Between 2020 and 2022, education-focussed lending apps mushroomed, piggybacking on the growth of the Indian edtech space, and getting an education loan became a matter of just a few clicks

However, the growth has been short-lived, and sectoral experts opine that these ventures are today struggling to increase or even maintain loan disbursal numbers, just like the lending apps outside the education space

Sector experts believe that a re-evaluation of the ongoing lending practices by retail education loan providers will go a long way in capturing a large share of the credit-seeking Indian learners’ market

Despite the widespread practice of financing higher education for children through loans in India, the educational loan market remains significantly underserved. According to CARE Ratings, the penetration rate of the higher education loan market in the country is just 20%, which gives many players ample headroom to stretch.

Notwithstanding the entry of public and private banks and NBFCs in the space, a majority of players, until the last decade, showed resistance in lending to students who come from low to middle-income households and have only concentrated on funding aspirants either seeking to study overseas or from top-tier colleges or universities.

Over the past decade, with the widespread availability of affordable data and inexpensive smartphones in Indian households, getting easy and rapid loans has become easier.

During this period, the country has also witnessed the emergence of numerous new-age lending apps. These apps promise quick loan disbursals, often within minutes, and offer benefits such as zero collateral, small loan amounts, extended repayment periods, and no-cost EMI payment options.

While many of these apps serve a wide range of borrowers and purposes, certain platforms have specialised in providing easy loans exclusively to students under categories such as K-12 education, test preparation, upskilling, overseas education, and other vocational courses.

