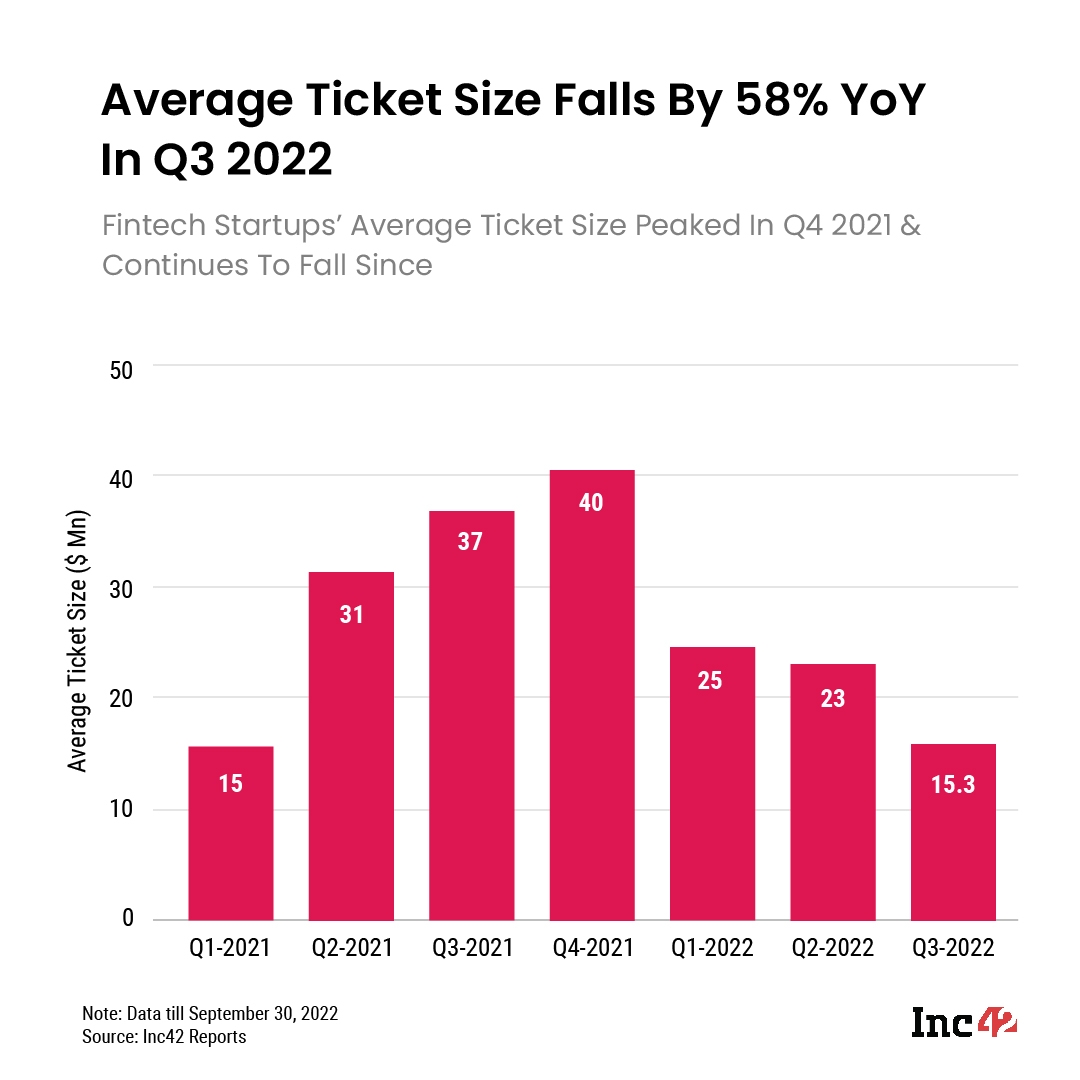

Fintech startups in India raised a total of $815 Mn in Q3 2022, while the average ticket size declined to $15.3 Mn

The number of mega deals in September 2022 quarter declined to 1 from 8 in the preceding June quarter

Experts and market stakeholders are of the opinion that fintech SaaS, digital banking, blockchain, insurtech, and others are some segments to watch out

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

The ongoing funding winter has cast a dark shadow on the fintech sector and slowed down the funding momentum of fintech startups. The average funding ticket size in the sector plummeted 58% year-on-year (YoY) to $15.3 Mn in Q3 2022 from $31 Mn.

The average ticket size during the quarter was 33.5% lower from $23 Mn in Q2 2022. It was also a 61.75% decline from the peak average ticket size of $40 Mn achieved in Q4 2021 in the wake of the pandemic.

