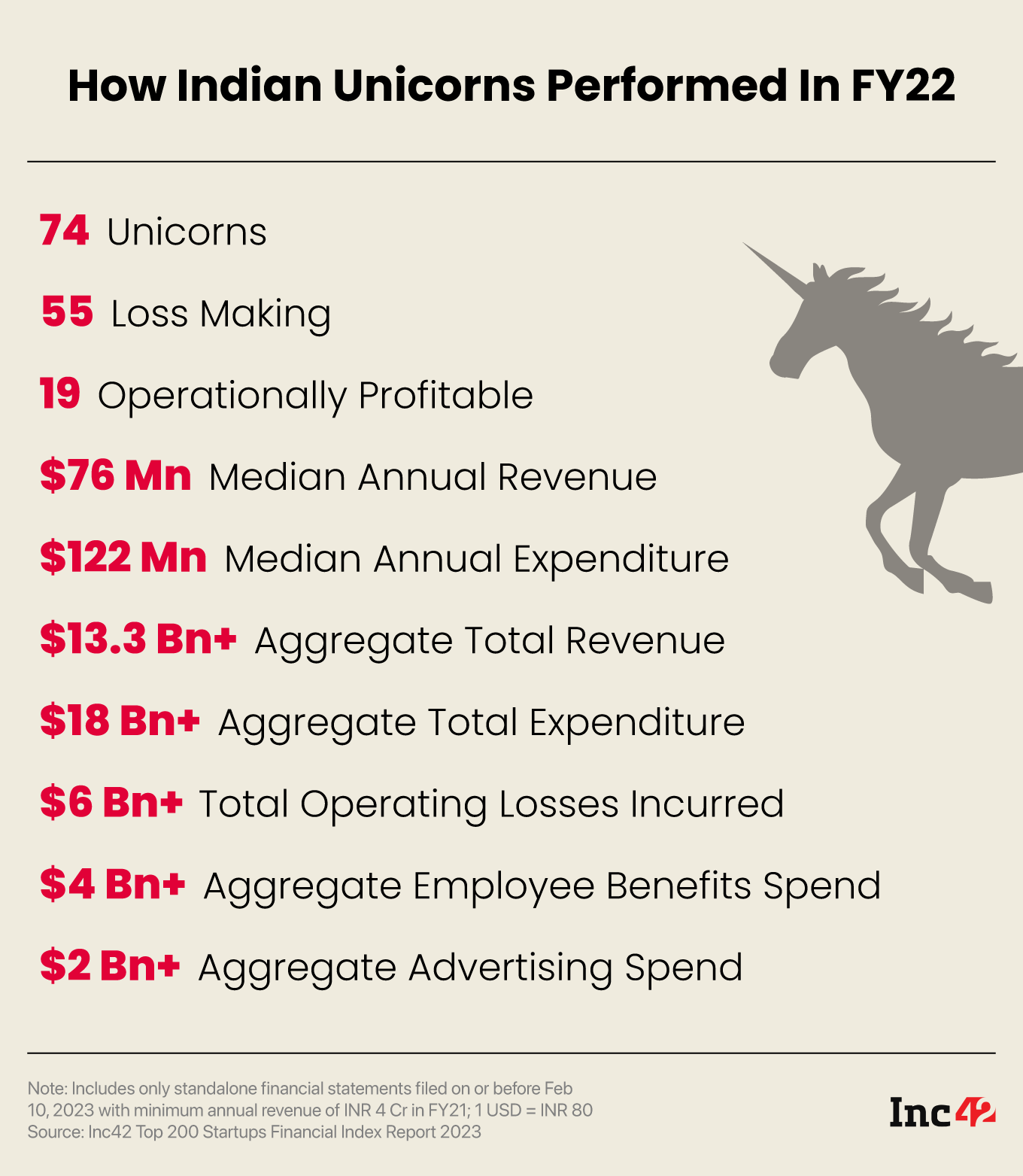

As many as 55 (74%) out of the 74 unicorns, analysed by Inc42, incurred a cumulative operating loss of $5.9 Bn in FY22.