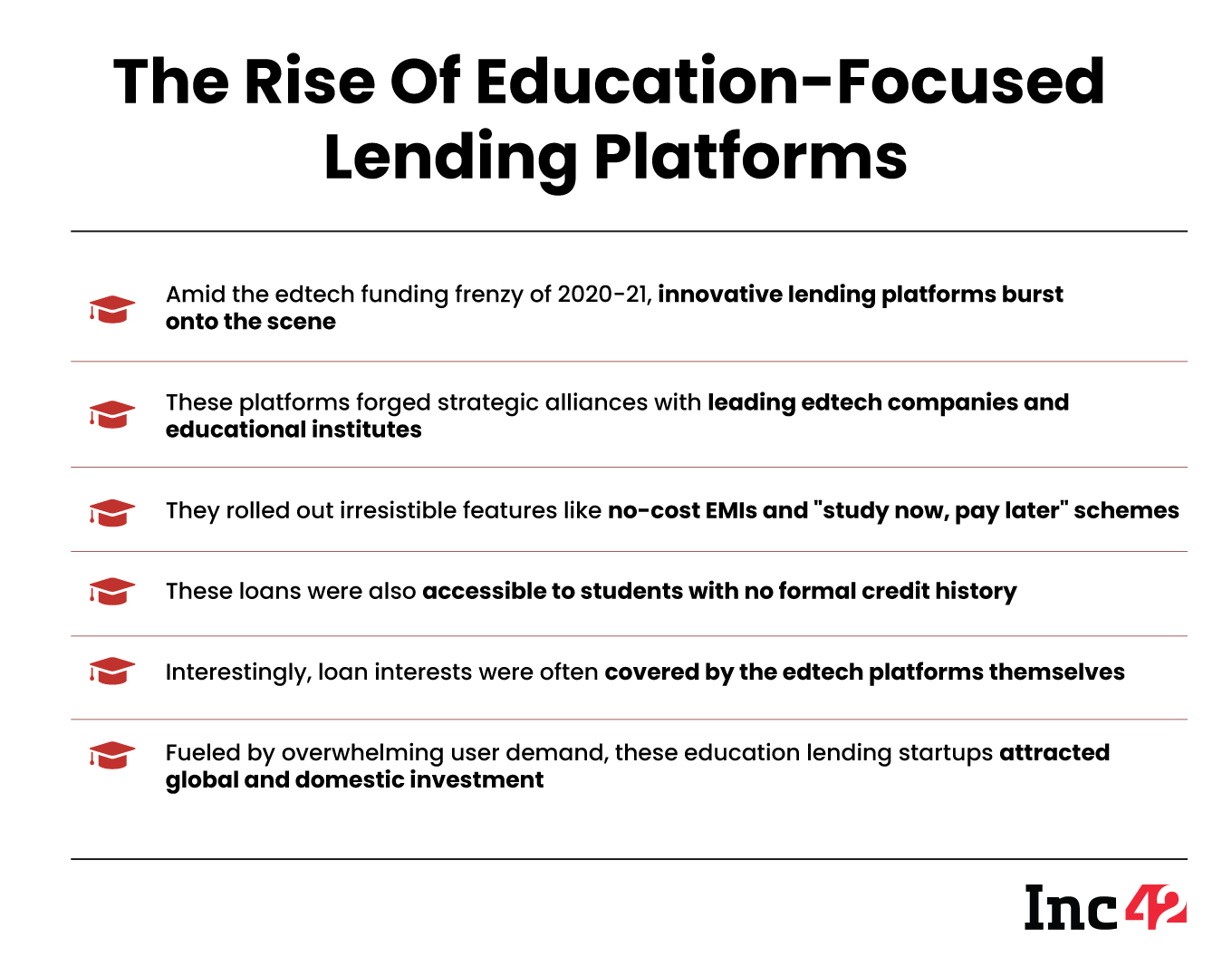

Before we move ahead, it is imperative to mention that the growth trajectory for education loan lending platforms coincides with the Indian edtech boom story.

Not to mention, the Covid-19 pandemic proved to be a shot in the arm for the edtech companies, when many of these players onboarded millions of users as the industry was also flush with billions of dollars of VC funds.

Given that a majority of edtechs grew their roots deep into the country, on the back of technology, joining hands with these players to serve students in Tier II & III cities and towns of the country and beyond made more sense.

Between 2020 and 2022, education-focussed lending apps mushroomed, piggybacking on the growth of the Indian edtech space, and getting an education loan became a matter of just a few clicks.

The lending service providers (LSPs) had but one playbook — to become allies of the flourishing Indian edtech startups and extend easy education loans to individuals under segments such as K-12, test prep, upskilling, vocational training and study abroad services.

Yet, the growth of education-focussed fintech startups has plateaued. Many of these ventures now grapple with challenges in boosting or even sustaining their loan disbursement figures, mirroring the trends seen in non-education lending apps.

