While Nykaa's INR 5.2 Cr profit in Q2 FY23 is 300% higher than Q2 FY22, the picture is somewhat different when viewed on a sequential or QoQ basis

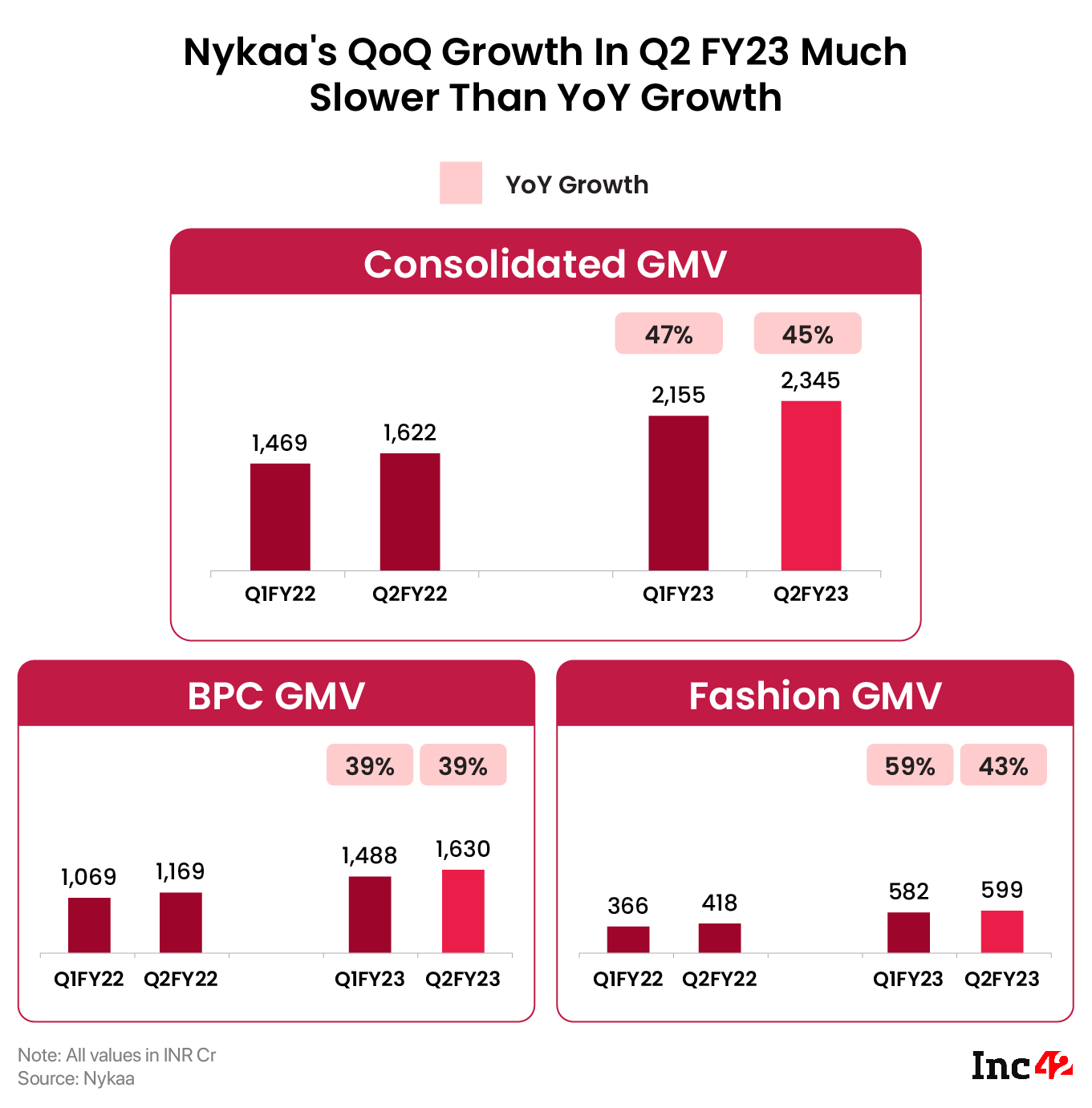

For instance, the total GMV grew 45% YoY to INR 2,345.7 Cr in the reported quarter, but on a QoQ basis, the GMV only grew 8% from INR 2,155 Cr

The global macroeconomic slowdown and rampant inflation has eaten into Nykaa’s business on both the supply and demand side

It’s a tough time to be an ecommerce marketplace in 2022 — even for a giant such as Nykaa, which has been a mainstay in the Indian beauty shopping for many Indians.

