Insurance penetration in India was 1% in 2021 compared to the 4% global average

This makes insurtech the fastest-growing fintech sub-segment in terms of market opportunity, growing at a CAGR of 57%

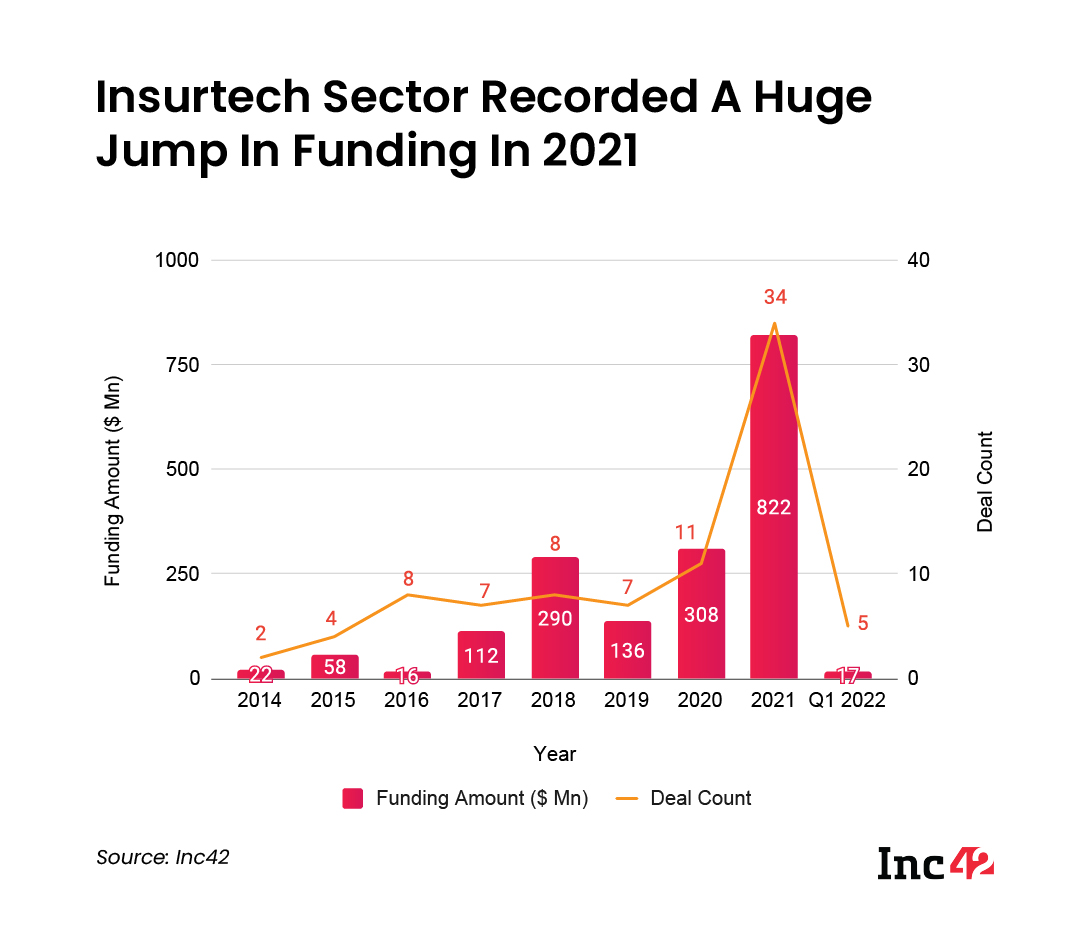

According to the latest fintech report by Inc42, 300+ active insurtech startups in India raised $1.8 Bn between 2014 and Q1 2022

