ZestMoney’s eight-year journey has come to an end after the management shocked its employees by asking them to stay at home from December 7

Sources say that ZestMoney was relying on an internal funding round, which did not materialise

ZestMoney’s revival plan of focussing on digital EMI and small-ticket loans failed on the back of the RBI’s tightened lending regulations

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

Founders quitting, a failed acquisition bid, regulatory hurdles and a severe slowdown in the core BNPL business — ZestMoney has been on a downward spiral all year, which has now culminated in the startup shutting down.

The 8-year-old startup has crumbled from a valuation of $455 Mn and nearly 150 employees are now staring at an even more uncertain future.

Employees were informed about the impending shutdown at a town hall meeting on December 5, 2023, which left many perplexed, especially when the promotions were handed over twice to a majority of the staffers this year (in June and October).

Several of these employees told Inc42 that the surprise meeting was called to inform the employees to sit at home starting December 7, except for a few who would help pack up.

Although, as per our sources, there were no indications of operations shutting down until last month, the problems in the company had already been highlighted by the fact that ZestMoney’s cofounders Lizzie Chapman, Priya Sharma and Ashish Anantharaman stepped down from their respective roles in May, as the company battled for survival.

ZestMoney’s Last Ditch Attempts

Founded in 2015 by Chapman, Sharma and Anantharaman, ZestMoney raised more than $125 Mn in debt and equity funding since its inception. In its last funding round (in September 2021), the company raised $50 Mn at a valuation of $455 Mn. At the time, India was riding high on the BNPL wave, but a slew of regulatory changes since 2022 have impacted many players in this segment.

