A Founder Exit Is Different At Different Stages, But It Cannot Be The End Game

Why start a company? To have a big founder exit, right? You don’t sit in a room, envisage a future and think, ‘Do you know what, I’m going to make someone a very happy VC indeed!’The main reason a startup founder is not funded (which they tend not to understand) is that their business is fundamentally not a VC fundable company though. Why?

Why can you have a nice, solid business, growing steadily and maybe even generating cash and not be of interest to investors? Some founders may read Tech Crunch and see stupid companies get funded and direct their ire outwards rather than inwards.

Most startups are not VC fundable because the potential exit value of the startup does not generate the returns needed to make VC math (their business model) work. If I offered you $50m for your startup, would you be happy? Well probably. For most, $50m is certainly a life changing event. However for almost all VCs it’s “eh,” a rounding error.

This is probably devastating news to some founders and they just don’t understand why they don’t get to be cool and have big founding announcements too. The VC approach to building startups is the cool aid founders have drunk reading Tech Crunch and the like. Large raises and super-human growth rates are what are celebrated. Profitability and generating real cash is something that Gen-X people used to do. But for us Gen-Y, that’s not the way to get rich it seems. Only that’s wrong.

If your goal is to make an exit and to bank a whole lot of cash, you need to check the math and question what the fame is worth (is it worth ending up with near nothing?). For sure there are a lot of ‘unicorns’ where the founders are not going, nor have, at exit made much cash, but the VCs have. The VC game is the VC game. It’s not the founder game. You need your own playbook.

Why Do VCs Want You To Be Passionate And Committed?

It takes a long time to build a big company. At least 7 years to get to an IPO. 7 years is a long time, so founders clearly need to be committed. VCs will say they want ‘missionaries not mercenaries.’ I can’t help but wonder if this is self-serving?

Bill Gates and Mark Zuckerberg are so rich because they own most of the companies they founded and those companies were worth a lot. If you don’t own most of the company, then this is a different story.

How do founders come to not owning their companies when they start out with 100%?

- They raise money to grow their company and give 10-25% chunks incrementally at ideally high values at consecutive fundraises.

- They hire expensive management to help them grow fast and give them shares (e.g. VP of sales), maybe add another co-founder in the early days.

- VCs also encourage the founders to make large ESOP pools to lower the effective valuation, or put another way ‘motivate and retain staff.’

Assuming investors have proper reserve planning, they hope over time to keep ‘doubling down’ on future rounds, maintaining or exceeding their pro-rata. The more they own of an increasingly valuable company the better. Although this is a zero-sum game and the founders increasingly get diluted and concurrently cede control.

For VCs to own more of the company, the founders need to be passionate and committed so the company can be around long enough for them to do so. It is only after many years of work does the company become valuable enough, not for the founders, but for the VCs.

Founders need to be aware that often they give their investors the right to allow a sale (or not) to happen. They literally can decide when you, the founder, can sell your company.

What Is ‘Enough’ Value For VCs And Why?

The basic heuristic is that your company needs to be valuable enough to return the entire value of the VC’s fund. For a $50Mn fund that is $50Mn, but for a monster fund like Sequoia or a16z have, that could be a billion dollars. This is also the reason why VCs invest in all these dumb ideas and not in you. The dumb ideas have a chance, albeit a small one to be big enough (for them).

Now the next heuristic to quantify this better, is the amount you raise, times it by 50x and that is the minimum value you need to get a VC excited. How does this work? VCs want 10x returns. They own maybe 20% (targeted holding). 10x/20%= 50x.

If you raise $10m you need a $500m exit for the VC to get $100m (20%). Theoretically the largest VC fund you can target has $100m under management.

If your VC is a micro-fund with $100m under management they are looking for you to be a $500m exit. Can you be a $500m exit reasonably? If not, then you are a pass. If you want the big guys, you need to be in the billions. The bigger the fund, the bigger your exit needs to be for them to care.

It’s important to state though that these are low end numbers (and this is all very simplified). 20% targeted ownership stakes to be held per VC are quite unlikely. This is more likely going to be in the realm of 10% (unless the VC has a lot of AUM). Most seed valuations are going to be between $4 and 10m. You only get your 20% holding at a $5m post if you are allocating $1m per round. You also need to assume the investor get the full raise (no other co-investors) and that the VC gets to keep investing at least at pro-rata in any subsequent round, which means your exit needs to be larger to compensate for additional funds subsequently committed).

