to keep up with the rapid changes in consumer behaviour and the sweep of digitisation moving across the country.

Consumers are now demanding more plug-and-play solutions centred around flexibility, and hassle-free, time-efficient processes. Above all, they want banks to listen to them and provide the services and products they really need.

Addressing The Underbanked

Not too long ago, India’s biggest problem was that it had a large (190 Mn according to a 2017 World Bank report) unbanked population. That scale is now slowly tilting with the weight of an underbanked population – people who have bank accounts but do not use or have access to the full range of financial services. This is where neobanks like Niyo, Jupiter and P10 Bank are stepping in to fill this vast chasm.

In fact, a digitally empowered customer’s financial journey does not stop with online money transfers and payments. It extends to buying insurance, borrowing, exploring various investment opportunities, and building their savings.

This is one of the reasons why we built P10, we thought why can’t there be an app (for banking) that handles everything?” That was the turning point, which led us to develop a neobank platform, a secure, seamless way of managing savings, investments, bills, and payments all in one place.

Making Hyper-Personalisation The New Normal

Hyper-personalisation is the backbone of creating that refreshing consumer experience. Built on a technologically-forward framework, P10 Bank utilises user data to make relevant products and services available to its customers. For instance, if a customer books a flight using the P10 Bank debit card, they would be offered more relevant, related products like prepaid forex travel cards and travel insurance.

This Netflix-like hyper-personalisation looks at the user’s spending habits and other transactions to determine their needs down to the finest detail. Accenture surveyed banking executives across 30 countries for its 2019 report on digital banking, and 87% of them said that “customisation and real-time delivery will underpin future competitive advantage,” but only 38% were actually prioritising this move.

For us, however, personalisation forms the strong wireframe of their entire approach. Therefore, our goal is helping their customers achieve overall financial wellness by encouraging them to save, borrow, and spend in a systematic, planned way.

Today, we are catering largely to young professionals who are shaping consumer behaviour, the impetus behind the changing landscape of banking in India. These young audiences are challenging the banking industry to get out of their well-established comfort zones. Neobanks are game for it.

Summary

Neobanking, which is virtual, branchless banking, in India may still be in its infancy, but it is already at the forefront of the second wave of disruption in the fintech sector. Neobanks are challenging the existing banking system with their digital-rich business models, customer-focused approach, and a wide range of financial services.

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.