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

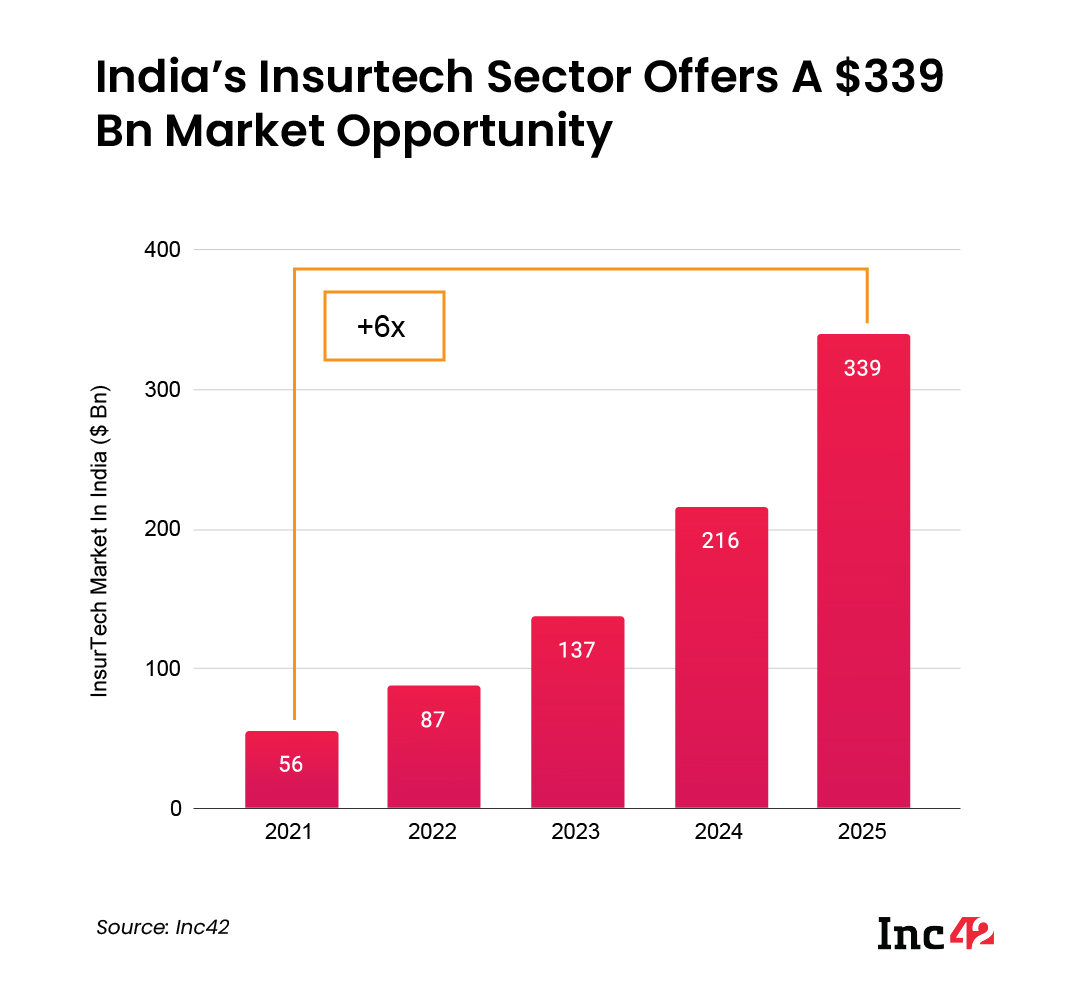

The Indian fintech market is one of the fastest-growing globally, estimated to reach $1.3 Tn by 2025, growing at a CAGR of 31%. Among its key sub-sectors, lending tech is likely to account for 47%, or $616 Bn, followed by insurtech at 26% ($339 Bn) and digital payments at 16% ($208 Bn).

In the wake of the pandemic, the Indian insurance sector (both life and non-life categories) witnessed considerable growth. According to IRDAI data, insurance penetration in India went up in FY21 to 4.2% from 3.76% in FY20.

However, as Indian Angel Network (IAN) cofounder Raman Roy says, less than 15% of the country’s 1.3 Bn population is served by the financial services sector, while insurance penetration was just 1% in 2021, which is very low compared to the 4% global average.

This spells a massive growth opportunity for the insurtech segment, in line with India’s burgeoning digital payment ecosystem. As Ankur Bansal, cofounder and director, BlackSoil Capital says,

“Insurtech is the fastest-growing fintech sub-segment in terms of market opportunity, growing at a CAGR of 57%, followed by investment tech (44%) and fintech SaaS (40%). Currently, the insurance market has a very low penetration compared to global leaders. With the National Health Stack further emphasising health insurance, it will help improve the (overall) penetration of the insurance sector.”

