The latest notification pertaining to Rule 11UA does not resolve the core issue of disputes arising from projections versus actual valuations, say valuation experts

Despite recent regulatory changes, the issue of angel tax continues to impede the growth of Indian startups, leaving founders and investors in a state of uncertainty.

The conflict between income tax regulations and FEMA adds complexity to the angel tax problem, highlighting the need for streamlined processes and simplified regulations.

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

Despite several notifications, reforms, and assurances from the central government, the issue of angel tax continues to plague Indian startups. The Finance Act of 23 only exacerbated the problem, leading to mounting concerns within the startup community.

In the words of Kanwal Rekhi, managing director of Inventus Capital Partners, “Who is advising the Indian finance ministry? I thought the government was promoting startup activity. What happened to Startup India?”

Angel tax, governed primarily by Section 56(2)(viib) and Section 68 of the Income Tax Act, poses a significant threat to startups. Section 56(2)(viib) deems investments in startups above fair market value as “income from other sources,” making them liable for taxation at corporate tax rates.

Conversely, Section 68 acts as a safeguard against the misuse and distribution of undocumented funds. It mandates a uniform tax rate of 60%, which is further augmented by additional surcharges and cess, culminating in an effective tax rate of around 78%. This section also opens the door for potential penalties, placing both investors and startup founders in a position of significant risk.

The situation becomes even more dire when one considers the implications of receiving intimation letters under Section 56(2)(viib) and Section 68. These letters from tax authorities signal trouble for startups, adding to the woes of founders.

This stringent taxation regime has created a climate of uncertainty and apprehension among the startup community. Despite the government’s efforts to address the issue, startups continue to grapple with the challenges posed by angel tax.

One ecommerce startup founder, whose angel tax case has been pending since 2016, expressed frustration, stating that while notifications and assurances abound, startups are still waiting for a definitive solution. The founder has now moved to Dubai and is working to launch a gaming startup.

Section 68 grants substantial power to assessment offices (AOs), which can become problematic for startups. According to Siddarth Pai, founding partner and CFO of early-stage fund 3one4 Capital, the issue of the tax officer comparing projections used in the valuation report to the actual performance of the company and disregarding the valuation report due to deviations still exists. This is the core issue of Angel Tax.

The uncertainty surrounding whether investments will be treated as income from other sources or whether startups can justify the source of their funds has created a cloud of uncertainty, stifling the growth and innovation that the government intended to promote through initiatives like Startup India.

New Angel TaX Rules But Old Problems

Despite the government’s assurances in the past and changes in angel tax implementation policies, startups have not been able to recover angel taxes claimed by the Income Tax Department even after seven years, as in the case of the founder highlighted above.

In its latest attempt, the IT department made changes to Rule 11 UA, introducing several valuation methods, to provide more clarity and flexibility for startups and investors. Here’s what the new rules bring in:

a) Five New Valuation Methods: Non-resident investors now have access to five additional valuation methods, including the Comparable Company Multiple Method, Probability Weighted Expected Return Method, Option Pricing Method, Milestone Analysis Method, and Replacement Cost Method. This expansion aims to cater to the diverse needs of investors.

b) Valuation For Shares Issued To Non-Residents: The price of equity shares issued to non-resident entities can now be considered the Fair Market Value (FMV) for both resident and non-resident investors, subject to certain conditions. This provision seeks to streamline the valuation process for cross-border investments.

c) Price Matching For VCs: Price matching for resident and non-resident investors is now available for investments made by Venture Capital Funds or Specified Funds. This change aims to create consistency in valuations across different investor categories.

d) Valuation Methods For CCPS: According to the notification, the valuation of CCPS could also be based on the FMV of unquoted equity shares.

e) Safe Harbor Provision: To provide some leeway, a safe harbour of 10% variation in value has been introduced.

While these changes are seen as positive steps, they do not resolve the angel tax issue, as several founders and investors pointed out.

Nitesh Mehta, partner, M&A Tax and Regulatory Services at BDO India, highlighted that the notification addresses some aspects of the problem but does not resolve the core issue of disputes arising from projections versus actual valuations.

For others, the amendments bring some feel-good factors but fall flat in their attempt to bandage the angel tax wounds.