With a median expenditure-to-revenue ratio of 1.5, the 55 loss-making unicorns burned INR 1.5 to generate INR 1 in revenue in FY22

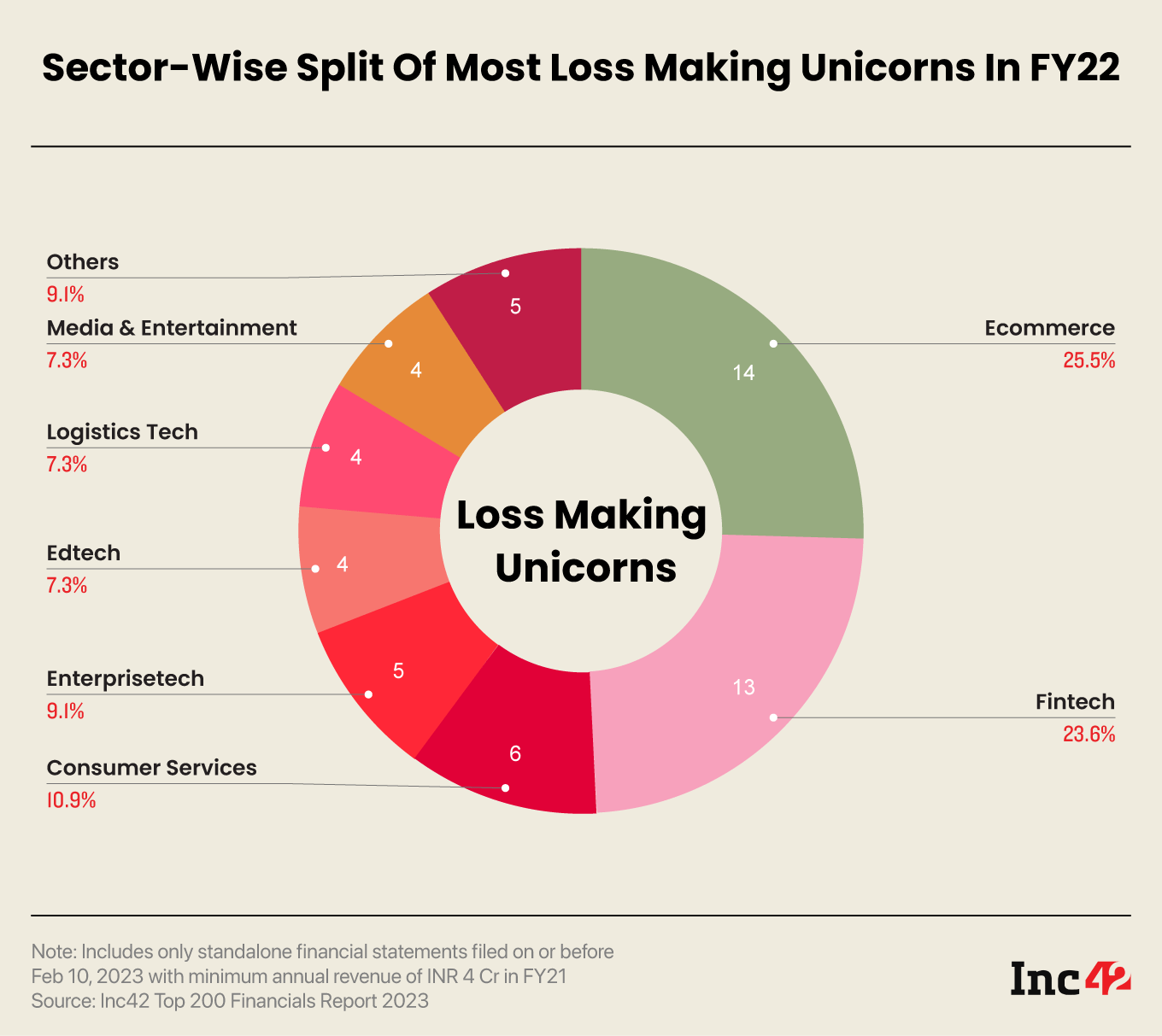

Of the 55 loss-making unicorns in FY22, 14 were from the ecommerce sector alone, followed by fintech at 13, and consumer services at 6 unicorns.

