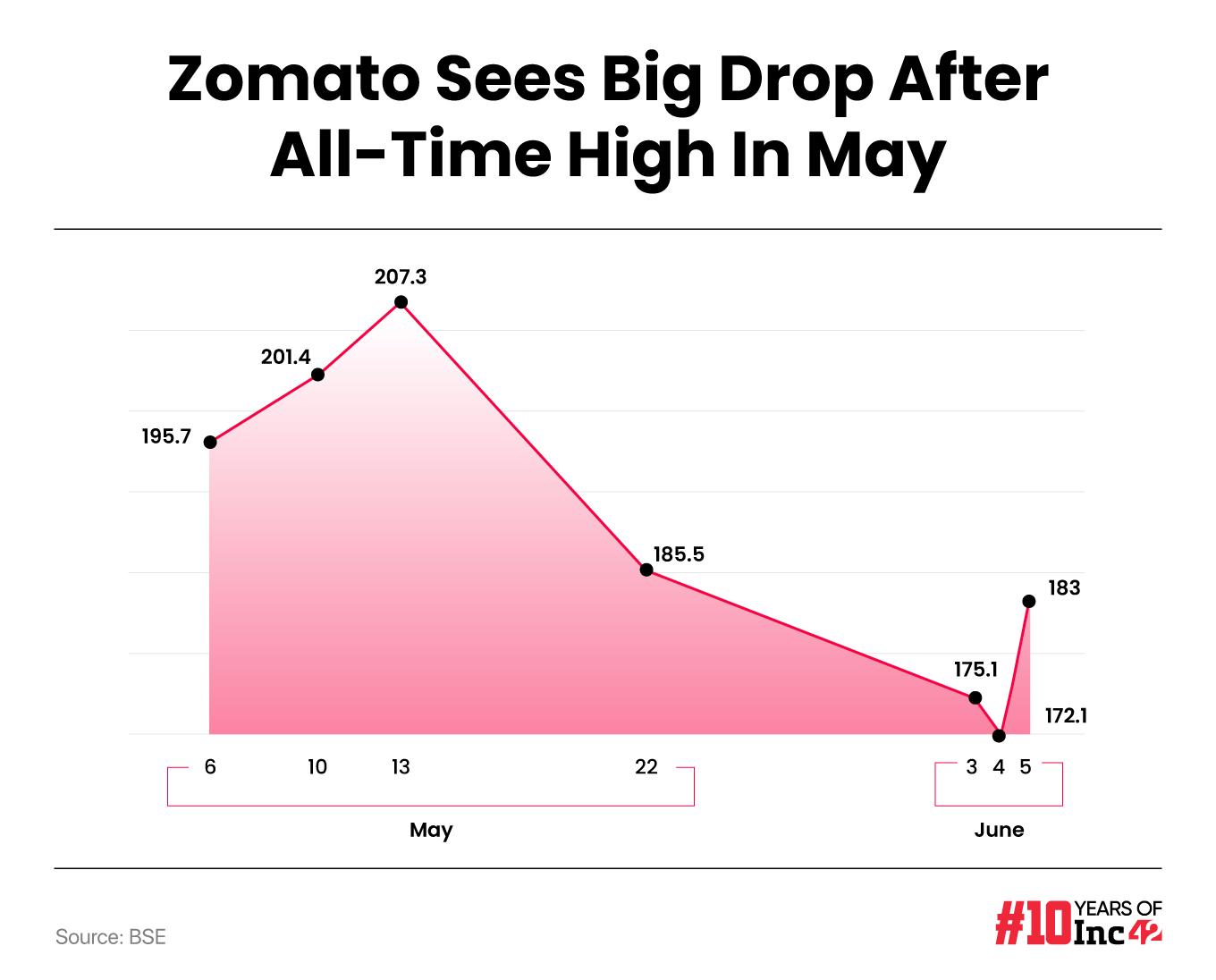

From an all-time high of INR 207 during the intraday trading on May 13, Zomato closed Wednesday’s (June 6) session at INR 183.65 – a drop of over 10% in less than a month

Despite the high potential for Blinkit, a profitable food delivery business and the ever-growing Hyperpure B2B vertical, Zomato seems to have lost some of its charm in the stock market

Investors believe that lot of the value built into the Zomato stock over the past year is linked to the growth potential for Blinkit, which is set for competition from JioMart and Flipkart in the near future

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

The Zomato stock has been one of the most intriguing success stories from the 2021 vintage of startups that went for public listings.

After popping on listing, Zomato has typified the investor sentiment when it comes to tech stocks. In the first year of being a public company, the Zomato stock crashed, along with the rest of the market, amid the massive sell-off at the end of 2021 and early 2022. However, this also set the stage for a big comeback.

And Zomato’s comeback did happen, coinciding with the company inching towards profits by around March 2023. We’ve of course covered the ups and downs in detail, but every quarter for the past five quarters, Zomato gathered momentum and became one of the hottest stocks.

The company’s market cap touched the $20 Bn (INR 1.6 Lakh Cr) along the way, and when Zomato ended FY24 with record profits of INR 351 Cr ($40 Mn), it seemed that the stock would continue to climb. But in the weeks since the release of its Q4 results, Zomato has been one of the weakest new-age tech stocks.