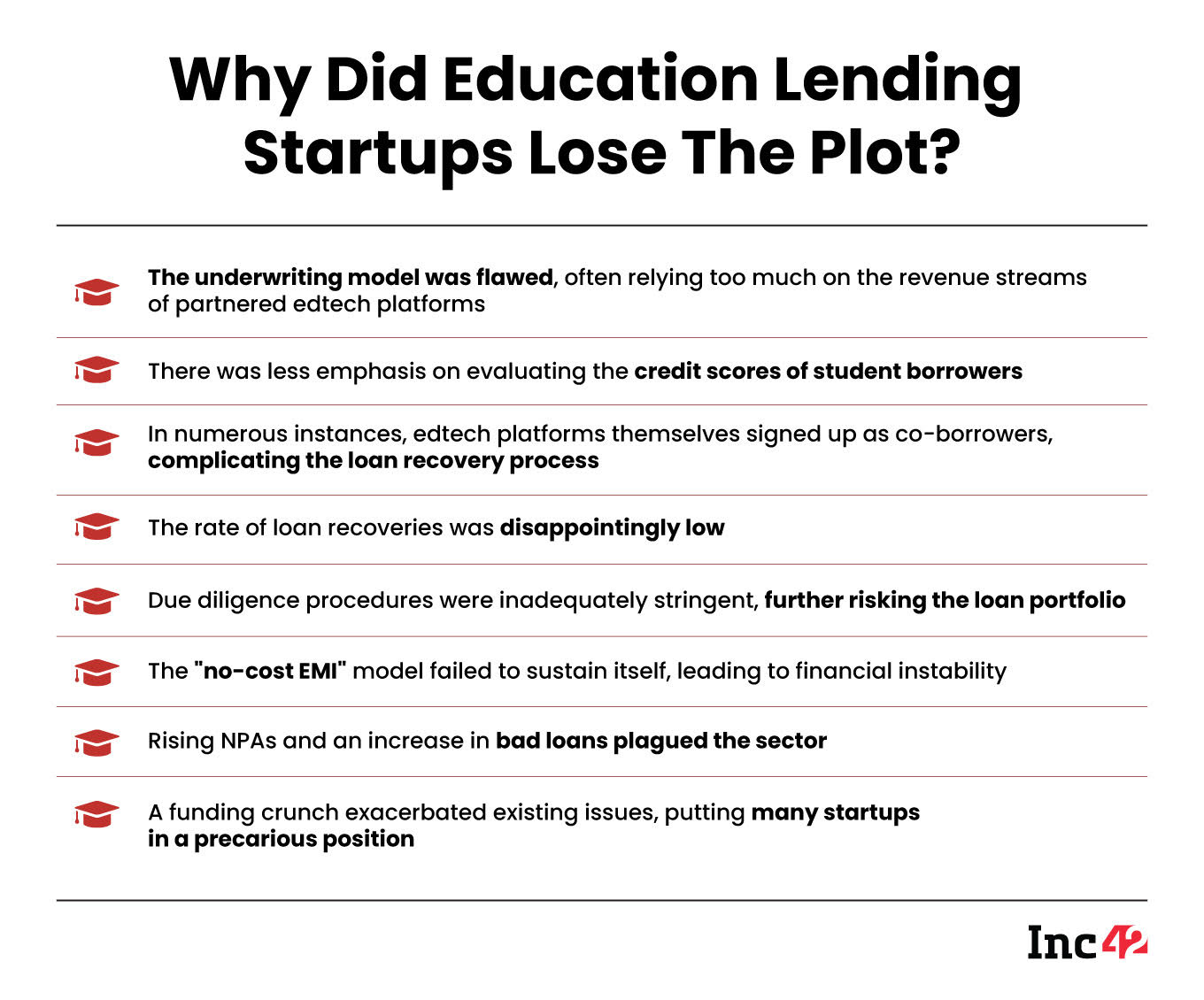

Not just this, this breed of lenders has also received a big blow due to their flawed underwriting models, inadequate due diligence, and rising NPAs, which could be as high as 50-70% in some cases, industry analysts Inc42 spoke to for this story revealed.

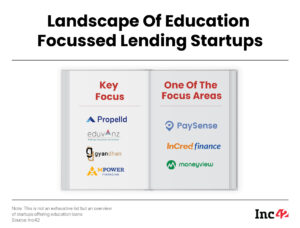

Currently, pureplay education financing companies like GyanDhan, Eduvanz, Propelld, and Avanse provide loans to students across various categories. Furthermore, fintech startups like MoneyView, PaySense, and InCred also extend education loans alongside a range of other credit services.

Further, amid a dire need for funds, many are struggling to stay afloat, and there seems to be little hope for them to get rescued as some resort to unethical practices, in clear violation of the RBI’s digital lending guidelines that came into effect in 2022, giving a bad name to the space.

So, what went wrong, and why there seems to be more distress on the horizon for these players?

Before we delve any deeper into the crux of the matter, let’s understand how a sub-sector in the Indian edtech space mushroomed during the pandemic and may now be on the verge of dying down.

The Pandemic Booster Shot

In a bid to cash in on the Covid-19-led edtech boom, many lenders ventured into the space and started facilitating individuals with hassle-free loans, easy EMIs and study now and pay later financing options — an area largely underserved by conventional banks or NBFCs, as stated above.

Raising the bar, these lenders focussed on taking Tier II and III cities under their ambit, which not only helped them increase their loan disbursals but also gave edtechs a boost of sorts.

Not to mention, this piqued investor interest, the likes of Peak XV, Better Capital, Matrix Partners and founders like CRED’s CEO Kunal Shah, and InCred CEO Bhupinder Singh, couldn’t resist forming a beeline to back the efforts of the new-age education loan providers.

Despite the high rate of interest, compared to the conventional educational loan rates, these players witnessed a massive uptick in loan disbursals, driven by an increasing number of students embracing edtech platforms, during the pandemic, either to upskill themselves or pursue higher education.

And given a sudden influx in the demand for these loans, who wouldn’t have wanted to dance cheek to cheek? Hence, the flow of millions of dollars of VC money.

