SUMMARY

ESOPs are well thought-out plans to build cohesion and create shared wealth in a company

The ESOP buyback schemes have, of late, got an impetus on the back of fast-changing investment scenarios

A company may opt for ESOP buyback to provide an exit to employees or for listing gains if it believes its valuation can go higher

Employee stock options or ESOPs have been around for some time now. However, the recent uptick in startups going for ESOP buybacks has brought it under the spotlight.

ESOPs are well-thought-out plans to build cohesion and create shared wealth in a company. It is an all-important part of the liberal remuneration packages offered by companies to retain and attract talent. Today, employees are well informed about ESOPs and their wealth creation potential. Besides the monetary part, ownership interest excites employees. ESOPs also foster accountability on both sides.

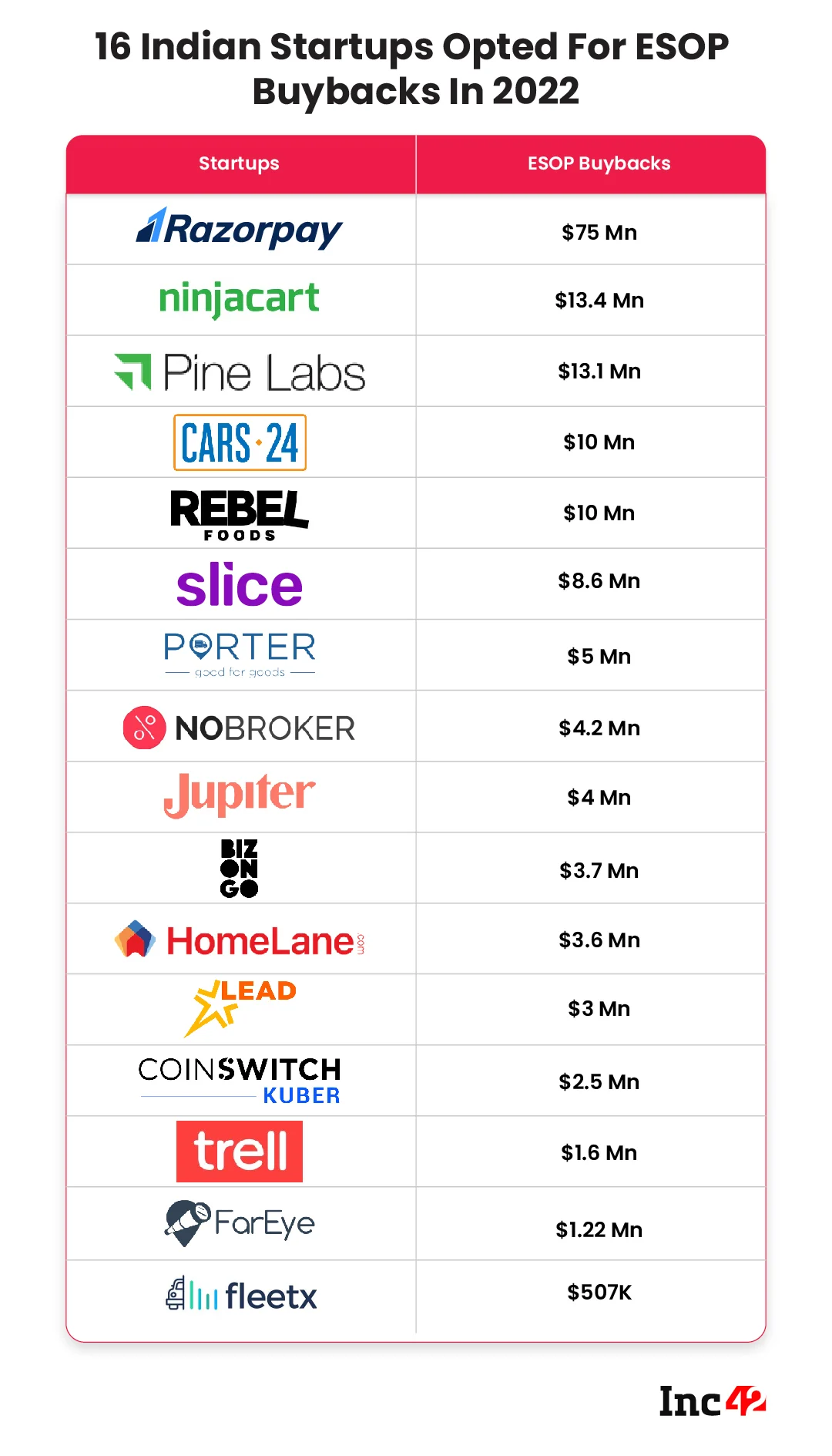

ESOP buybacks by companies have seen a frantic increase in the last year or so. In the first three months of 2022, 15 startups unveiled ESOP buyback schemes, in tune with the trend witnessed in 2021.

However, the question is why companies undertake ESOP buyback programmes. Is it a good idea to buy back ESOPs, and what are its tax implications for the employers and employees?

According to Rahul Shah, co-head of research at Equitymaster, “ESOP buyback is a good idea, provided the buybacks are done using the profits and cash generated by the company rather than raising money from outside.”

Factors That Trigger ESOP Buybacks

Reasons for ESOP buybacks vary. If the shares are not listed, a company may opt for buyback to provide an exit route to its employees.

“In some cases, companies believe valuation is high and can earn more while listing. So, they start buying their own shares,” said Kshitij Purohit, lead, commodities and currencies, CapitalVia Global Research.

A growing base of ESOPs in companies, which have managed to scale up revenue and valuation, allows investors to take exposure to companies whose shares may not be available directly. “Liquidity provisions to employees can provide an attractive price to take exposure in the investment,” said Nakul Zaveri, managing partner at Relativity Investment Management.