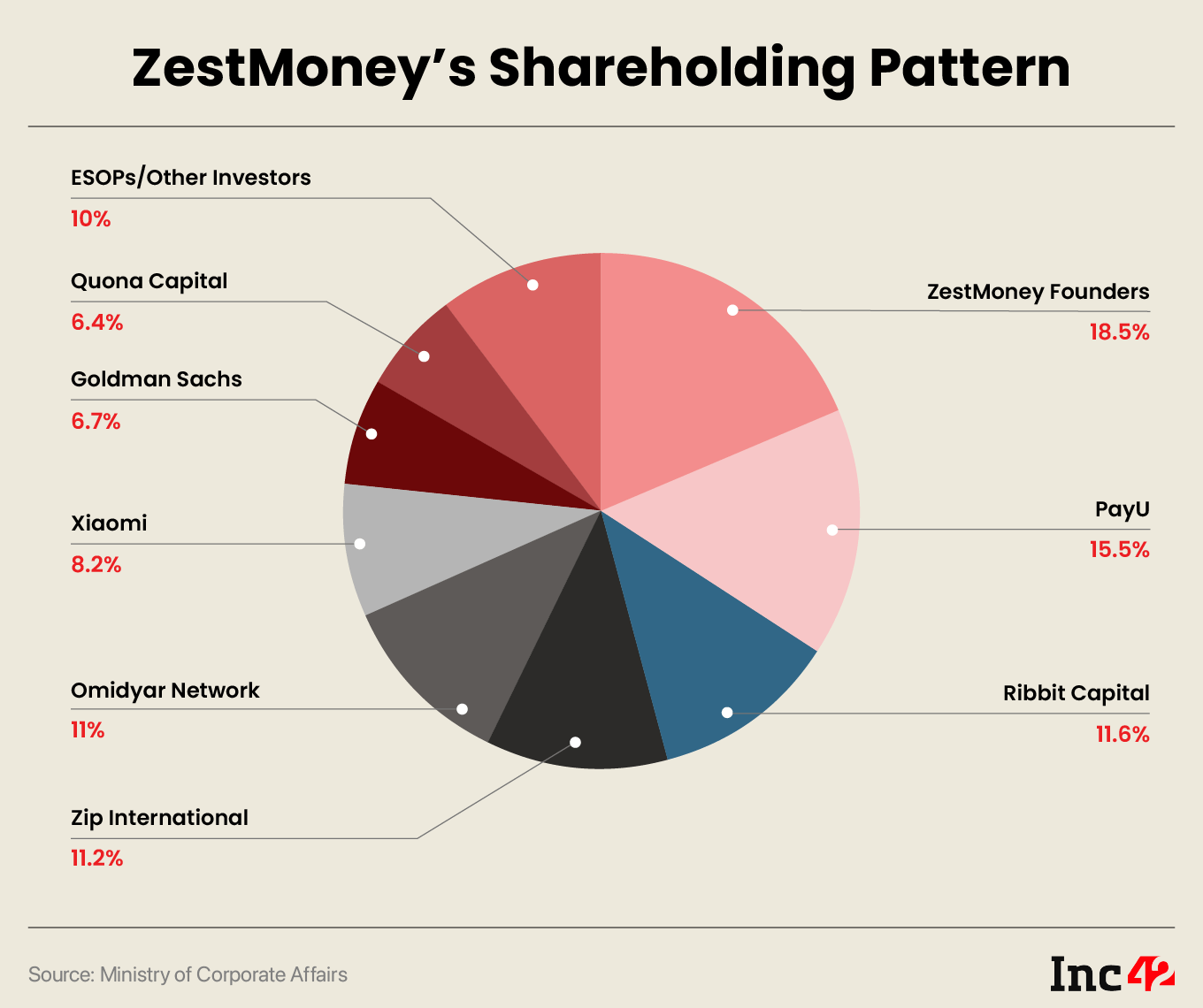

For the last two years, ZestMoney was in talks with PhonePe for an acquisition, which did not materialise and soon after the founders quit, even though they hold a combined stake of 18.5% in the company.

Close on the heels of the failed acquisition talks in May this year, the company said it would have new leaders at the helm to replace the outgoing founders — vice president of finance Mohit Chhajer, chief banking officer Mandar Satpute, and senior VP and head of growth Abhishek Sharma. It also claimed to be in the process of raising funds to stave off any shutdown.

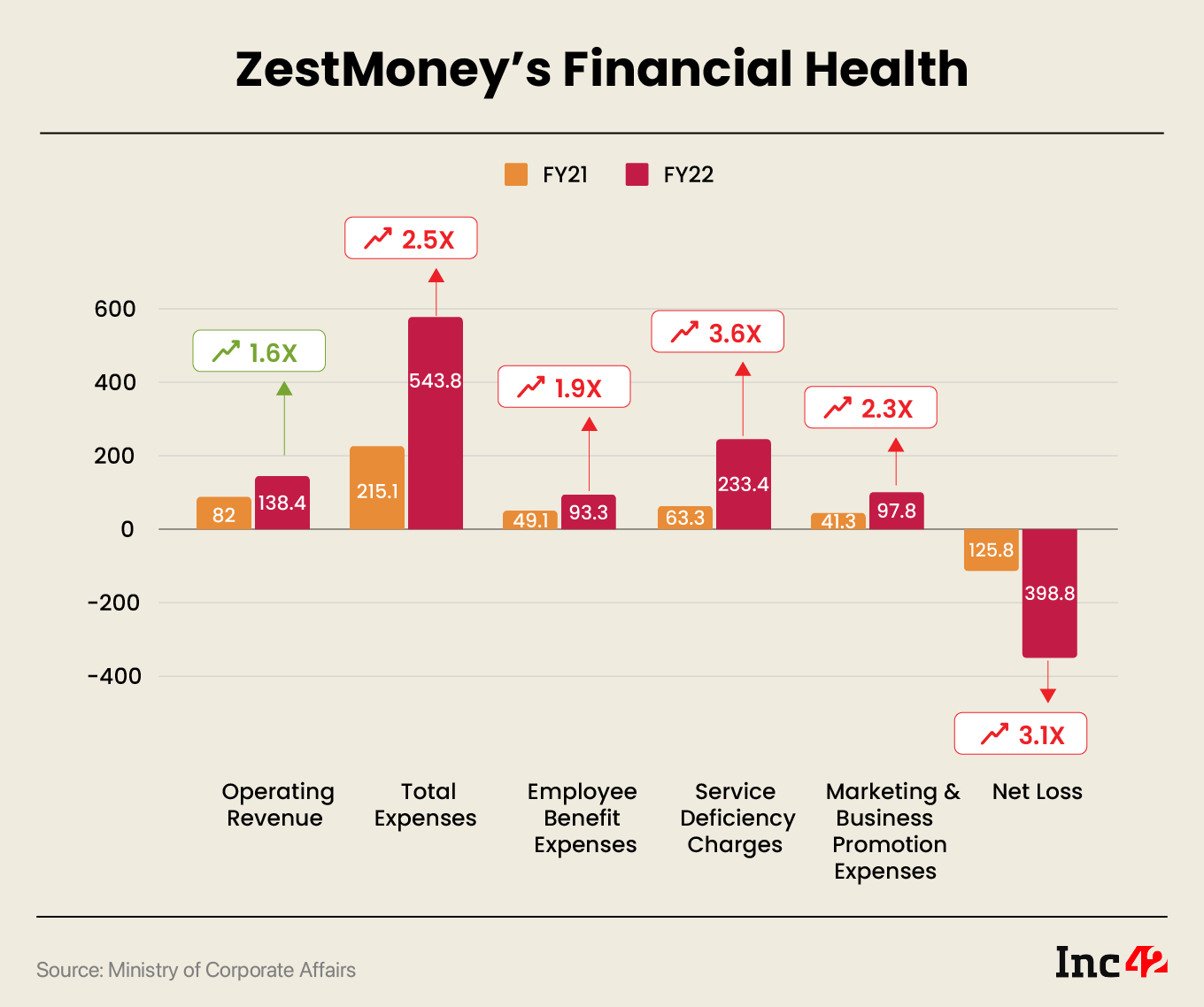

As the funding crisis deepened within the startup, ZestMoney announced layoffs in April 2023, impacting 20% of its workforce. ZestMoney retained nearly 150 employees in product, tech, finance and HR divisions and culled infrastructure costs.