For the uninitiated, edtech loan providers typically partner with NBFCs and banks (mostly private) to offer loans to students. These firms then join hands with edtech companies that provide various courses to students. Lately, many among them have also secured NBFC licences. Some of these names include Eduvanz and GyanDhan.

The credit facilities are usually offered to students at no interest with the flexibility to repay in a span of 3 to 15 months through EMIs.

According to the loan policy documents of these companies, the loans come with an interest rate of 15-30%, higher than those of banks that charge an interest rate of 7-15% on average.

Top industry experts that Inc42 spoke with said that in the majority of cases, where no-cost EMI education loans are provided, edtech platforms pay the interest on behalf of students.

According to Kaushik Saha, the lead for FinOperations at Apollo Group, various new partnerships have been forged between lenders and edtech firms since 2020. Under their agreement, edtech platforms absorb the rate of interest to facilitate no-cost EMIs to students and co-borrowers of guarantors of these loans.

Moving on, the realisation had yet to strike these players as to why traditional lenders shy away from offering quick educational loans, despite a huge market out there.

Anomalies In The Edtech Lending Structure

While, on the one hand, loan disbursals became a new fad, the rising number of loan defaults, on the other hand, was becoming a gigantic task to handle for these players.

At the outset, when the investor capital was flowing unabated into the edtech and fintech industries, investors looked to capture a wider userbase of India’s internet population that could be lent easy credit at higher interest rates.

Therefore, both investors and founders rested their focus on increasing the number of loan disbursals. However, what became the Achilles heel, in this strategy, was uncontrolled NPAs or bad loans.

According to experts, the strategy to serve the underserved market could have worked in the favour if these players were able to strike the right balance by earning minimum NPAs; however, more disbursals led to more bad loans — a trap that could have been avoided in the first place.

Now that the era of easy VC money has ended, a majority of these lenders are looking for ways to make recoveries.

Interestingly, while these lenders shy away from talking openly about their NPAs, they can still be seen fancying how their disbursals grew from 50-100% YOY in 2022 alone.

For instance:

- Mumbai headquartered Eduvanz, which focusses on the study now and pay later business model said that its loan disbursals grew 2x in 2022.

- GyanDhan, which provides loans for overseas education, disbursed loans to the tune of INR 700 Cr in FY22 and has set a target of INR 2,300 Cr in loan disbursals for FY23.

- Another education-focussed lending startup Avanse said that it disbursed loans worth INR 2,927 Cr in FY22, according to a report.

Notable, the metric that is being flaunted by a majority of these edtech loan providers gives little insight into the financial health of their businesses, as a majority of them are saddled with losses.

The Curious Case Of Zero-Cost EMIs

The promises of zero-cost EMI payments became another challenge as the high-interest rates in the range of 15% to 30% were to be borne by edtech platforms, a cofounder of an education loan startup told Inc42.

The strategy did not prove to be any kind of consolation as edtechs continued to lap up losses amid the funding winter, which, in turn, also impacted the revenue stream (income from interest) of their lending allies.

“Much like the consumer goods or ecommerce industries, where the BNPL or no-cost EMI modes are undergoing a major overhaul, the education financing companies will also have to re-strategise their products and pull back on incentivising their customers to run sustainable businesses,” a Bengaluru-based fintech product developer said.

Unlike large banks and NBFCs, which take into account multiple factors before offering loans, the lenders in the edtech space have largely focussed on providing easy loans, leading to high delinquency rates.

According to Saha, unlike the case of traditional education loans, the new-age education-focussed lending firms take into account the revenue model and the quality of the courses provided by their partner edtech platforms.

“In fact, more than 70% of underwriting weightage goes to the partnered edtech platform’s revenue model and 30% to the borrower’s creditworthiness,” Saha added.

This has failed to work out on so many levels, and now the Indian edtech sector is grappling with a cash flow issue, falling user base and scaling down of startup operations.

“Amid edtech woes, loan disbursals have taken a hit. In K-12 segment alone, we have witnessed a 20% YoY fall in the metric,” the CEO of a popular edtech financing company admitted.

Due Diligence Gone For A Toss?

Among other factors that have plagued the growth potential in this space is a general lack of due diligence before providing loans.

