SUMMARY

Subhead: Raises $750K Funding From Prime Venture Partners

Micro, Small and Medium Enterprises (MSME) sector has become a big priority sector in not only in the Indian economy but also in the Indian startup ecosystem. Besides the impetus from the government’s ‘ Startup Indian, Standup India’ plan, it is also witnessing interest from many startups who are trying to solve the problem of working capital for SMEs in their own ways.

For instance Ahmedabad-based GVFL Limited has launched INR 600 Cr. MSME Fund, known as Value Multiplier Fund to focus on the technology startups and non-technology MSMEs in the early-growth stage. Then there is Chennai-based fintech startup, Veritas Finance, mainly catering to the working capital and business credit requirements of the small businesses in the MSME sector. There are many others working on similar models such as such as Aye Finance and Lendingkart.

However, the fact remains that SME sector still faces a cash crunch MSMEs often struggle to keep their cash flow intact and can hardly withstand the burden of late payments. They are always in dire need for working capital to sustain continued growth and production. It is this problem that the Bangalore-based KredX, an invoice-discounting platform founded by IIT & Stanford alumni Manish Kumar, Anurag Jain & Puneet Agarwal in 2015, aims to solve.

Today, it has raised $750k in funding from Bangalore-based seed stage investor Prime Venture partners.

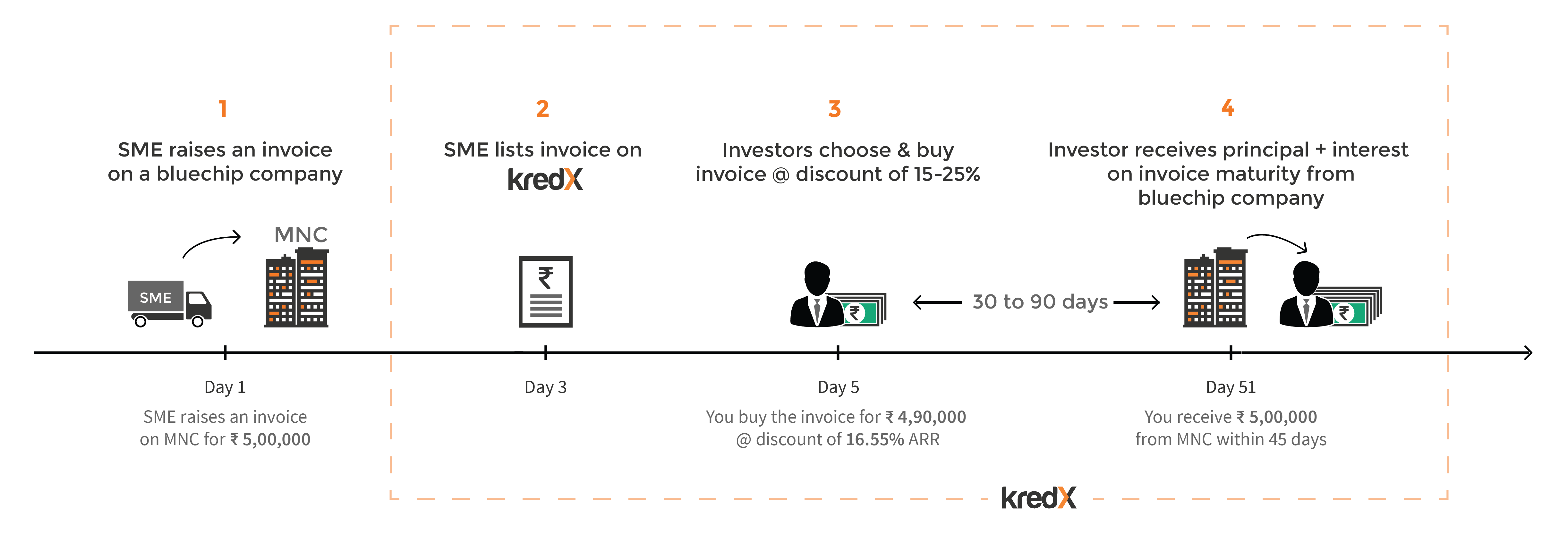

Says Manish, “For SMEs who supply to blue chip companies, it normally takes about 60-90 days to get their invoices credited. During that time when cash is locked, SMEs normally have to resort to banks for working capital requirements without realising that the invoice itself is an underutilised financial instrument. On the other hand are individual financiers who are looking to earn above-average financial returns aims to solve. Hence KredX connects the credit-worthy MSMEs looking to raise working capital (against their unpaid invoices) to these individual financiers, thereby enabling instant access to cash for SMEs.”