If the public listing last year brought in many plaudits for Nykaa founder Falguni Nayar, there’s a bitter reality settling in now. Growth has been tough and the company’s financial performance has not been as robust as one might have expected after the proceeds from the IPO.

Nykaa’s Quarterly Growth Extremely Slow

Nykaa reported a net profit of INR 5.2 Cr in Q2 FY23. While this is a 300% jump when compared to Q2 FY22 (prior to the public listing), the picture is somewhat different when viewed on a sequential or QoQ basis.

Profit growth is almost flat when compared to the quarter ended June, when it had a profit of INR 5 Cr.

This pattern of high YoY growth and marginal QoQ gains continues when it comes to revenue and GMV too.

First the GMV comparison: Total GMV grew 45% YoY to INR 2,345.7 Cr in the reported quarter, but on a QoQ basis, the GMV only grew 8% from INR 2,155 Cr.

Now the operating revenue: Nykaa reported a healthy 39% YoY growth in operating revenue to INR 1,230.8 Cr but the quarter-on-quarter comparison shows revenue has only increased by 7% from INR 1,148.4 Cr in Q1 FY23.

The GMV of the beauty and personal care segment rose 39% from Q2FY22 to INR 1,630.1 Cr in Q2FY23, and this segment has seen the highest QoQ GMV growth at 9%.

Nykaa Fashion saw a 43% YoY increase in GMV to INR 599.1 Cr, but the sequential growth is again very underwhelming with just 2% quarter-on-quarter improvement.

One positive for the company is the overall improvement in QoQ EBITDA (33%). EBITDA margin expanded 96 basis points QoQ, thanks to a mix of owned brands, higher ad income and marketing efficiency, according to the company.

Economic Slowdown, Inflation Bites Nykaa

The overall YoY comparison paints a rosy picture, while the sequential or quarterly growth is tepid. So what exactly is ailing Nykaa this year?

As per Nykaa founder and CEO Nayar, the company’s digital marketing costs for the fashion business were slightly higher than it was during the pandemic period, which has resulted in its marketing costs remaining at Q2 FY22 levels.

The company also added nine new retail stores in the July-September quarter, and has a total of 121 stores in 53 cities. The retail expansion coincided with Nykaa adding more fulfilment centres in Q2 FY23.

Speaking about the transition from warehouse-based distribution, Nayar said, “We have seen fulfilment costs go up. Nykaa decided to get closer to its customers, and instead of four big warehouses, we have fulfilment centres in 15 cities now to reduce the distance.”

Nykaa revealed that fulfilment costs also improved driven by regionalisation strategy, but was partly offset by inflation and macroeconomic pressures.

The global macroeconomic slowdown has eaten into Nykaa’s business and margins as well. Nayar added that the company is considering restructuring its business to reduce inflationary pressure, which involves slower hiring as employee costs are rising even in this bearish climate.

Given that it is a marketplace, Nykaa is facing headwinds on both demand and supply due to rising inflation. For instance, brand partners, particularly those who import products into India are seeing their own costs rise, which are being passed on to consumers in the form of lower discounts or simply higher pricing.

On the demand side, the higher inflation has slowed down consumer spending considerably. Considering the lower number of ecommerce shoppers during the peak festive season in 2022, as well as the lower average spend, it’s not just Nykaa which has had to deal with slower growth in 2022.

Fashion is one vertical that should have grown healthily in the pre-festive season (August-September), but analysts have been disappointed with the growth in this category. “Orders grew just 8% YoY and declined 7% QoQ. GMV grew 43% YoY, but growth in net realisations was much lower at 20% on account of higher returns,” Jefferies said in its latest coverage on Nykaa.

Will Nykaa Stock Bounce Back After Crash?

Worryingly, Nykaa has exhausted INR 233 Cr from the INR 234 Cr it had earmarked from the IPO proceeds towards customer acquisition and retention. In other words, it will have to use the revenue generated to drive growth.

That’s the ideal scenario, but one can also expect a further rights issue in the near future, especially after the lock-in period for pre-IPO investors expires on November 10, 2022.