N.A. Shah Advisors’ partner Diana Mathias emphasised that the changes do not address all the issues, particularly the restrictive definition of startups and VC funds. A majority of Indian startups do not meet the criteria for exemptions, creating challenges for those in need of continuous funding. Additionally, the prescribed shell capital limit adds further complexity and restrictiveness to the startup exemption, which we highlighted in our past coverage of angel tax.

Mayank Singh, cofounder of Delhi NCR-based edtech startup Campus 365, pointed out potential concerns arising from differing fair market value calculation methodologies.

These concerns include complexity, compliance challenges, valuation discrepancies, and subjectivity, which can lead to a potential impact on investor confidence, operational delays, and the possibility of legal challenges. To mitigate these concerns, clear and consistent guidelines are essential.

Furthermore, despite adding the valuation methods, IT department’s assessment officers (AOs) reportedly still have the authority to question the valuation. AOs can also send notices to founders asking for the income tax returns of shareholders for the last three years under Section 68.

This does not change the fact that AOs are likely to consider the premium amount as income from other sources and impose the angel tax if the startups have not filed Form 2 (more on this below).

Startup Valuation Caught Between FEMA and IT Rules

Pai averred that startups need to get two different valuation reports for investments by Indian investors and non-Indian investors, from a tax perspective. Due to this, a company has to get up to four valuation reports from three different valuers for three different sets of laws (Company’s Act, Income Tax Act & FEMA)

The Indian capital is a minority in large-stage funding rounds. Thus the matching provision of the new notification may not have as much of an impact as expected. This also leads to illogical situations wherein if an AIF invests INR 100 Cr and a foreign investor invests INR 150 Cr, only INR 200 Cr would be exempt from angel tax despite the remaining INR 50 Cr coming from the same investor whose investment is partly exempt, Pai explained.

The conflict between the Foreign Exchange Management Act (FEMA) and income tax regulations further complicates the issue of angel tax.

FEMA regulations require funds to be infused at a price higher than fair value, while income tax regulations suggest the opposite. This contradiction has created confusion and administrative burdens for startups and investors, added N.A. Shah’s Mathias.

Moreover, the notification has introduced a mechanism for valuing Compulsorily Convertible Preference Shares (CCPS), which was previously left to merchant bankers. While this provides some clarity, it also adds complexity to an already complicated system.

Non-resident investors face additional challenges as they must navigate different valuation principles and mechanisms under the same regulation. This adds complexity to transactions, making it challenging for non-resident investors to comply with all the requirements.

Given the uncertainty surrounding their eventual valuation, many startups rely on convertible instruments for fundraising. However, this introduces a new layer of complexity, as questions arise regarding whether the provisions will be triggered when these instruments eventually convert into equity shares.

If market conditions sour and the company’s valuation falls, startups are very likely to face unexpected closures. This existential uncertainty creates an additional burden for startups and investors alike.

The Unending Saga of Angel Tax

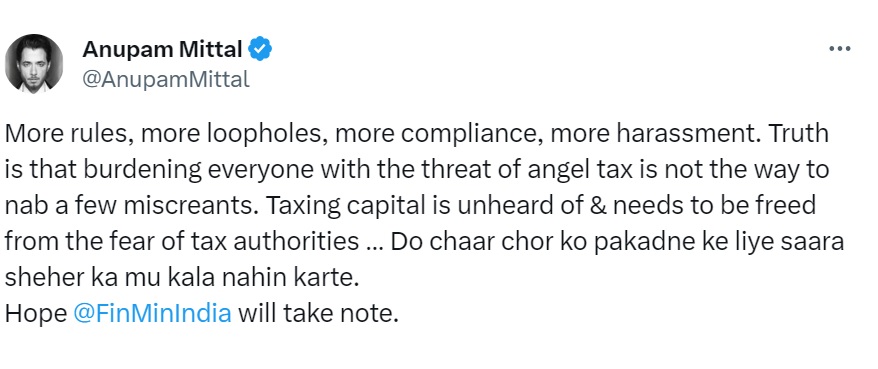

Despite previous efforts and announcements by the Indian government, the angel tax issue continues to haunt startups. Commenting on the latest notification, entrepreneur and angel investor Anupam Mittal recently tweeted, “More rules, more loopholes, more compliance, more harassment. Truth is that burdening everyone with the threat of angel tax is not the way to nab a few miscreants…”

This is indeed the case for many startups. Srinivas Varadarajan, founder and CEO of Mysuru-based Vigyanlabs Innovations, has been embroiled in angel tax issues since 2016. His company’s income tax returns claim for the fiscal year 2016 remains unresolved till date. The IT department’s decision to adjust the angel tax amount against the outstanding amount has only added to Varadarajan’s frustration.