Through invoice discounting is not a new method, but KredX is trying to democratize it, and enable it in an organized way, to solve the problems of working capital of MSMEs by unlocking cash tied up in customer invoices that would otherwise be paid in 30 to 90 days.

How It Works

KredX is following a top down approach to getting SMEs on the platform. Hence, it partners with large blue chip companies, signing an agreement with them to take up their entire supply chain. The firm could be a software firm or a manufacturing firm or in be in any sector. By partnering with KredX for free, it only stands to benefit as KredX straightens out their supply chain, fuelling its growth by powering the supply chain. So while a working capital loan from a bank or a NBFC would take 2-3 weeks to materialize, KredX makes it possible to get access to funds in 48 hours.

Meanwhile the associated SMEs stand to benefit as they get instant access to cash on the back of their invoices at a very miniscule service fee. Simultaneously, retail financiers who are always looking for opportunities to invest in financial instruments that can provide them better returns in short term with relatively lower risk also benefit by partnering with Kredx at the same minimal service charge.

Technology To The Rescue

In order to suitably assess credit risk of SMEs, the startup has an in-house credit risk team and has developed its own proprietary risk model using artificial intelligence, data science, and machine learning. It has put in place a comprehensive system of its own checks and balances to mitigate risk and avoid defaulters. In addition the Fintech startup has partnered with leading banks, accounting firms and law firms to ensure all aspects of the service are fully compliant with regulations and ensure consumer protection at all times.

Additionally, for financiers, KredX provides complete trade services starting from sourcing curated invoices to conducting due diligence using its proprietary credit underwriting algorithms. It also manages complete paperwork for the financier and borrowers.

In the rarest of cases, if the blue chip company defaults on the invoice, it ensures that the SME is in apposition to pay on the back of its other clients. There is a soft collection team in place as well.

1000 Invoices And Counting!

Since it became operational in June 2015, KredX has already processed over 1000 invoices (ranging from INR 1 lakhs to INR 1Cr) in a period of less than a year. That too solely by-invitation only launch. Now it is looking to its service commercially. The startup has also set up a sales team in place to pitch to HNIs, who too have mostly been acquired through referrals till date.

On being questioned about this year’s targets Manish adds, “ In our less than one year of operation, we have actually surpassed the initial targets we had set. So we are going back to the drawing board again to assess our goals for this year.” No wonder the startup caught the eye of Prime Venture Partners. The funds raised would be utilised to expand the team as well as strengthen the analytics and technology platform.

As far as the competition from other players such as Lendingkart, Aye Finance, and Veritas Finance is concerned, Manish adds that startups in this space are attacking the problem in different ways but KredX is trying to solve it differently. He adds,

“The way we think of it is why should SMEs go for a loan when they have an asset which can be utilized for the same? So while invoice discounting was happening in an unorganized way, what we are doing is organize this largely unstructured market using technology, data and statistics.”

Investor Speak

And it is this strong technology focus of KredX which was one of the factors which drew the interest of Prime Venture partners. Sanjay Swamy, Managing Partner, Prime Venture Partners stated, “ The fact that KredX has a strong technology focus and is looking to scale by using AI and algorithms and not simply fleet-on-street teams was a big draw. Besides that, the founding team is a great mix of people with the right blend of sales, banking, and technology expertise. So pedigree of the team was also a strong factor. That said, the space itself is a multi-billion dollar opportunity with a big gap between demand and supply to be addressed.”

Sanjay added that alternate financing and lending platforms are going to transform the way businesses and individuals gain access to capital. The core competency required for any credit product to scale is risk modelling. As per him, KredX is using technology to solve an obvious pain point for over 21 million MSMEs in India with hundreds of unpaid invoices and is assembling an incredible team of experts in Data Science, AI and Machine Learning that will play a key role in scaling the business.

One could not agree more on this. As per current estimates, India’s MSME sector represents about 58 Mn businesses, which is creating over 150 Mn jobs, and accounts for 45% of the country’s industrial output. With KredX tapping into the largely unstructured market of invoice discounting, there is tremendous opportunity for it to scale. It radically different approach to solving the working finance problem for SMEs using underutilized asset of invoices, does place it in a different league from other players in the space which are majorly relying on loans. As rightly pointed out by Sanjay, any startup which wants to succeed in this space has to develop a fool-proof risk model. How far is KredX able to do that with invoice discounting using AI, data science, and machine learning is something to watch out for.