After touching an all-time high of INR 207 during the intraday trading on May 13, Zomato closed the trading session on Wednesday (June 6) at INR 183.65. This is a decline of over 11% from the all-time high mark in less than a month. In fact, the stock fell to as low as INR 146.85 during the intraday trading on June 4, when the votes for the Lok Sabha elections were being counted.

However, the stock did manage to rally nearly 7% on June 5 as investors went shopping after the previous day’s crash. But despite the high potential for Blinkit and the possibility of unlocking massive profits there, Zomato’s profitable food delivery business and the ever-growing Hyperpure B2B vertical, Zomato seems to have lost some of its charm.

In fact, even the day after it reported the profits for the full fiscal year FY24, Zomato saw a 6% drop in share price.

At the time it was believed that the company’s less-than-robust performance in the food delivery segment particularly grated investors, many of whom looked to book profits anticipating slower growth in Q1 FY25 (the ongoing quarter).

In its Q4 presentation and earnings call, Zomato stressed that it would also have to invest heavily to scale up Blinkit, which is also being seen as a hurdle in the quick commerce vertical’s bid to reach profitability.

Zomato Stock, But Value Tied To Blinkit

The rapid growth seen in the quick commerce business has compelled Zomato to double down on Blinkit. It is looking to nearly double its store count by the end of FY25. This aggressive expansion is also likely to have tempered investor expectations around future growth in profits.

While Blinkit did turn adjusted EBITDA positive in Q4, the road to full profitability is still long. And since the Q4 results, a raft of bad signals have come to the market, including the entry of Reliance and Flipkart as stiff competition in quick commerce, possibly spooking many investors.

Mukesh Ambani-led Reliance Industries Ltd (RIL) is reported to be close to launching its own quick commerce operations through JioMart after taking a punt earlier and pulling out.

The conglomerate is looking to deliver groceries in select cities in under 30 minutes and is likely to ramp up operations by next year. Reliance reportedly plans to take it to around 1,000 cities in future, and JioMart will tap into Reliance Retail’s network of over 18,000 stores across the country.

That kind of scale would allow JioMart to potentially catapult the existing group of quick commerce apps — Blinkit, Swiggy’s Instamart and Zepto — and also end the nascent ambitions of Tata-owned BigBasket and Flipkart before they take off.

Flipkart is fresh with funds from Google and majority stakeholder Walmart and is also likely to make a major push for grocery delivery, where Blinkit, Zepto and Swiggy have created well-oiled playbooks.

While the potential threat from Reliance cannot be ignored, the fact is that Blinkit has not yet cleared the doubts in the investor mind by itself. So JioMart only compounds the problems for Blinkit.

Remember, Blinkit is not just a vertical for Zomato, it could soon become larger than food delivery. Analysts such as Bernstein estimate that Blinkit will have larger revenue than food delivery by FY27.

“A lot of the value built into the Zomato stock over the past year is linked to the growth potential for quick commerce, and if Zomato is shedding the gains now, that’s largely because of the potential weakness in the Blinkit narrative,” according to an analyst at a Mumbai-based brokerage that has been covering Zomato since August 2021, a few weeks after the listing.

Patience Needed For New-Age Stocks

Another thing that most analysts told Inc42 is that Zomato is not a stock for the short-term gain chasers. It’s a stock that can have a 2X or 3X growth in the next two years if investors show patience. This seems obvious, but it’s important to have this context when talking about the recent weakness seen in the stock.

Particularly because a lot of new-age investors are joining the market who are more exposed to the power of brands like Zomato or Nykaa or Paytm. Paytm’s woes have become part of memes, but the fact is investors have lost real money and it won’t be the first time that a ‘startup’ stock sees such a meltdown.

“Zomato’s gain in the past year is only half the story. The stock has grown as a direct result of operational efficiency, but this comes at the expense of a large scale. Zomato still needs to show it can continue to bring in profits despite the investment needed for scale which is a matter of a few quarters at least,” the analyst quoted above added.

Investors in the public market cannot expect to see the rocket growth that private market investors and VCs are used to. Assuming that a new-age tech stock will sprout wings is a big mistake made by investors, particularly novice investors, because they may not see threats to business models in the same way as experienced investors who have lived through cycles.

“Tech-first business models are more exposed to the changes in the underlying infrastructure and the internet ecosystem around which they are built. Newer investors don’t have the years of expertise needed to react unpanicked to such changes, one relevant example of which is AI,” the founder of a Bengaluru-based consultancy and auditing firm added.

However, one cannot blame investors alone. Brokerage signals are not all in the Zomato stock’s favour.

Australian brokerage firm Macquarie gave Zomato an ‘underperform’ rating and assigned the stock a price target of INR 96, roughly half of the price Zomato is trading at today.

Macquarie’s view is centred around the competition from Reliance JioMart which has a last-mile logistics arm Grab, and has invested in Dunzo which does have operational history in the quick commerce space.

And given that Swiggy is also likely to be listed within a year, things are not going to be easy for the Deepinder Goyal-led company. Zomato has done the hard yards when it comes to profits, but now it has to drive value for shareholders to retain their long-term faith and that’s an entirely new ballgame.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.