LIC’s mega IPO closed for subscription on May 9, and the stock will make its stock market debut on May 17

The success of the LIC IPO and its valuation will present a big opportunity for the insurtech sector in the country as the insurance market is widely underpenetrated

LIC can partner with insurtech players for their tech prowess and product innovation

Undeterred by the weak investor sentiment, state-owned Life Insurance Corporation (LIC) is set to make its stock market debut on May 17.

The investor response to the INR 21,000 Cr initial public offer (IPO) of LIC was positive as the issue got subscribed 2.95 times.

“The LIC offer was long-awaited and largely had institutional backing…so there is no surprise in the fact that the issue got subscribed,” said Tanushree Banerjee, co-head of research at Equitymaster.

LIC Vs New-Age Tech Startups

Investors’ enthusiasm towards the LIC offer, however, is not as overwhelming as it was for IPOs of new-age tech companies like Nykaa, Zomato, Paytm, among others.

The market conditions have vastly changed since November last year when some of these most-talked-about startups hit the market.

It is a different story that almost all of the new-age stocks are trading way below their listing prices. Paytm leads the pack with about a 70% fall from its listing price.

Right after the close of LIC IPO on May 9, Delhivery’s public offer will open on May 11. The SoftBank-backed new-age logistics company has launched an ad blitzkrieg ahead of its IPO even as other startups — Ola, Pharmeasy and boAt — have delayed their IPOs due to the high volatility in the market.

Foreign portfolio investors (FPIs) were net sellers for seven months to April 2022, pulling out INR 1.65 Lakh Cr from equities. FPIs withdrew INR 17,144 Cr from the Indian equity market in April.

The investor community and startup universe will keenly watch Delhivery’s performance, especially in the background of a disappointing decline in share prices of Zomato and Paytm.

But for now, all eyes are on LIC’s IPO, the biggest in India.

Importance Of Mega LIC Offer

LIC’s public offer assumes extra significance for the fledgling insurtech space in the country.

“LIC IPO is a game-changer not only for the equity markets but also for the insurance ecosystem in India,” said Nakul Zaveri.

Zaveri is a managing partner at Relativity Investment Management, a sustainability-focused private equity strategy, sponsored by the TRUST Group.

As digitisation presents great opportunities in the insurance sector, insurtech is well-positioned to attract funding from financial and strategic investors, Zaveri noted.