What Is Enough For Your Founder Exit?

How much money do you want to make? This is a question I ask every single founder whether or not I am mentoring, consulting or looking at partnering with. Some get taken aback and most don’t have an answer, but I explain the amount you want to make will both instruct and dictate the kind of business you are going to build and how, as well as your funding strategy.

How you approach bagging $1m and $1bn founder exits are very different beasts indeed. Let’s face it, if you are looking to make $1m, no VC is going to fund you anyway. There are a lot of ways to make $1m, also, your exit opportunities for a $1m company are extensive – there are only a few companies that can afford to buy a $1bn company, so the exit is harder as well.

So be honest with yourself. How much is enough? Is it $10, 20, 50, 100 million? Get clear on that number and then you can figure out the kind of business which is enough for you as the founder and not a VC.

Founder math is not the same as a VC. You also only have one company; they have exposure to many. You only need a few million to be pretty comfy, whilst a few million does not work with the VC’s business model.

I can’t help but think the rhetoric of the world changing founder is a ruse invented by the same Madison Avenue PR firm that got people to buy compressed and polished coal as a subterfuge to prevent them from selling out too early and getting a higher RoI and payout.

Is It The Journey Or The Founder Exit That Matters To You?

Many founders start companies because they don’t want to work for a big company. They want the freedom of being their own boss. The issue is that economics and control can be mutually exclusive. Having control doesn’t necessarily yield the highest returns.

In an academic paper, Noam Wasserman, former professor at Harvard Business School has found that founders having more control leads to lower valuations. I just blogged about this here.

“Both qualitative case studies and quantitative analyses of more than 6,000 private companies highlight that startups in which the founder has maintained control (by retaining a majority of the board of directors and/or by remaining as CEO) have significantly lower valuations than those where the founder has relinquished control. This is especially true when the startup is two years old or more.”

Now there is some food for thought. Let’s look at an example of where a founder lost control:

In 1997, when first-time founder Lew Cirne founded Wily Technology, an enterprise-application management company, he faced a wide variety of decisions about how to build his company. Over the next two years, he hired experienced executives, built a team of fifty employees, raised two large rounds of financing from top venture capitalists (VCs), and gave up three of five seats on the board of directors to those investors.

When it came time to raise the next round of financing, the board decided that Wily needed a CEO who had stronger business skills than Cirne, who had a technical background. Their choice, “professional CEO” Richard Williams, replaced Cirne as CEO. For his part, Cirne was left with a very narrow technical-visionary role within the company.

However, Williams was able to lead Wily to a big exit: a $375 million sale to Computer Associates in early 2006. Cirne admits he could never have accomplished such value creation, but he nevertheless was left with painful regrets about his early decisions that had led to his being replaced.

What matters to you? Having the biggest possible founder exit, or being the boss of your own company ad infinitum? There may be some gradient between the two, but fundamentally once your train goes on the VC tracks there is no looking back. You are a VC funded company not a bootstrapped one. Another way of thinking about ‘freedom’ is you have the freedom to build a company till you reach your limits, in the opinion of VCs, allow a professional CEO to step in, build it to a bigger exit and then have ‘financial freedom’ thereafter. Not about outcome for some.

If the idea of being the CEO is symbolic of your freedom, then understand that the most important lever a VC has (if they control the board) to influence the value of their investment is the ability to choose and fire the CEO. Put another way, the most valuable lever they have is the ability to decide if you have control or not of the company you started.

The reality is I think most founders are more mercenary than missionary at the end of the day, and so a nice big exit sounds pretty fine indeed. Only when it comes to the reality that you aren’t Bill Gates and don’t successfully navigate to retaining control and economics, it will be rather painful hit to your ego if you have one.

There are, of course, benefits of getting a nice founder exit. You not only make cash, but you can use it to do it all over again and have even more control.

Soon after leaving Computer Associates, Cirne decided to found his next startup, New Relic. He solo founded New Relic and tapped his favourite Wily employees for his early hires. He cautiously self-funded New Relic for as long as he could, and made sure to keep control of his board of directors and to remain CEO, even at the expense of growing more value.