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

The race to enter India’s highly coveted unicorn club seems to have finally paused. Amid the funding winter, no new startup has been able to secure the unicorn tag after Tata 1 MG entered the club of 108 unicorns in September 2022.

Further, what is disheartening is that in the first two months of 2023 (January and February), the number of mega deals stood at only five, as compared to 23 such deals in the same period a year ago. Overall, Indian startups raised around $1.6 Bn in January and February 2023, compared to $8.3 Bn raised in 2021, according to the data compiled by Inc42.

With purses clenched tighter than ever before, investors have now taken a backseat, and their eyes are only on the startups that put profitability, unit economics, and revenues first. Not to mention, this impacted India’s most-valued startups in FY22, which were seen struggling due to mounting losses despite heavy cash burns.

According to Inc42’s ‘India’s Top 200 Startups Financial Index Report 2023’, as many as 55 (74%) out of the 74 unicorns, analysed in the report, incurred a cumulative operating loss of $5.9 Bn in FY22. This was almost double the cumulative loss of $3 Bn incurred by 53 unicorns in FY21.

With a median expenditure-to-revenue ratio of 1.5, the 55 loss-making unicorns burned INR 1.5 to generate INR 1 in revenue in FY22. This is an increase of 15% from the median expenditure-to-revenue ratio of 1.3 for 53 loss-making unicorns in FY21, indicating that unicorns burned more cash to generate revenue in FY22.

According to Rajeev Suri, partner, Orios Ventures Partners, the FY22 was an era of free money and market sentiment was all about chasing growth. Investors made a risky bet on high-growth companies for better returns, while startups burned more cash, seeking hyper growth. However, with changing public market dynamics and the not-so-good performance of venture-funded IPOs, the pressure to achieve profitability piled up on Indian unicorns.

Download Report!“The cost of capital has gone up and one can no longer afford to continue burning capital. The founders need to judiciously deploy the capital, as investors are now asking for metrics like profitability, return on equity (RoE), return on ad spend (RoA), which was not the case earlier. All this has lead to recalibration of strategies from the founder’s perspective and FY23 numbers will be very different,” added Anirudh A. Damani, Managing Partner at Artha Venture Fund.

