The angel tax regime has undergone metamorphosis more than a dozen times since its inception. Despite this, it has been time and again contested by the stakeholders who have continued to be in pain under its reign

While the intention of the government behind such a tax levy was to curb the inflow and outflow of unaccounted money, it now sees every startup with the same spectacle

Industry stakeholders see standardisation of the scrutiny process and upgradation of the CASS system in accordance with the startups as some of the key reforms needed in the long run

Angel tax has been haunting Indian startups since its introduction in 2012, and many entrepreneurs today want a permanent solution to the complexities that this taxation regime brings.

Notable, since its introduction, the angel tax has undergone metamorphosis several times. Despite this, it has been time and again contested by industry stakeholders who have continued to be in pain under its reign.

Is there a solution to the angel tax issue?

Well, that is exactly what we will try to uncover in this piece. However, before we move ahead, it is imperative to be well-versed with the origins of the now highly controversial taxation regime that has many new-age founders on tenterhooks.

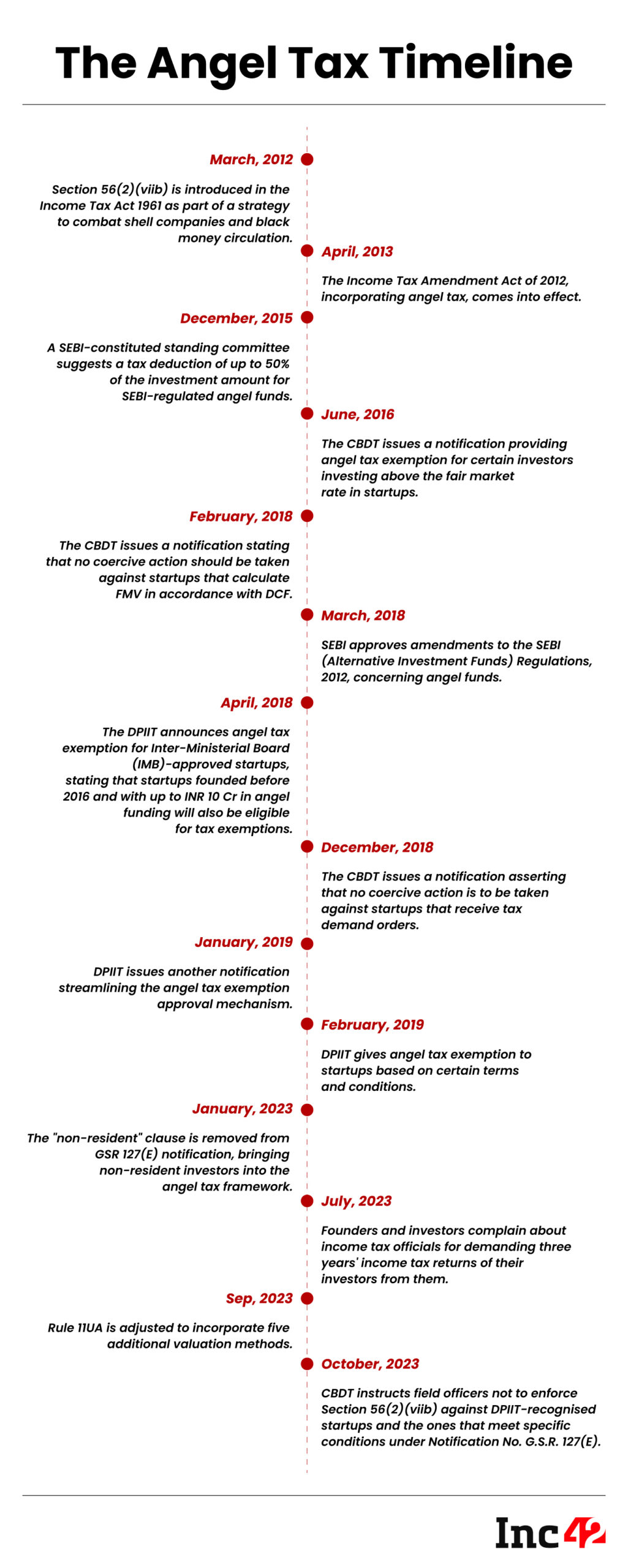

The story of the now infamous angel tax starts with the introduction of Section 56(2)(viib) in the Income Tax Act, 1961. The Government of India, in 2012, included the sub-section in the I-T Act to keep shell companies at bay and tighten its noose on the generation and circulation of black money.

Simply put, this is a tax payable on capital raised by unlisted companies if the value of the shares issued to investors exceeds their fair market value (FMV).

And, this was a non-issue for startups until 2016, when Income Tax officials started sending the notices to startups as well under the Section 56(2)(viib) and Section 68 questioning

- Revenue is not matching the projected value

- The valuation method

The Income Tax officials since then have asked startups to pay the angel tax as per Section 56(2)(viib).

While the government’s intention behind such a tax levy was to curb the inflow and outflow of unaccounted money, it now fails to distinguish between genuine and fraudulent cases, as some would say.

This is probably why Subhash Chandra Garg, former secretary of the Department of Economic Affairs, Ministry of Finance, wants the entire tech startup ecosystem excluded from Section 56(2)(viib) angel tax.

Speaking with Inc42, Garg said, “The wrestling going on for the last six to seven years to find a fix for the original sin of Section 56(2)(viib) should stop by abolishing this section for technology startups.”

In his book, “We Also Make Policy”, Garg elaborated that tech startups are not vehicles for money laundering and that changing the Department for Promotion of Industry and Internal Trade (DPIIT) notification alone was insufficient.

