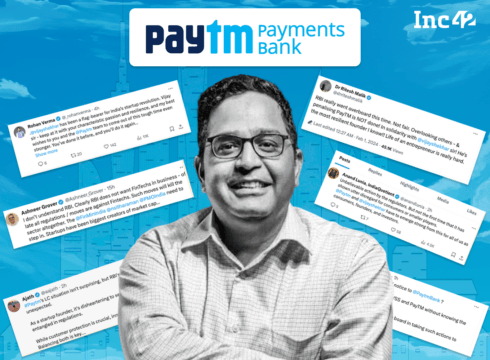

The Paytm CEO is receiving full support from his colleagues and veterans from the startup ecosystem

Stakeholders of the Indian startup space have called out the RBI for targeting the Indian fintech sector, which is already dealing with several regulatory quagmires

To mitigate the impact of the RBI diktat, the company will accelerate the transfer of its nodal accounts to other banks

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

Barely a day after the RBI cracked its whip on Paytm Payments Bank, barring it from providing UPI service or any other banking services to its customer accounts, several startup founders and VCs stand in support of Paytm CEO and founder Vijay Shekhar Sharma.

At a time when the RBI curbs could have a far-reaching impact on India’s biggest fintech firm and result in the annulment of its payments bank licence, the Paytm CEO is receiving full support from his colleagues and veterans from the startup ecosystem.

Notably, this is also one of the rare instances in which even bankers and analysts, let alone founders, have criticised the RBI and termed its diktat ‘harsh’.

While it was still unclear until yesterday what the RBI’s stance might mean for Paytm, analysts see the RBI directive impacting revenues of offline merchants, FASTtag payments, wallets business and several other propositions of Paytm.

However, in a bid to mitigate the impact of the RBI diktat, the company has said that it will accelerate the transfer of its nodal accounts to other banks and minimise the impact on business continuity.

For the uninitiated, the apex bank also issues directions to terminate the Nodal Accounts of One97 Communications Ltd and Paytm Payments Services Ltd at the earliest.

Meanwhile, the Paytm CEO has extended his gratitude to the startup community.

“Thank you everyone for your relentless support. Obviously, a conversation at a wider level should help. We should not let anything deter us from what we all have built over so many years. The Indian Startup Dream must overcome every situation collectively. Here, for good,” Sharma said.

Moving on, stakeholders of the Indian startup space have openly criticised the RBI for being dismissive of tech entrepreneurship. Some have even called out the RBI for targeting the Indian fintech sector, which is often seen bogged down in regulatory challenges.

It is also crucial to note that the RBI has maintained that the new curbs on Paytm Payments Bank have been slapped due to “persistent non-compliance and continued material supervisory concerns”.

In March 2022, the RBI directed Paytm Payments Bank to stop onboarding new customers. Despite Paytm expressing confidence earlier that good news would be received on this front by March 2024, the ban has not been lifted by the central bank yet.

In the larger Indian payments bank arena, Paytm rivals players like Airtel Payments Bank, Fino Payments Bank and Jio Payments Bank. While Paytm Payments Bank was incorporated in August 2016, Jio followed suit with a similar offering just three months later.

The central bank’s latest regulatory whiplash has come at a time when the oil-to-telecom conglomerate Reliance Industries’ fintech arm, Jio Financial Services, is making serious headway into the country’s much-regulated fintech space. Even analysts and sectoral experts, see the incursion of the behemoth (RIL) in the fintech domain as a threat to the likes of Paytm and others.

The RBI’s latest stance to tighten its noose on the VSS-led fintech also comes at a time when there is growing fondness for reverse flipping among Indian startups based in foreign lands.

As of now, the Desh Wapsi plans of fintech startups like Groww, Pine Labs, and Razorpay are in full swing. However, the latest RBI-Paytm chapter has the potential to make Indian startups settled abroad reconsider their stance, for the industry stalwarts have time and again raised concerns over heavy regulatory compliances.

While it remains to be seen what step will the apex bank take to soften its blow after its Paytm stance, fears are brewing unabated that more such moves have the potential to derail the country’s fintech ambitions.

The Paytm stock opened the day at its lower circuit of INR 609.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.