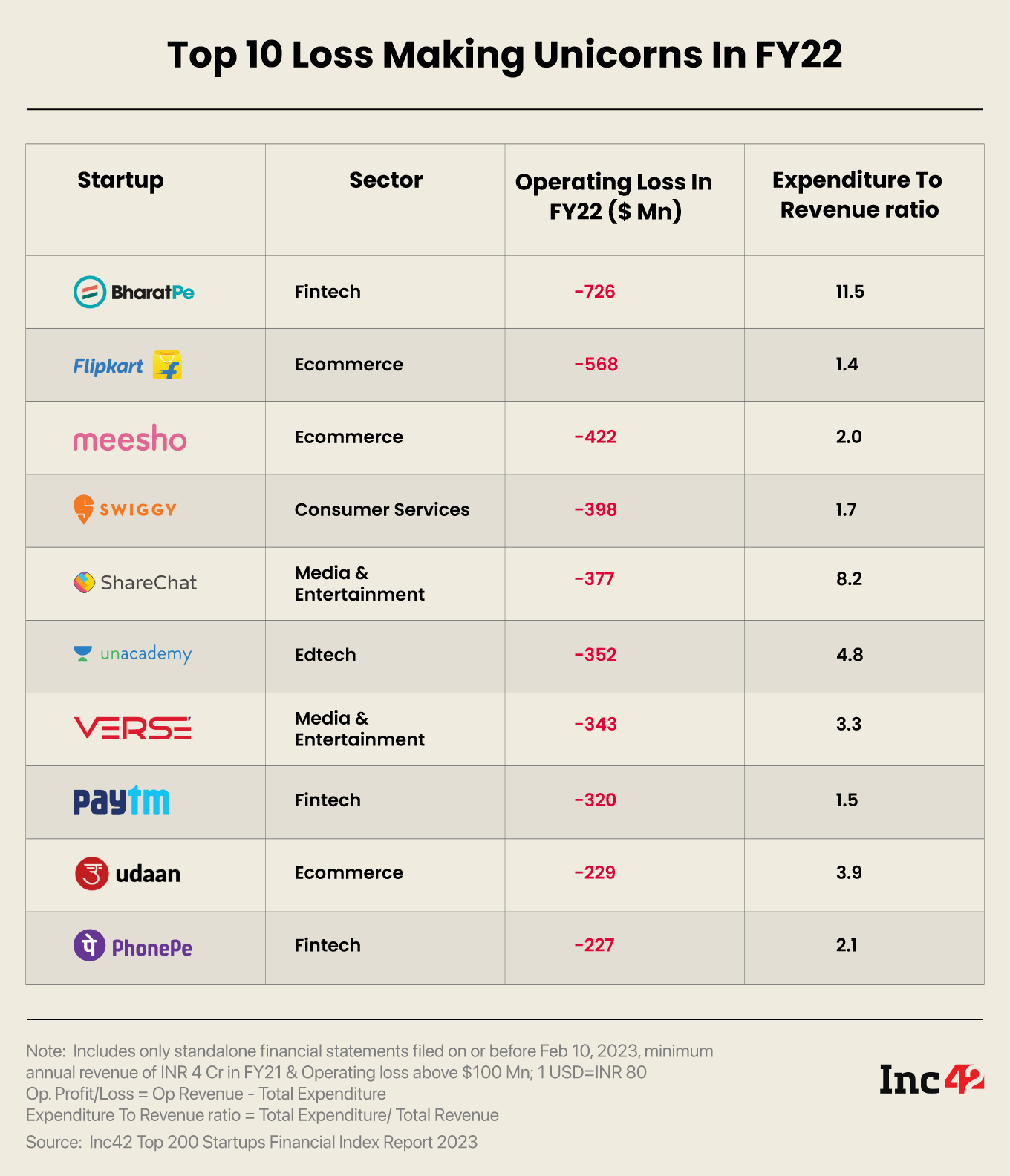

BharatPe: The Highest Loss-Making Unicorn In FY22

As shown in the chart below, BharatPe emerged as the highest loss-making unicorn, with an operating loss of $726 Mn and an expenditure-to-revenue ratio of 11.5, indicating that the startup spent INR 11.5 to earn one rupee in revenue in FY22.

It is pertinent to note that the high FY22 loss was due to a one-time non-cash expense related to the change in the fair value of compulsory convertible preference shares (CCPS), BharatPe stated in its filings with the Ministry of Corporate Affairs. Excluding the CCPS conversion, the company’s operating loss stood at $98.2 Mn (INR 811 Cr) in FY22.

The company has been going through a leadership crisis since the emergence of a public spat between former MD Ashneer Grover and the board last year. Additionally, the startup recently saw the exit of CEO Suhail Sameer.

Further, the expenditure-to-revenue ratio of ShareChat and OYO remained high in FY22 – at 8.2 and 8.8, respectively. Although Flipkart and Meesho were able to keep their FY22 expenditure-to-revenue ratio lower than many others, they were saddled with heavy operational losses.

