Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

While watching your favourite programme on television, you might have come across the latest Indusind Bank advert featuring Boman Irani (Bobby uncle) always trying to one up his neighbour, Farhan Akhtar (playing himself). This time, they’re comparing banking services and Farhan comes up trumps when he displays Indusind bank’s new Fingerprint Banking system that replaces passwords with a fingerprint. Utterly disappointed, Bobby uncle leaves the scene to open an account with IndusInd bank.

Whether it’s the Deepika Padukone ad for Axis Bank’s mobile banking initiative or Indusind’s video branch feature, there have been a flurry of communications, off-late, by the banking giants of India signalling a change in the medium of their process.

The Digital Transformation

The last few years have seen the banking industry change from a predominantly transactional business to a customer-centric one. By 2020, it is estimated that digital natives are going to form the majority segment of customers thus changing the industry ecosystem and forcing financial organisations to shape up or ship out. The digital sector is evolving rapidly and encompassing each facet of banking and financial institutions today, need to be on top of their game to stay ahead of the competition.

Emergence of FinTech

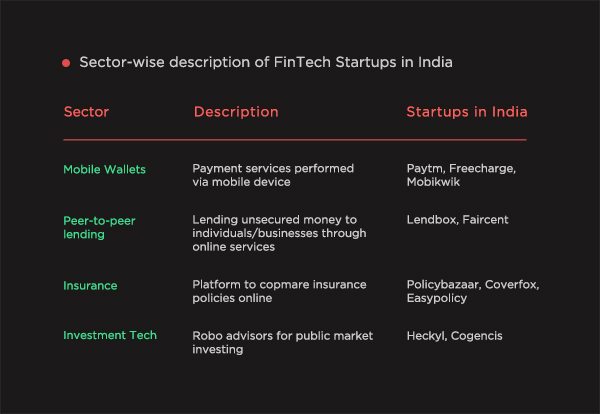

The digital revolution has given rise to an emerging technology-driven financial services sector, now known as the FinTech sector. This sector covers services related to mobile wallets, payment solutions, peer-to-peer lending, insurance, banking technology and cyber currency.

Sector-wise description of FinTech startups in India:

Constituents of FinTechIn 2015, the Indian FinTech sector was in its formative stages. This period saw the emergence of numerous startups, incubators and investments from public and private investors. It was clearly reflected that the right mix of technical expertise, capital investments, government policies, regulatory framework and entrepreneurial mindset could be the driving force to establish FinTech as a key enabler for financial services in India. Looking at the progress that the key constituents of fintech have made in 2016, we are well on our way to achieving this goal.

Government

The Indian government has been successful in adding over 200 million unbanked individuals into the banking sector through the ‘Jan Dhan Yojana’. ‘Aadhar’ has been extended for pension, Provident Fund and the ‘Jan Dhan Yojana’. This ensures the seamless crediting of subsidies and other proceeds straight into the linked account. With regards to tax benefits, the government is offering tax rebates for merchants accepting more than 50% of their transactions digitally, 80% rebates on the patent costs for startups and to withdraw surcharge on online and card payments for availing of Government services.

Investors

FinTech investment in India increased from $247 Mn in 2014 to more than $1.5 Bn in 2015. India has a comparatively lesser number of angel investors (1800 in 2016) than the USA (300000) but is witnessing increasing interest levels in startup funding. While VC firms have been early stage investors in fintech businesses, banks and other financial institutions are getting involved in the growth stage of these businesses.

Barclays and Axis bank have already initiated processes to set up accelerators in two locations in Mumbai, where they are offering resources like help with project management, pitching opportunities to senior management and problem statements from their databases. Barclays is even offering to share its customer database with particular fintech companies to test their products.

Startups

The transaction value of the Indian FinTech sector is estimated to be approximately $33 Bn in 2016 and is expected to reach $73 Bn by 2020.

2016 saw the emergence of startups like Active.Ai in the artificial intelligence space, fonePaisa in the payments solution space, Hummingbill in the SaaS space and SayPay in the biometric authentication space amongst others. FinTech startups are most certainly off to a good start. However, to maintain the momentum of the FinTech sector, it is their responsibility to demonstrate to our regulatory bodies that they can benefit the society, by putting forth ample evidence to the public, institutions and the regulators that they can be regulated and monitored sustainably.

A successful FinTech ecosystem of the future will be where all the market participants connect engage and share ideas across vibrant communities and networks as well as identify and convert opportunities into business. In this age of penetrative technology, no market participant can afford to operate individually.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.