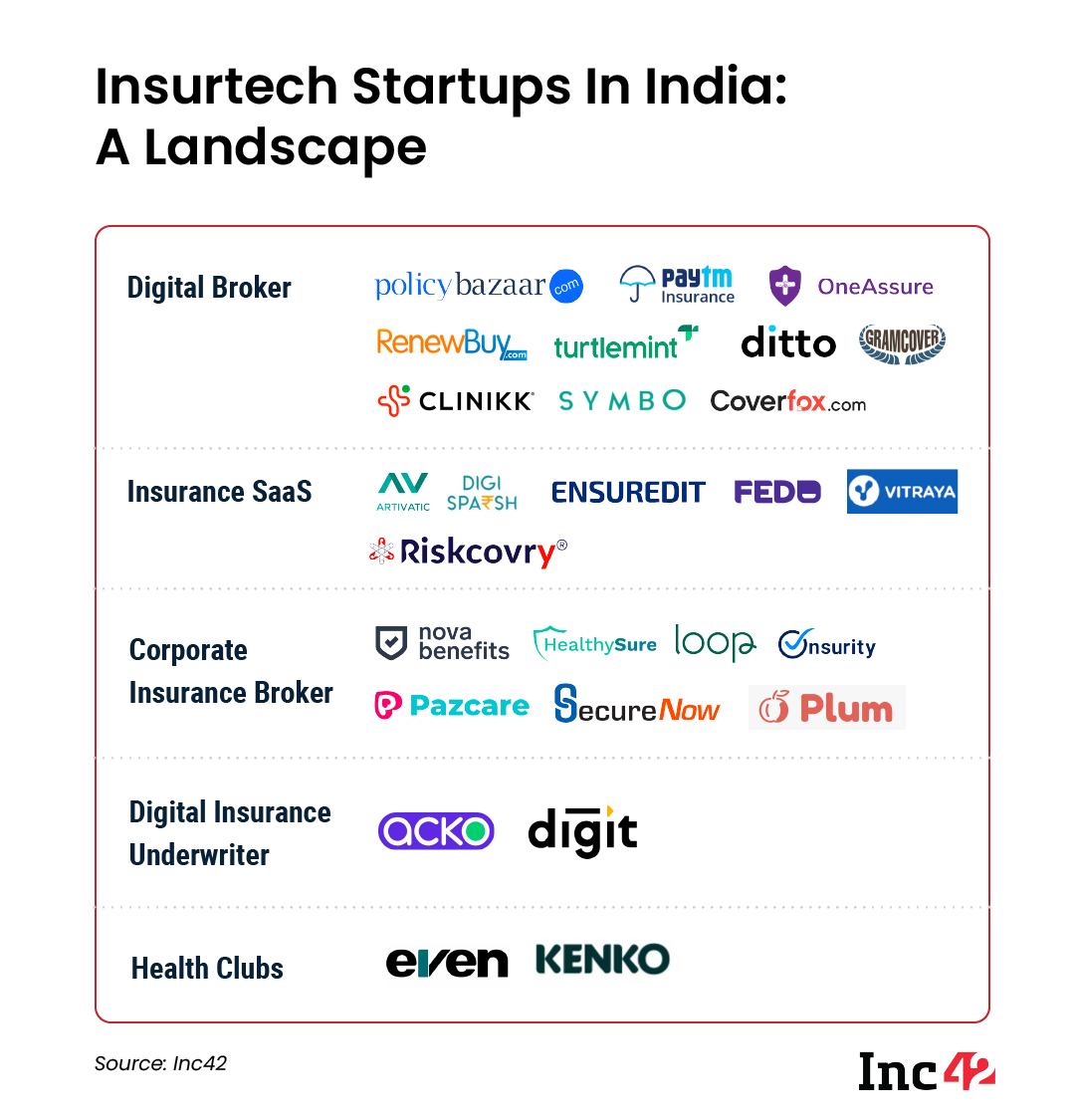

These are not mere predictions or a number-crunching exercise. According to Inc42’s latest release, The State Of Indian Fintech Report Q2 2022, InFocus: Insurtech, there are 300+ active insurtech companies in India. Among the funded ones, there are unicorns such as Acko, PolicyBazaar (publicly listed) and Digit Insurance (to IPO in 2023).