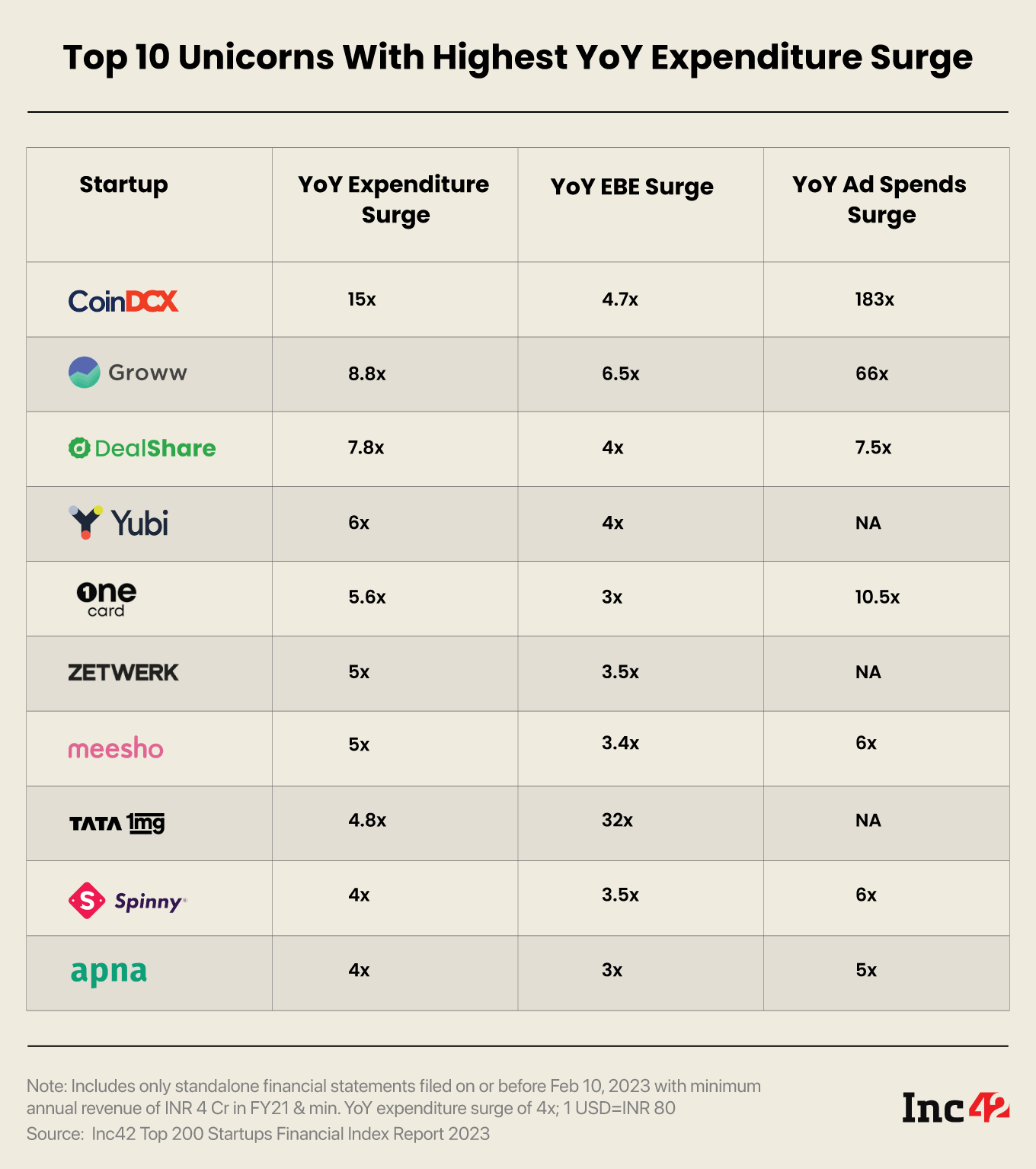

CoinDCX: The Unicorn With Highest YoY Surge In FY22 Expenditure

While CoinDCX incurred an operating loss of around $4 Mn in FY22 at an expenditure-to-revenue ratio of 1.06, its expenditure jumped 15x YoY to $76 Mn from $5 Mn in FY21. The increase in expenses was primarily due to the surge in the company’s ad spend, which grew 183x in FY22 to $40 Mn from $221K in FY21.