More value is relative; New Relic is now public and has a market cap of $1.6bn.

Decide what is important to you. You can’t typically have your cake and eat it too, but there is also a long game you can play.

How To Maximise Founder Exit Value – The Founder Playbook

I am going to take for granted you want to go the VC route. The key math for you as a founder to do is figure out the best time to sell when your equity is at a local maximum.

Your ability to sell will be based on a number of factors you will likely not be able to control:

- Market valuations. What are the comps in the market and what are you worth? Is it 5x or 10x revenue (or other metrics). The public markets, recent acquisitions, the strategic nature of your offering, competitive pressures will all contribute to this

- Willing acquirer. Does someone want to buy you when you want to sell?

- Ability to sell. Do you have the right to sell your compay? Will your board (investors) allow you to sell if you got a decent offer, or do you have to keep pushing for the fence?

Value Of Equity May Not Be Bigger At Later Funding Stages

You need to understand that the value of your equity at different funding rounds is fairly predictable. There are heuristics to tell you the mean and median levels of dilution you will suffer. There may well be points in time that the value of your equity remains constant over time – meaning your founder promote (value of your equity) may be worth the same at S-A as at S-D. Why, because the level of dilution you suffer and the rate of valuation appraisal fall out of line.

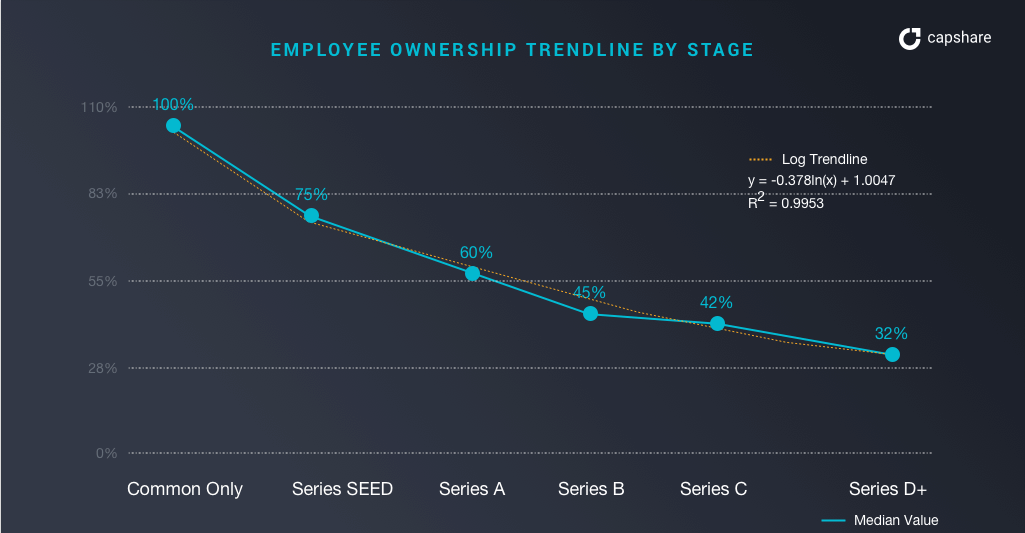

What do founders own at different stages?

What is the founder promote at different stages?

At Series D founders’ stock (as a group- meaning if there are 3 founders you need to divide by 3) was worth only $6.52m at a “median” as opposed to $52.45n at the mean company. Note at seed and Series A, it is almost the same for a median company.

Selling at seed can be the same value as at Series D

Median performing founders may have a better personal RoI to sell earlier, than to wait to future stages of growth. Ironically, there are also less potential acquirers the larger you are.

If your startup is an outlier, a unicorn in waiting then this situation is very different. You can keep going and keep being worth more and more. Only, that is for the multiple standard deviations- the black swans (unicorns).

