Covid-19 has undoubtedly posed a wide array of new challenges and a newer landscape in the lending world

Every borrower was a good borrower before it turned bad

It’s time to control the actual outflow of funds ensuring funds are used only for intended purposes

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

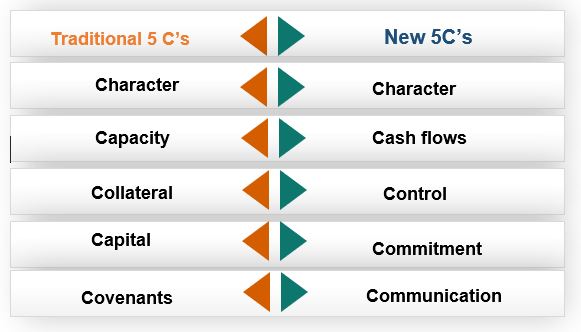

The credit analysis universe is commonly governed by the famous 5 C’s – Character, Capacity, Capital, Collateral and Covenants. Whether it is sourcing, appraisal or monitoring, these are the five attributes which asked to look at especially when we are lending to businesses.

The unexpected emergence of the dreaded pandemic has undoubtedly posed a wide array of new challenges and a newer landscape in the lending world wherein every “C” of the model is affected. Borrowers are taking moratorium on repayment (supposedly affecting their character), their repayment capacity (historically judged from quarterly P&Ls) has reduced, values of collaterals are going down, RBI itself has asked to soften the capital requirements and most of the stipulated covenants are getting breached.

It is indeed organic repercussion of the situation that many of the credit folks are wondering how to lend in these times. Clearly, the need of the hour is new through the process. Based on my own experience and understanding, I propose a new version of 5C model of credit, replacing or modifying earlier mantras.

Character

One can possibly lend a good guy in bad times but should never lend a bad guy even in good times

Character is one attribute that cannot be excluded from any model. While historically, we have always judged a borrower’s character majorly by his credit history, the horizon in today’s time has to be widened. Every borrower was a good borrower before it turned bad. This very simple realization means that we need to move beyond bureau scores and repayment history.

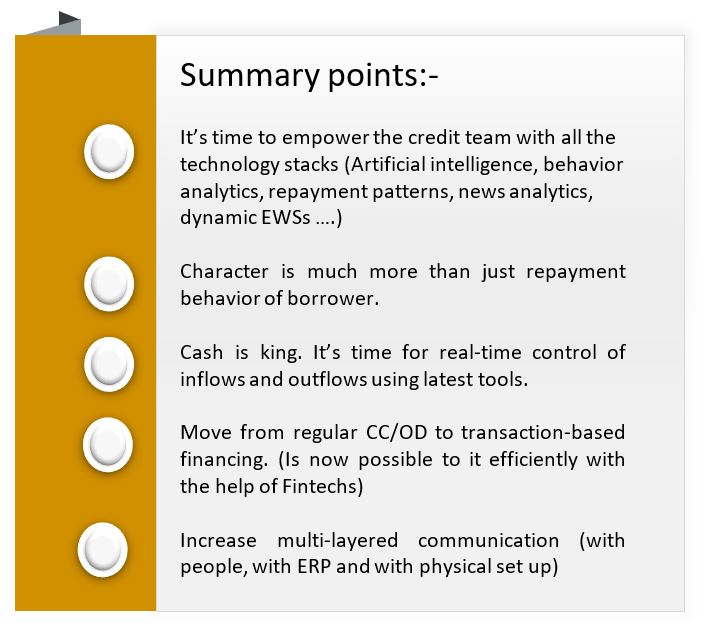

Behaviour aspect of a borrower is equally important. On the science part, we need to add tools like AI modeling and behaviour analytics. On the art part (since this attribute is more of an art than science), need to look at smart clues. How thrifty the borrower was in these times? Whether the borrower really needed the moratorium? How was the borrower able to fulfill (even partially) its commitment to creditors (employees/operational/financial)? Answers to some of these questions will give enough hints about the character of the borrower.