The company was also in talks to raise $4 Mn – $5 Mn from existing investors Quona Capital, Omidyar Network and Zip.

ZestMoney looked to revive its business model with digital EMI (BNPL) and personal loans as two core products in May this year. However, both models were severely hit by RBI’s digital lending guidelines, PPI lending rules and the recent changes in risk weights for unsecured credit.

Meanwhile, two independent sources privy to the developments at ZestMoney said that the new funding round did not materialise particularly because of the changes around risk weights for banks and NBFCs lending to digital lenders.

The RBI’s new guidelines on risk weight for unsecured loans were floated in November 2023 and have caused some panic among fintech startups. But in ZestMoney’s case, this disruption proved to be the final fatality.

“VCs in fintech have been watching the evolving regulations in India very closely and are wary that many business models would be upended due to the strict norms by the RBI on lending. The investors pulled the plug in ZestMoney’s case because the business model was solely surviving on small-ticket BNPL purchases and personal loans now,” a source said.

Sources further informed Inc42 that former CEO Chapman and CTO Ananth are already in the process of launching a new fintech venture and have hired various executives and senior employees from ZestMoney for the new startup.

Meanwhile, the third cofounder, Sharma, is looking to invest in startups, as per sources.

ZestMoney Suffers Regulatory Wrath

“The focus for the business going forward is on core digital EMI and personal loan products. We are not doing any SaaS and we have stopped the insurance business,” — ZestMoney said in a statement in May 2023.

The past six months have seen ZestMoney’s digital EMI product take a beating — not only from consumers but also from key partners like payment aggregators, ecommerce marketplaces and NBFCs.

ZestMoney’s largest investor, Prosus, pulled the plug on the startup’s partnership with Prosus-owned PayU for digital EMI services on ecommerce marketplaces.

Further, the RBI’s tightening regulations on stricter underwriting models, sufficient disclosures and capping the first loss default guarantee (FLDG) at 5% have also made it costlier for digital lenders such as ZestMoney to raise capital from banks and NBFCs.

Although PayU and ZestMoney told us earlier that they were working to resume the digital EMI partnership, the companies failed to walk the talk. Without one of its major partners, the digital EMI vertical was floundering.

The last straw to break the camel’s back, in this case ZestMoney’s, was the RBI’s unsecured credit rules that were announced last month. The RBI increased the weightage for banks and NBFCs when it comes to consumer loans, which means these lenders will have to put aside more capital as risk mitigation measures.

It is widely believed that these changes will lead to an increased borrowing rate for digital lenders. The changes directly impact the personal loan segments for digital lenders, which offer collateral-free unsecured loans.

NBFCs and banks have now become more wary of tying up with digital lenders for small-ticket collateral-free loans. This spelt the end of ZestMoney’s partnership with banks and NBFCs like Aditya Birla Finance, Tata Capital and ICICI Bank.

The ZestMoney Shutdown Is Just The Tip Of The Iceberg

Fintech experts believe that tightened regulations have put NBFCs and banks on alert, and many are closely examining their partnerships with digital lending platforms.

The explosive growth in the personal loans segment through such platforms has alarmed the central bank for several years now. It has urged banks and NBFCs to be more responsible about lending to digital platforms. Besides, there has also been pressure from civil rights groups to stamp out predatory lending and harassment in recovery practices.

By increasing the risk weightage, the RBI has only complicated these partnerships. There was speculation about the changes in risk weights impacting the BNPL business of the likes of Paytm, which the fintech giant denied this week.

But, generally speaking, fintech companies operating in small-ticket personal loans and BNPL spaces are expected to face a lot of headwinds in the next few months.

The shutdown of ZestMoney is an example of how tightening regulations can completely disrupt operations for fintech startups. Several fintech startups have branched out to digital lending in recent years and the regulatory changes threaten to disrupt their operations too.

In August this year, two major consumer internet giants — Flipkart and Swiggy — announced their lending foray. While Swiggy has announced its entry into the co-branded credit card segment, Flipkart’s eyes are on the personal loan business.

Google Pay has stepped up its partnerships for personal and merchant loans. Another big player, CRED, jumped into lending with a BNPL product in 2022, and now the fintech unicorn is looking at expanding and casting a wider net for its lending products.

The market is flooded with digital lending platforms, but this is perhaps exactly why the RBI has decided to increase the risk weights to avoid a potential catastrophe in the long run. As ever, fintech startups are realising that regulations are the reality for this sector and not an exception.

And in some ways, startups are also coming to terms with the fact that simply turning on the digital lending tap may not be enough. In that sense, ZestMoney is a cautionary tale for the fintech ecosystem.

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.