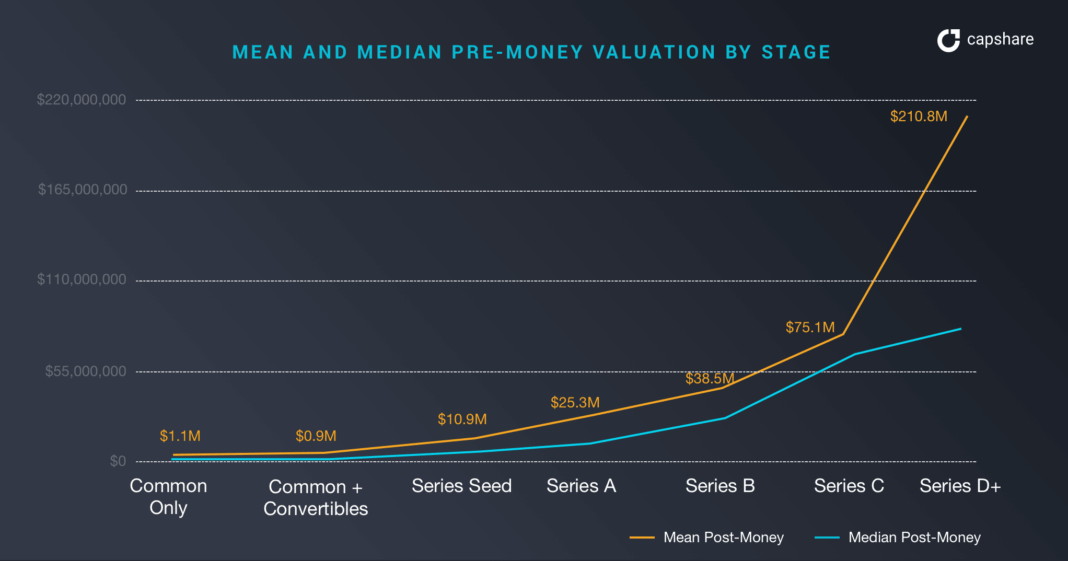

Valuations Of Startups By Funding Stage

Here we can see the difference between the mean and median for the differences in valuations between the unicorn outcomes and everyone else. The difference in pre-money valuations between the mean and median at Series D is $144Mn. The gap begins at the Series Seed and persists at all stages.