Cashflows

Turnover is vanity, profit is sanity but cash is reality

Cashflow replaces the attribute capacity in the proposed new model. Capacity has been generally judged by P&L related ratios (interest coverage, DSCR). However, since a lot of profit is actually stuck in debtors, it is the cashflow that really matters. So how to ensure regular cash-flows? Two points are crucial. First, your customer’s customers should pay and second, your customer’s customers should pay only to you (the lender).

For the first point, KYCC (know your customer’s customer) is important. We generally add a small para about the top 5 buyers of the borrower in the proposal note. But except for auto OEM borrowers (where the supply chain is clearly defined), I have not experienced deep analysis of buyers of borrowers. This happens primarily because takes an overall comfort on borrowers’ business, industry and vintage. But it is your borrower’s customers from where the repayments of the loan would actually come from, right?

Here, the challenge is, how can we analyze tens of customers of thousands of borrowers? The answer is in technology. FinTechs can pitch in helping to know a) whether the borrower’s customer is genuine (APIs are available for KYCs, Account & vintage verification) and b) How likely the repayment shall happen on time? (repayment patterns, news analytics, IPIs can aid in same).

For the second point (i.e. cash-flow routing), the simplest solution is to convert regular CC/OD lines to transaction-based lines (invoice discounting/factoring/PO based finance). Cash-credit as a product is not there in any other major economy barring India. In transaction-based finance, every borrower’s customer will pay to a dedicated lender’s account only. Further, it will increase the authenticity of transactions, give you the exact repayment behavior of each buyer and further strengthen your early warning mechanism (with invoice level matching any delay in debtors will be easily visible).

Borrowers may object on account of two reasons. First, they themselves are anticipating delays in invoice payments (the reason why TREDs volumes are decreasing). So, adequate grace periods need to be cushioned while discounting. Second, it is operationally cumbersome to discount every invoice. This problem can be sorted with adopting digital invoice discounting solutions where direct invoice level matching happens (further authentication from GSTIN). It also enables smart collections via emailer, links and other channels ensuring invoice repayment happens directly to lender’s account. Host to host integration can be other solution (though possible only in large enterprises)

Control

In a running business, the operational creditors supplying the next lot of material are the ones who get paid first.

Control now rather than doing a post mortem via end-use monitoring. It’s time to control the actual outflow of funds ensuring funds are used only for intended purposes. With new tools, one can authenticate every vendor to whom payment has to go, and for a larger amount, one can actually control invoice level payments. Every payee’s authentication (KYCs, bank account & other details) can also be done. Again, one cannot handle the volume manually but can make use of necessary technology solutions for same. PO based lending with transfers directly to borrowers’ suppliers will ensure funds within the business operations.

Commitment

While there are different viewpoints on the same, I personally believe, it’s not the promoter’s margin (or capital proportion) that matters, but its promoter’s intent. Already RBI has allowed banks to soften the capital contribution for MPBF calculation. Margin money should actually match with the operating profit of the firm. One can discount debtor invoices to directly pay creditors (with margin being released only after invoice payment). That way, one need not collect the stock statements (margins are getting managed real-time).

On the behavioural aspect, one needs to check the level of involvement in the business. Is it the only business the promoter is managing? how involved the whole family is into the business? How many PGs from the promoter family are provided? These questions shall answer to the level of commitment.

Communication

It’s more important to hear what isn’t being said

In a fast-changing world, rather than monitoring covenants, what is more important is to have regular (& possibly real-time) communication with the borrower. Communication has to be three layered; with people, with ERP and with physical set up. Credit managers hardly communicate with clients but the same has to increase. Also, the personal interaction should not be restricted with CFO, but also to one layer up (promoter) and one layer down as three of them see the company differently.

Further, with API’s, real-time integration is possible with the borrower’s ERP giving exact details of sales, purchase and collections. Further, plant visits reports can be complemented with actual video footages of the plants. In fact, this is the right time to get borrowers to accept for all the monitoring tools you were always looking to implement. These tools shall not only give right early warning signals but also resist promoters from the thoughts of diverting funds.

Happy Lending.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.