As we reported earlier this week, analysts expect the positive numbers in Q2 to arrest some of the sell-off pressure on Nykaa’s stock.

Last week, Nykaa shares touched a new record low of INR 975.50, but since then the stock has seen a rally.

The company’s current market cap is INR 54,744 Cr, which fell to INR 46,292 Cr last week, when it hit the all-time low. The company has lost a market cap of INR 75,857 Cr since listing, from an all-time high of INR 1.22 Lakh Cr.

Nykaa had one of the best debuts among the new-age Indian tech stocks last year, with its investors witnessing almost 100% return on their investments. But this can be a double-edged sword — the higher returns in a weak economic climate could trigger a fresh wave of sell-offs from investors after the lock-in expiry, according to brokerage firm JM Financial.

JM said that since 12%+ shareholding is currently on 100x returns, these investors could look to diversify their portfolio which might weigh down Nykaa’s stock.

Kotak Securities highlighted the increase in expenses in its report post the Q2 financials, pointing out the above-expectation QoQ increase in employee costs, because of Nykaa’s new initiatives, including SuperStore for B2B ecommerce, retail expansion and bulking up technology team.

The Mumbai-based company also entered into a strategic alliance with the Middle East-based Apparel Group to build an omnichannel beauty retail platform for the Gulf market.

“New businesses like eB2B [SuperStore] are being set up and will need business development executives for sales. There is also an additional element of selling commission from third party platforms, warehouse outsource manpower cost, beauty advisor fees, and warehouse operation management expenses,” Kotak added.

On the flipside, analysts also believe that any short-term dip could see retail and institutional investors building long-term positions by accumulating shares.

Can Nykaa Edge Out Competition?

Despite being around for more than a decade, Nykaa’s stronghold on the beauty ecommerce vertical is slipping. With the entry of hundreds of D2C brands, house of brands and rival vertical marketplaces, Nykaa is no longer the go-to destination for beauty shopping.

With a total of $2.1 Bn funding, FMCG D2C brands, including BPC brands, top the current list of the total number of funded players in the overall D2C market, as per an Inc42 report.

As the number of D2C brands have increased in the Indian market, Nykaa has also started focusing more on offline retail as highlighted by Nayar during the investor presentation yesterday. It is also adding new verticals to compete with the host of players such as its Nykaa Man and Nykaa Fashion apps, which are intended to increase Nykaa’s share of fashion and beauty purchases across segments.

Nykaa, which has private labels and a marketplace, competes with several players across the ecommerce beauty industry. The likes of WOW Skin Science, Mamaearth (which turned profitable in FY22), Sugar Cosmetics, mCaffeine, Plum Goodness and others are not just competitors but also customers for Nykaa. This is also why Nykaa is prominently highlighting its owned brands in its presentation for Q2.

On the marketplace side, the likes of Purplle and MyGlamm are looking to replicate Nykaa’s multi-pronged approach.

The latest launch was GLOOT, marking Nykaa’s foray into the men’s innerwear and athleisure category. It acquired Dot & Key, Earth Rhythm, Kica and Pipa Bella to boost the owned brands mix on its marketplace, which are expected to drive the margins growth in the quarters to come.

One also cannot ignore the competition from Tata Digital (TataNeu, TataCliq, BigBasket), Reliance-owned Ajio and Flipkart’s Myntra which has made major inroads into the beauty vertical, besides fashion. Tata Digital is reportedly planning a beauty and cosmetics vertical marketplace, which is likely to throw new challenges to Nykaa.

In its report, brokerage ICICI Securities pointed out the increasing competition for Nykaa, which might necessitate changes in its omnichannel mix. “It will have to go more mainstream to drive this growth (tougher decisions about brand stretch along the way).”

Jefferies too mentioned “rising competitive intensity from horizontal as well as vertical players” as a potential negative trigger for Nykaa in the near-term.

Despite these challenges, most analysts are optimistic about Nykaa turning around the relatively low EBITDA and profit margins in the coming quarters. Nykaa is banking on its marketing efficiency, growing retail presence, as well as the momentum for owned brands to pull up the profits in the next two quarters of FY23.

However, it remains to be seen whether the underwhelming reception for ecommerce festive season sales in 2022 will have a negative impact on Nykaa’s performance in the ongoing quarter.

The feeling is that the next quarter’s financial performance will be the one that makes or breaks Nykaa’s future.