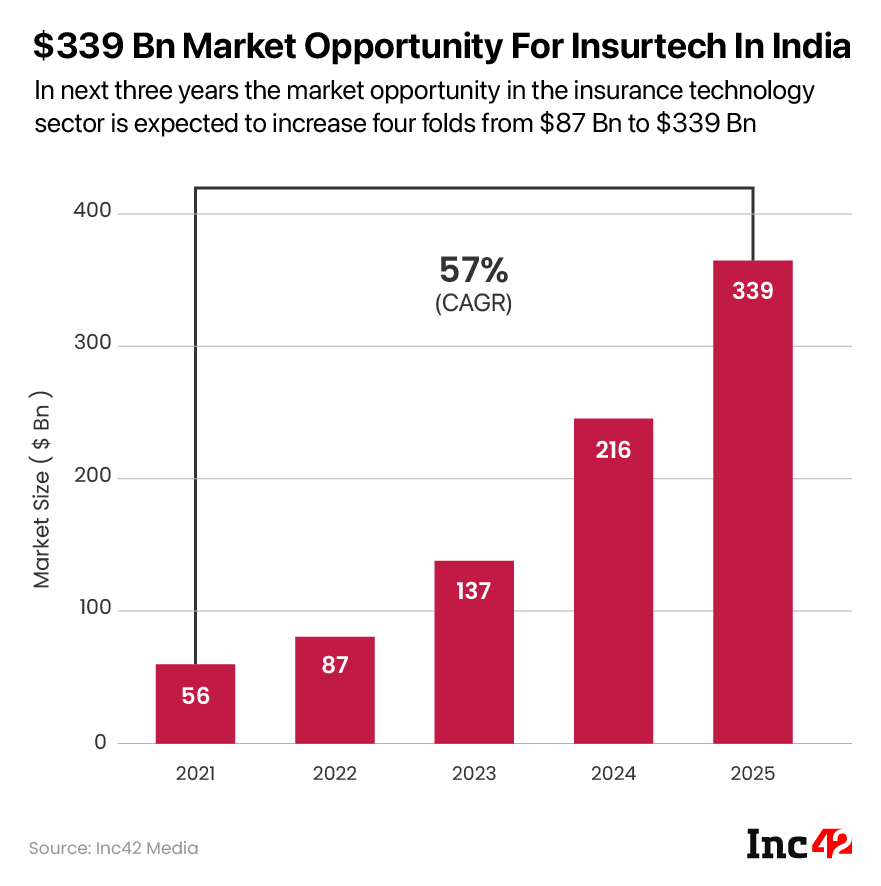

Insurtech players attracted about $820 Mn in 34 funding deals from venture capital entities and angel investors in 2021. The sector has three unicorns in this space including — Digit Insurance, Acko and newly listed PolicyBazaar.

LIC’s Digital Ambitions

Earlier this year, LIC unveiled its plans to have a separate vertical for digital operations after witnessing a fall in its market share in the previous two years. The state-run insurer, however, has a lot of catching up to do when it comes to digital play.

Insurtech players would be keenly watching LIC’s operations as a public-listed entity and how its external shareholders, with insurance industry experience, act as catalysts of change. Moody’s Investor Services says external shareholders can encourage LIC to negotiate wider online distribution agreements with third parties.

LIC has a pretty strong omnichannel distribution platform comprising individual agents, bancassurance partners, alternate channels (corporate agents, brokers and insurance marketing firms), digital sales, micro-insurance agents and point of sales.

Individual agents were responsible for sourcing 96.69%, 95.73%, 94.78% and 96.20% of new business premium (NBP) for individual insurance products in India during the financial year 2018-19 (FY19), FY20, FY21 and the first nine months of FY22, respectively.

LIC is the market leader by a long distance in the Indian life insurance industry. In FY21, its market share was at 64.1% in terms of gross written premium (GWP), 66.2% in terms of NBP, 74.6% in terms of the number of individual policies issued, and 81.1% in terms of the number of group policies issued.

Having said that, LIC and other legacy players greatly lack in product innovation.

“Since most of the startups have strong technology offerings, they can use the product gaps in legacy companies to their advantage,” said Banerjee.

The simple interpretation of this scenario is that the market is wide open for a partnership between LIC, and other legacy players, and insurtech startups.

Complimenting each other’s strengths can be a win-win. The collaboration between LIC’s vast distribution network, spread across the country, and tech prowess and product innovation of insurtech can be not only mutually beneficial but also help to a great extent in insurance penetration.

On the platter will be the vast Indian life insurance market for such a partnership. The size of the Indian life insurance industry was pegged at INR 6.2 Lakh Cr, based on total premium, in FY21, up from INR 5.7 Lakh Cr in FY20, according to a note by Anandrathi. The industry’s total premium has grown at 11% CAGR in the last five years ending FY21.

LIC – A New Benchmark For Insurtech Valuation

“LIC’s listing will bring in substantial investor interest to the sector,” said Banerjee, adding that the sector at present has only a few listed companies having a relatively small market share.

HDFC Life Insurance Co, SBI Life Insurance Co. and ICICI Prudential Life Insurance Co are the other listed legacy insurers. In the startup world, aggregator Policybazaar is a listed entity.

Banerjee pointed out that the startups in the insurance space can now evaluate their performance by benchmarking themselves against the listed players.

Equity investors embracing LIC IPO has, however, little to do with funding prospects for the insurtech sector. Private equities, VCs and angel investors will continue to evaluate the merits of funding insurance startups based on their individual moats.

Even if LIC adopts an aggressive digital approach after listing, its business model will continue to be different from that of insurtech players.

Complementing each other by playing to one’s strength—and not by competing — would serve best the interest of legacy players and startups in the medium term.