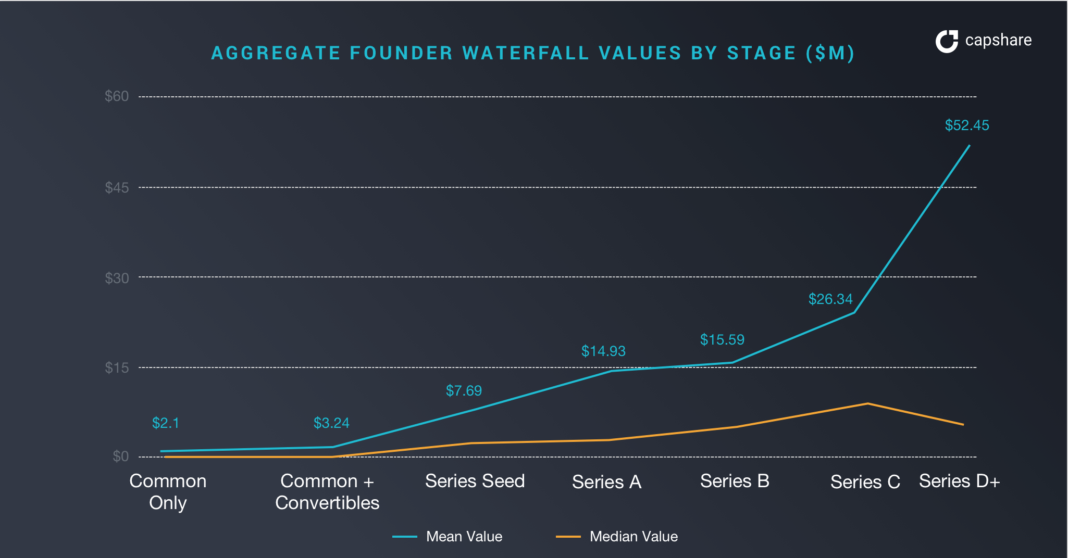

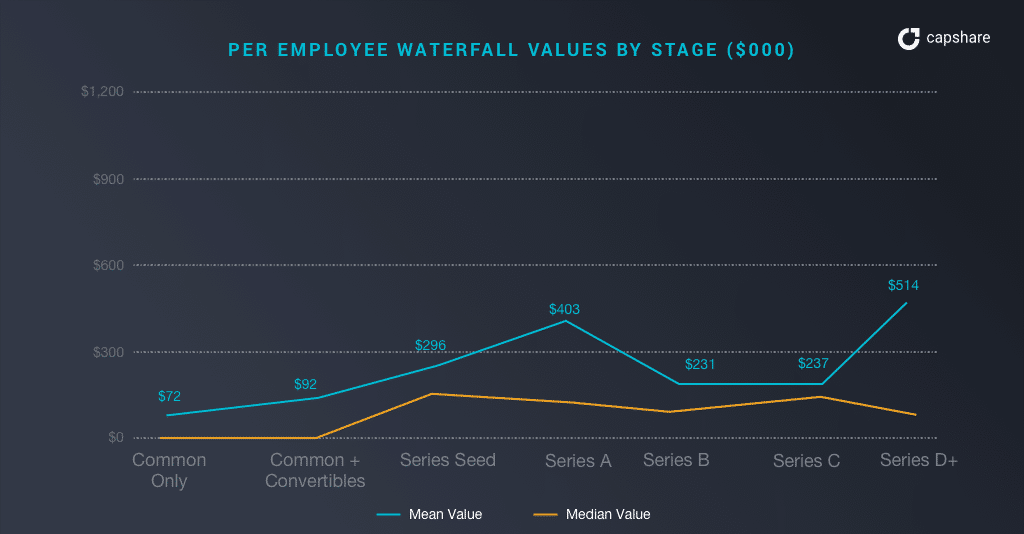

Value Of Staff Shares By Stage

If you particularly care about bringing in your staff into the ‘founder math’ calculations, there is not much value of them encouraging you not to exit as soon as possible unless the exit is big.

If you do waterfall math, which accounts for payments of liquidation preferences etc., median per-employee (this includes founders) waterfall values hover around $130-$190K, whereas mean per-employee waterfall values are about 2-5x that value. Employees want your startup to be an outlier as much as you do.

Note: per-employee figures include founder amounts. So non-founder employee numbers will be significantly smaller; assume that non-founder employees would be 50% of the figures above.

If you are a mid-level employee at a median performing company, your equity is probably worth $65-95K if the company exits at its latest valuation. However, if you are a mid-level employee at a top performer, your equity could be worth somewhere around $130K-$500K.

Hacking Outcomes By Stage

This chart shows wonderfully how founders can hack their outcome.

If your company exits around Series D, you can expect the following splits:

- Founder ownership: 11-17%

- Other employees: 17-21%

- Investors: 66-68%

Key here is the founders own about 11% of their startup at series-d. At Seed they own about 61% (one round dilution + creation of ESOP pool). At D, the valuation of your startup has increased, but maligned to creating value to the founders ownership.

Examples of dilution and valuation going in the wrong directions for founders are evidenced by the following founders:

- Box: Aaron Levie, founder of Box, owned about 4% at IPO in 2015.

- Zendesk: CEO MikkelSvane owned about 8% at its IPO in 2014.

- ExactTarget: Co-founder owned 3.8% at the time the company filed its S-1

If your pre-money is about $11Mn and you set to work putting that investment to work, the possibility of finding a buyer to acquire you for $38m is not out of the realm of possibility, right? That’s where founder math comes in; Post seed with a nice little acquisition and series-d at the investment pre-money, your founder promote is worth the same at $7.7Mn!

Wtf. The level of risk and sleepless nights to get to series-d from seed is a lot! You create 7x value for the VCs but your value is the same! That clearly doesn’t make sense. The founder playbook, if you could see into the future, is to sell out at seed, vest for a while and start another company.

The reality is the situation is even worse if you were to sell at your series-d as you would have a mountain of liquidation preferences to pay before the founder exit.

This clearly is totally against the VC math playbook. As we discussed above, $40Mn is light years away from the $500m VCs are ideally looking for to have a meaningful exit. So there is the problem, if the only playbook you know is the VC one, you are not maximising your outcome and time commitment. It only makes sense if you buck the mean and become an outlier. You are a founder because you don’t believe you are the mean though, right?

[This post by Alexander Jarvis first appeared on the official website and has been reproduced with permission.]