“We went for an appeal. And, for the last seven years, it has been on hold and unresolved. Since 2019, after COVID-19, all the income tax return claims have been pending. FY2016 was under appeal but why are you holding the ITR claim for other years?” asked Varadrajan.

Take another case of Gurugram-based Planet GoGo. In its ITR for FY2016, the startup claimed a loss of INR 33 Lakhs. However, AOs held that Planet Gogo sold shares to two entities NBM Investment Fund, a non-resident company and HT Digital Media Holdings with very high premiums and received INR 24,37,500 from each of the investors.

The AO did not accept the DCF valuation method used by the company and added the total amount of INR 48,63,880 as income from other sources under Section 56(2)(viib).

Earlier this year, Planet Gogo won the case at the Income Tax Appellate Tribunal, Delhi.

Pushpinder Singh, founder and CEO of Travelkhana, shared a similar experience, recounting that his startup has been awaiting a hearing since November 1, 2019, with no resolution in sight. Despite the government’s introduction of a faceless scheme, startups like Travelkhana have faced difficulties in settling disputes with the income tax department.

Similarly, Nikunj Bubna, another founder, highlighted that his exemption from angel tax issues is still pending, even after six years. Despite appealing to the Commissioner of Income Tax (CIT) three years ago, the case has yet to be listed for a hearing.

The income tax department’s handling of these cases has been a source of frustration for startups. Most startups with pending cases report a lack of clarity and transparency in the process. The delays in processing cases have only added to the burden of businesses already grappling with the challenges of angel tax.

Angel Tax Exemption Form: My Way Or Highway

Now, let’s look at the process of claiming exemptions.