Amid strong growth in the popularity of cryptocurrencies, CoinDCX appointed actor Ayushmann Khurrana as its brand ambassador in October 2021. It also launched many other marketing campaigns that year, leading to higher ad expenses. However, the ongoing crypto winter and the Reserve Bank of India’s (RBI) stance on cryptocurrencies have now hit the growth momentum of crypto exchanges in the country.

In terms of YoY employee expenditure growth, 1mg posted the highest surge of 32x in FY22, while in terms of ad expenses, Groww followed CoinDCX with a 66x surge in FY22.

Ecommerce: The Sector With Highest Number Of Loss-Making Unicorns

Of the 55 loss-making unicorns, 14 were from the ecommerce sector alone, followed by fintech at 13, and consumer services at 6 unicorns.

The Profitability Paradox

Over the years, the primary consumer-facing sectors such as ecommerce and consumer services have continued to struggle due to the dearth of product differentiation/offerings, high customer acquisition costs, low customer retention, lower repeat ratio, and heavy ad spending, among other things, making it difficult for companies to walk straight on the path of profitability.

According to Blacksoil Capital’s cofounder and director Ankur Bansal, “The key issue faced by unicorns in the Indian consumer sector is heavy reliance on online sales and the dependence on third-party manufacturers.” He added that e-retail penetration in India was around 5% in 2022 against 28%-30% in countries such as China.

Not only this, ecommerce websites have a major problem of a lower average order value (AOV) of $15 coupled with high double-digit product returns of around 18-21%.

“Amazon accepted returns of approximately $761 Bn in 2021. High returns add to the overall fulfilment cost, as the companies are required to bear the cost of reverse logistics, a business which grew by approximately 10% in 2020 alone. Additionally, ecommerce has to rely on a deep discounting model, owing to a lack of product differentiation/offerings and the presence of mom-and-pop shops,” Bansal added.

Compared to others, fintech is marred by complex and stringent regulations, which make it difficult for fintech startups to innovate and create differentiation. For instance, the RBI’s notification on PPI-MD last year has put an end to the rising challenger credit cards as a new category in the fintech space.

Orios’ Suri highlights that while UPI has revolutionised payments, factors such as a zero merchant discount rate have killed a prospective business model for fintechs. While asset management and insurance businesses are primarily driven by commissions, lending is cluttered and poses challenges for fintechs to grow.

Download Report!Is Unicorn Profitability Really A Concern?

In one of his recent social media posts, CRED’s founder Kunal Shah wrote, “Most venture-funded companies are built differently than common businesses that trade where you buy cheap and sell goods with some margin. Tech companies invest capital for several years in building large distribution and engagement before they monetise.”

However, the bigger question is: For how long should a company burn VC money without becoming profitable?

As Artha’s Damani believe, the VCs today are not comfortable with unsustainable burns. The cost of raising money from a LP has gone up and it in essence has created a domino effect on the entire cycle of investing, deployment of capital by investors and expected returns.

At the same time, the investors we have spoken to have reiterated their faith in the founders at the unicorn level.

Orios’ Suri said, “The founders who have reached this level are smart and young. They know when to get back to the drawing board. This is a ruthless market, and they have struggled and successfully managed down cycles, in which many failed. So, if you tell them profitability is the only way to go forward, they will achieve it with their focus on creating strong business fundamentals.”

Overall, India today stands out as a strong market globally. Also, with India leading the group of G20 nations this year, it is expected that startup investments may revive after an initial slowdown in the next few quarters. Although in Anirudh’s words, the year 2021 euphoria is difficult to be seen again anytime soon until if one confirms that Covid is going to come back, economy is going to shut down and the governments across the globe will be printing more money.

Download Report!“Until then, these are the days of ‘agnipariksha’ (testing times) for India’s unicorns. Standing on a curve, those who will survive this phase will transition to a much smoother road to a sustainable future,” Suri concluded.

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.