Recently, in the ESOP buyback scheme of fintech unicorn Razorpay, Lightspeed and Moore bought ESOPs from the 650 participants, reportedly at a valuation of $ 6.5 Bn.

ESOP Buybacks Are Rare In The Universe of Listed Entities

Enterprises buy back shares from public shareholders to jack up stock prices and boost investor sentiment. Publicly traded stocks are also brought back by companies to thwart hostile takeover bids.

However, ESOP buybacks by listed companies are rare. “Buyback of ESOP is not common among listed companies in India. It is mostly seen in startups and listed companies abroad,” said Rahul Sharma, research head, Equity 99.

Providing liquidity to employees is one reason why companies buy back ESOPs. Controlling the dilution in the company is another reason, Sharma noted.

“Once the vesting period has passed, the company facilitates a buyback exercise to allow its employees to liquidate their shares and create wealth. The shares can be bought back in stages or all at once,” Purohit pointed out.

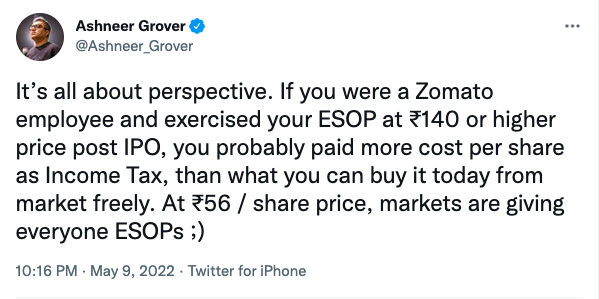

Buyback of ESOPs by listed companies can be intriguing. Unlike in unlisted companies, stock prices can be a key determining factor in the valuation game. But volatility in the stock can flummox stock option holders. BharatPe cofounder Ashneer Grover put it succinctly in a tweet.

Buyback Offer Is Not Legally Binding On Employees

No employee can exert pressure on a company to buy back stock options. But is it legally binding on employees to tender shares in buyback offers of the company? Sandeep Jhunjhunwala, partner-M&A, Nangia Andersen LLP, said Section 68 of the Companies Act deals with corporate provisions governing buyback of shares and other specified securities.

“The term ‘specified securities’ includes employee stock options and, therefore, technically, a company while buying back ESOPs prior to their exercise, should also adopt the procedures provided under Section 68 and related rules,” he said.

The prescribed procedures among other things require a company to make a buyback offer to option holders. An offer is always subject to acceptance. One can safely infer that ESOP buyback is not legally binding on employees. Rather, it is subject to the employee’s consent to voluntarily tender the options in the buyback plan.

“Even where ESOPs are floated by foreign parent companies which are not governed by Indian corporate laws, a buyback cannot be made legally binding on the employee, requiring a compulsory tender of ESOPs,” said Jhunjhunwala.

Taxing ESOP Buybacks: Salary Or Capital Gains?

The ESOP buyback schemes have, of late, got an impetus on the back of fast-changing investment scenarios. The tax implications of buyback, for both employers and employees, therefore, warrant a closer scrutiny now.

The Income-Tax Act does not specifically provide for tax implications on buyback of ESOPs before the exercise of stock options.

One view is that ESOPs are issued to employees by virtue of an employer-employee relationship and, therefore, the buyback of such options could be taxable as ‘salary’.

“In such a scenario, the employer would be under an obligation to withhold tax on payment of such consideration, i.e., ‘salary’ to the employee at applicable slab rates,” said Jhunjhunwala.

Such a view would find support if the employment contract or ESOP policies facilitate a subsequent buyback before the stock options are exercised.

Buyback of ESOPs, prior to exercise, could also be viewed as a relinquishment of rights to acquire equity shares. Hence, it could be construed as a transfer of capital assets.

This view is underpinned by the absence of a specific entry under Section 17 in the Income-Tax Act to cover buyback of unexercised options (this particular section deals with components of salary or perquisites).

The employee would be, however, under an obligation to pay taxes on buyback consideration by way of advance or self-assessment tax as there is no specific withholding tax provisions on payments in the nature of capital gains to resident employees.

“Capital gains payments to non-resident employees would, however, be subject to withholding taxes to be observed by the employer at applicable rates,” Jhunjhunwala said.

According to him, the characterisation of buyback consideration as salary vis-à-vis capital gains would become relevant even from the perspective of expense deduction at the hands of the employer.

The revenue department strongly favours the disallowance of ESOP expenditure. Officials argue that the same is notional and capital in nature.

Jhunjhunwala said in the case of a buyback, which entails cash consideration, expense deduction of such consideration could arguably be taken on the footing that it is akin to salary or bonus, and hence, an allowable employee benefits expense.

“Where the transaction is seen as a buyback of a right and treated at par with buyback of shares, claiming it as a tax-deductible expense could pose challenges,” he added.

Practically, unexercised options are bought back by the employer at a nominal value and cash consideration is given as a bonus, in lieu of such unexercised options, which get taxed as ‘salary’ at the hands of the employee, Jhunjhunwala explained.

ESOP Buyback Vis-à-Vis Buyback Of Listed Shares

Taxation aspects of buyback of ESOPs prior to exercise are pertinent. These are, however, unclear in the absence of specific tax provisions, noted Jhunjhunwala.

The Income-Tax Act provides for a specific tax regime for the buyback of shares. Buyback tax at an effective rate of 23.3% at the buyer company level is paid, calculated on the difference between buyback consideration and subscription amount.

“Income arising to the shareholder that has suffered buyback tax at buyer-entity level, is consequently tax-exempt,” he said.