Last month, Inc42 reported how upkslling edtech Skill-Lync pushed students into a debt trap. When we dug deeper, we found that the edtech was allegedly making its students take personal loans by projecting them as ‘employees of some fake companies’.

The Inc42 report attracted a lot of attention on social media platforms and a wave of Skill-Lync’s former and current students emerged seconding the findings of the article.

Our pursuit to dig deeper into the woes of these students led us to a point wherein we were left stranded with the question if these students were offered education loans or personal loans.

This was because of two key reasons. Firstly, education loans do not require students to be working professionals, which in the aforementioned case was the case, and Inc42 has documents to substantiate this statement.

Secondly, many lenders offer educational loans against some collateral, which can be gold or property of the guarantors. Not only this, in many cases, lenders give weightage to the degree/course, along with the reputation of the institute, before approving education loans.

However, a personal loan, on the contrary, is given without any collateral on the creditworthiness of the applicant who can be a salaried employee or a businessperson.

In addition, the repayments of education loans start after the completion of a particular course or once a student has a job in hand. However, the EMIs of personal loans start instantly.

Moving on, according to industry experts, many lenders and edtech players are today working on a profit-sharing basis, with students at the core. Such partnerships should be scrutinised as they may well be in violation of the RBI’s newly stipulated lending guidelines.

Smelling that a lot could be brewing behind closed doors, the sources hinted that the closed-door partnerships between edtechs and lenders are such that while one party becomes a guarantor for the borrower (in this case students), the other party processes loans with little ado with zilch due diligence, completely overlooking the creditworthiness of borrowers, let alone collateral.

Further, the NBFCs or banks have the authority to restructure loans depending on the tie-ups they have with edtech platforms/educational institutions and the nature of the courses being offered.

On High Priority: Sector-Specific Lending Guidelines

Many questionable practices by some fintech companies have already invited regulatory intervention with the RBI issuing the digital lending guidelines last year that make it imperative for fintech companies/lenders to check the creditworthiness of the borrowers.

In addition, digital lenders are required to adhere to e-KYC mandates (of borrowers) to ensure more transparency in the due diligence process.

Earlier this year, the RBI released its default loss guarantee (DLG) guidelines, which make the lending service provider accountable in case of loan defaults. Under the new norms, lending service providers will have to guarantee the compensation of a certain percentage of default to the lending partner (banks, NBFCs or fintechs).

In the education loan disbursal space, it is not yet clear whether edtech platforms are classified as LSPs and should compensate for any loan defaults or if the onus is on fintech firms.

Sources say that the edtech platforms have mainly been acting as co-borrowers and not as guarantors to avoid compensating for bad loans.

In any case, the bad loans will show up on the books of lending partners, thereby adding to the latter’s list of challenges.

Therefore, it has now become all the more important for the apex bank to come up with sector-specific definitions of lending service providers, according to industry experts.

Notwithstanding the instances of unethical practices in the space, the overall education loan industry is in a recovery mode, according to CARE Ratings.

The overall assets under management (AUM) of the education loan segment stood at INR 1.1 lakh Cr, as of September 30, 2022, as against INR 0.88 Lakh Cr, as of September 30, 2020, as per the rating agency.

The education loan segment in India has been primarily dominated by public sector banks. However, over the past five years, specialised NBFCs, focussing on the overseas education loan segment, have seen a steady rise in their market share.

In just two years (between September 2020 and September 2022), NBFCs almost doubled their market share in retail education loans to 18.6%, as per a report by CARE ratings.

The report, dated February 2023, reads that NBFCs have focussed on building expertise in the retail education loans segment with well-defined sourcing channels, including educational consultants, digital marketing, and direct walk-ins at branches.

Further, higher loan book growth of NBFCs as compared to banks is primarily driven by the robust demand for the overseas education segment among Indian students. NBFCs, too, have carved out a niche in the overseas education loan segment supported by specialised credit underwriting skills, while banks remain focussed on catering to the domestic education segment, as per the report.

In the current times when much seems to be happening, with no cap on what’s right or wrong, a re-evaluation of the ongoing lending practices by retail education loan providers will go a long way in capturing a large share of the credit-seeking Indian learners’ market.

[Edited by Shishir Parasher]