Further, insurtech companies in India raised $1.8 Bn between 2014 and Q1 2022, accounting for 8.18% of the $22 Bn funding raised by the entire fintech ecosystem. The year 2021 saw the maximum capital inflow in this sector, with Acko and Digit raising $225 Mn and $200 Mn, respectively, making it to the top funding deals of the year.

Other key insurtech companies in India eyeing a significant market share include Paytm Insurance, ENSUREDIT, Onsurity, Plum, Riskcovry, RenewBuy and Turtlemint, among others.

Factors Fueling The Growth Of Insurtech In India

Anup Jain, the managing partner at Orios Venture Partners, believes that India being a low-penetration market is the biggest reason it is poised for high growth in the insurtech segment.

Swati Murarka, vice-president of Athera Venture Partners, further underlines the rising awareness across Tier 2 cities and beyond, widespread use of women-specific insurance products, and better SME participation (and hence, more insurance benefits for employees) as the key reasons for insurtech growth in India.

“There have been B2C players like PolicyBazaar and Digit, which have cracked distribution on the retail side. But there is an increasing number of B2B2C players using partnerships with corporate houses/SMEs to drive higher penetration with lower acquisition cost. The acceleration of direct-to-customer digital sales for simple products to whom we call digital natives, omni-orchestration for lead generation and conversion and the AI-enabled agent lifecycle management have improved reach and conversion,” she added.

Other growth factors driving insurtech companies in India include:

Consumer Inclination: Post pandemic, there has been seen a rise in consumer spending on insurance products. India’s insurance penetration was pegged at 4.2% in FY21, with life insurance penetration at 3.2% and non-life insurance penetration at 1.0%. Premiums from India’s life insurance industry is expected to reach INR 24 Lakh Cr ($317.98 Bn) by FY31.

Improved Reach & Technology Blend: Acceleration of direct-to-customer digital sales for simpler products, to what we call “digital natives”, Omni-orchestration for lead generation and conversions, AI-enabled agent lifecycle management have improved reach and conversion. Data analytics has further helped identify new customer segments and also helped increase personalisation, improve underwriting, and enhance pricing proposition.

Emergence Of The National Health Stack: Currently, the Indian insurance market has a very low penetration compared to global leaders. National Health Stack has helped improve the penetration into the insurance sector. The digital infra growth has also boosted insurtech adoption and helped in increasing the exposure in Tier 2 markets.

Key Focus Areas For Insurtech Startups In FY23 And Onwards

Shashank Randev, Founder VC of 100X.VC, thinks that insurtech, a fragmented market, offers a huge opportunity to digitalise the entire process on the consumer and business sides.

However, these models should be flexible on payments and aware of the nuances of individual customer profiles instead of ticking a few standard boxes, which is the current norm.

According to Jain of Orios Venture Partners, “This will require multiple sandboxes on the regulatory side to harness the ability to innovate.”

Some key areas of focus for insurtech companies in India include:

Personalising Product Offerings: All the major players in the insurtech space aim to align themselves with rapidly changing customer behavior and the shift in consumers’ lifestyles towards healthy living. The key area of focus is on personalisation of product offerings instead of mass consumer-focused products.

Innovations In The Underwriting: This will lead to more flexibility and customised products with a fully digital experience combining zero friction on submissions, transparency on benefits and claims are some of the areas of focus for insurtechs which are current problem statements in the traditional insurance industry.

Expansion To Tier 2 & Beyond Cities: Unfortunately, most new and early-stage players are still battling for a small crowded target segment in tier 1 and urban cities. However, fintech startups who will be able to expand into the underserved and unserved markets, leverage technology as a solution, and build innovative products will be able to gain huge returns.

“Selling is only part of the challenge. The key issues lie around fulfilment and meeting the obligations. About 80% of the entrepreneurs primarily focus on customer acquisition. However, the entire fulfilment cycle, from tying up with insurers to building innovative products centred around current customer requirements, from customer acquisition to after-sales services, needs to be considered,” said IAN’s Roy.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.