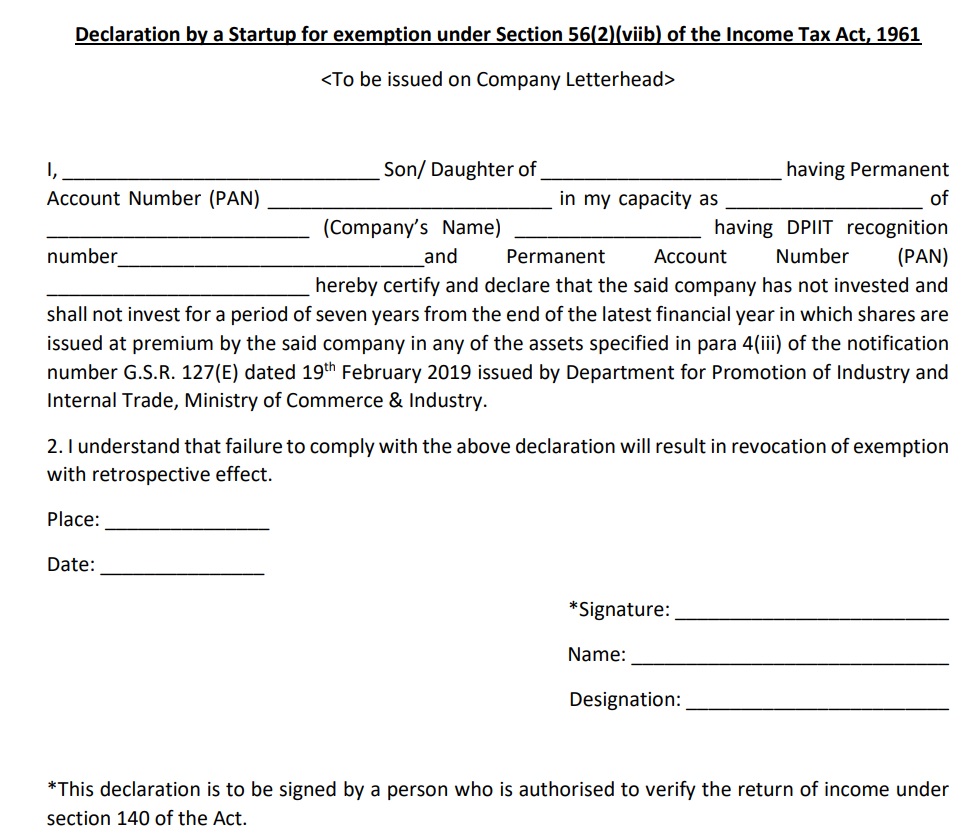

After a significant uproar in 2018 and 2019, the Indian government announced the exemption of angel tax for startups in 2019.

However, it asked startups to file Form 2, a declaration letter, to be exempted from angel tax.

According to the declaration, a startup seeking exemption from angel tax must fulfil the following conditions:

- It must be recognised as a startup by the Department for Promotion of Industry and Internal Trade (DPIIT)

- The aggregate amount of paid-up share capital and share premium of the startup after issuance does not exceed INR 25 Cr, excluding non-residents and VC funds.

- The startup will not establish any subsidiaries for the next seven years.

- The startup will not provide loans or advances, including salary advances to its employees.

- The startup has not invested in any assets, such as buildings or land, beyond what is used by the startup and so on.

If a company is found violating any of these terms, it will be liable to pay the angel tax retrospectively. Naturally, the criteria for these exemptions are hard to maintain if a company is looking to grow and scale.

“You are not even allowed to buy a car that is costier than the INR 10 Lakhs threshold” said a founder. “How can we file the declaration form and put the entire expansion plans on hold? Which investor or VC will invest, if we don’t have a good expansion plan,” he asked.

Until February 2021, only a small percentage, roughly 8% (3,612 startups) out of the then 44,000 recognised startups, filed Form 2 to avail exemptions under the angel tax.

Mathias pointed out that startups typically expand through acquisitions, enabling them to enter new markets and reach new customers. As soon as this happens, the startup exemption is again revoked. “These conditions are challenging to comply with, and genuine startups still in the growth process will continue to face scrutiny from income tax authorities regarding their pricing and valuation mechanisms adopted in hindsight,” she added.

What’s The Way Forward

Startup founders are fast becoming disillusioned with the situation, seeing it as a threat to ‘ease of doing business’ in India.

One founder quoted earlier lamented, “This is not ease of doing business. This is about the ease of killing business.”

Introduced in 2012, Section 56(2)(viib) of the Income Tax Act was originally intended as an anti-abuse law to discourage shell companies and curb the circulation of black money. However, the imposition of angel tax on startups raises questions about the government’s motivations.

It appears to be a case of government revenue taking precedence over the growth and success of startups.

Angel investors argue that the government already has access to detailed information about their finances through income tax return filings. They contend that if the same money is being invested in startups, it should not be treated as unaccounted for and subject to taxation. Matching these ITRs with the investment claims of startups is being suggested as a straightforward solution to this problem.

3one4 Capital’s Pai recently published a playbook highlighting possible responses that startup founders can provide when faced with notices under Section 56(2)(viib) or Section 68. This guidance aims to simplify the process and reduce the burden of justifying the source of funds.

BDO’s Mehta added that a single window clearance system could expedite tax validation for startups during tax holidays. Additionally, the government should consider market practices related to startup funding when framing laws, ensuring that tax requirements align with business needs.

The issue of angel tax continues to be a pressing concern for Indian startups more than half a decade after the problems were first pointed out.

Despite some regulatory changes, there is still a need for comprehensive reform to address the challenges faced by the startup community. The conflict between income tax regulations and FEMA, coupled with the uncertainty surrounding convertible instruments, further complicates the situation.

Startups and investors remain stuck in a web of bureaucratic processes and administrative burdens.

Ultimately, resolving the angel tax issue is not just a matter of taxation but a reflection of the government’s commitment to fostering innovation and entrepreneurship in India, and an environment where startups can thrive without looming tax demons.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.