Garg has a point here. Even if there are a few cases of money laundering, the entire ecosystem must not be blamed and punished on the back of assumptions that the money being invested in them would eventually be syphoned off.

It must be noted that the Indian government has made several amendments to the now overly complicated taxation regime, but Indian founders hardly see any relief.

Before delving into the suggestions brought forth by industry experts, let’s steal a glance at what the existing norms are all about.

The Existing Norm

In February 2019, the Indian Government after much hullabaloo, notified G.S.R 127(E) guidelines that allow startups to go for angel tax exemption.

According to the notification, an entity could be exempted from angel tax, if

- It’s a DPIIT-recognised startup

- The aggregate amount of paid-up share capital and share premium of the startup after the issue or proposed issue of shares, if any, does not exceed INR 25 Cr. This does not include VCs.

Such startups are asked to file a declaration in Form 2, which states:

- They will not establish any subsidiaries for the next seven years.

- Will not provide loans or advances, including salary advances to employees.

- The startups have not invested in any assets, such as buildings or land, beyond what is used by the startup and so on.

The declaration list to apply for the angel tax exemption is way too long.

According to Diana Mathias, a partner at N.A. Shah Advisors, startups typically expand through acquisitions, which enable them to enter new markets and reach new customers. However, when this happens, the startup exemption is revoked.

“These conditions are challenging to comply with, and genuine startups still in the growth process face heightened scrutiny from income tax authorities regarding their pricing and valuation mechanisms adopted in hindsight,” she said, adding that only a few startups opt to file Form 2 as a result.

Interestingly, an RTI response by DPIIT revealed that between February 19, 2019, and September 26, 2023, of the 10,809 DPIIT-recognised startups that applied for the exemption, only 8,066 startups were exempted.

In its latest attempt, the IT department made changes to Rule 11 UA, introducing several valuation methods, to provide more clarity and flexibility to startups and investors in the form of:

- Five New Valuation Methods: Non-resident investors now have access to five valuation methods, including the Comparable Company Multiple Method, Probability Weighted Expected Return Method, Option Pricing Method, Milestone Analysis Method, and Replacement Cost Method. This expansion aims to cater to the diverse needs of investors.

- Valuation For Shares Issued To Non-Residents: The price of equity shares issued to non-resident entities can now be considered the Fair Market Value (FMV) for both resident and non-resident investors, subject to certain conditions. This provision seeks to streamline the valuation process for cross-border investments.

- Price Matching For VCs: Price matching for resident and non-resident investors is now available for investments made by Venture Capital Funds or Specified Funds. This change aims to create consistency in valuations across different investor categories.

- Valuation Methods For CCPS: According to the notification, the valuation of CCPS could also be based on the FMV of unquoted equity shares.

- Safe Harbor Provision: To provide some leeway, a safe harbour of 10% variation in value has been introduced.

While these changes are seen as positive steps, they do not resolve the angel tax issue, as several founders and investors pointed out.

So, What’s The Long-Term Solution?

The startup founders that Inc42 spoke with agreed that the existing angel tax regime needs a further tweak.

The founding partner of VC fund 3one4 Capital, Siddarth Pai, suggested the dematerialisation of securities to address the regulator’s black money concerns, standardisation of the scrutiny process and upgradation of the computer-assisted scrutiny selection (CASS) system in accordance with the startups as some of the key reforms needed in the long run.

Further, the industry stakeholders want:

Increase In The Exemption Limit To INR 80 Cr: Speaking of quick fixes, some founders want the current angel tax exemption limit to increase to INR 80 Cr from the current INR 25 Cr to encompass a more extensive range of startups.

Dematerialisation Of Security: Dematerialising security would enhance traceability and enable the identification of ultimate beneficial owners (UBOs). It would also capture secondary transfers, which currently go unrecorded. This will help combat the issue of lack of transparency among private companies.

Standardisation Of The Scrutiny Process: The scrutiny process should be made more objective and less reliant on subjective judgments by tax officers. Guidelines should be established to differentiate legitimate business cases from money laundering. Quality of spending should be considered.

Updation Of The CASS System: The CASS system needs an update to prevent companies with losses and share premiums from receiving notices automatically. Startups often operate with losses during their growth phase. Better triggers and interlinking is required.

Resolution Of Issues Under Section 68: Section 68, although less discussed than Section 56(2)(viib), is equally significant. Recent cases involving TravelKhana and BabyGoGo, whose bank accounts were emptied due to Section 68, have sent shockwaves throughout the Indian startup ecosystem.

Section 68 aims to delve deeper into fraudulent transactions and is unconcerned with valuation or premium. Instead, it seeks to establish the identity, creditworthiness, and genuineness of transactions for each investor.

While the aforementioned solutions can go a long way in addressing the angel tax issue, Somdutta Singh, the founder and CEO of Assiduus Global, an angel investor, and an advisor to the Government of India, believes that a comprehensive and clear definition of startups needs to be floated, taking into account factors like revenue, age, and scale. This will help in distinguishing genuine startups from other entities.

Seconding this, Ipsita Agarwalla, senior member of International tax practice and funds formation practice at Nishith Desai Associates averred that considering that valuation rules have been notified by the government and valuation will be undertaken by SEBI-registered merchant bankers, clear instructions should be given to tax authorities to not raise questions on valuation.

Additionally, simplifying the angel tax provisions and providing exemptions or deductions based on certain criteria can reduce the burden on startups and encourage investment.

Industry experts also believe that similar improvements can be made to address issues related to Section 68. Finally, regular communication and coordination between tax authorities, the DPIIT, and startups can help in addressing concerns promptly and ensuring compliance without undue scrutiny.