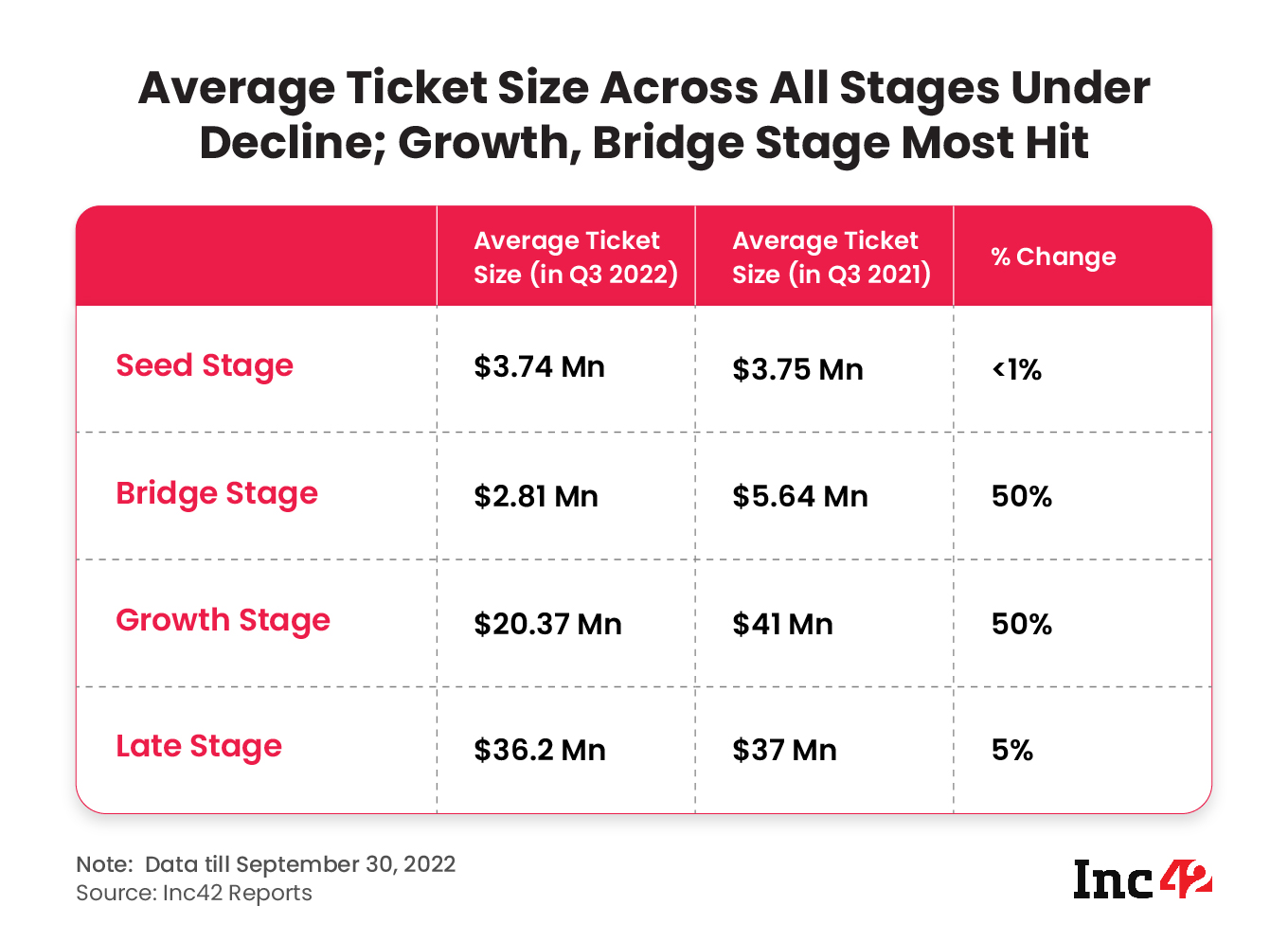

The growth-stage startups in the fintech sector were the worst hit in Q3 2022, recording a 50% YoY decline in average ticket size to $20.37 Mn, while the average ticket size for late-stage startups fell 5% to $36.2 Mn.

The average ticket size for early-stage startups stood at $3.5 Mn during the September 2022 quarter, a 12% YoY decline.

Notably, India’s fintech ecosystem is estimated to be a market worth $2.1 Tn by 2030, growing at a CAGR of 18%. However, only 647 startups out of the over 4.2K active startups in the sector are funded currently.

In terms of total funding, the fintech sector raised the highest $815.5 Mn during Q3 2022 among the key sectors. However, this was a decline of 55% compared to $1.78 Bn each raised in Q2 2022 and Q1 2022. Further, the funding has nearly become one-fourth from the peak of $3.2 Bn raised in Q4 2021.

Reasons For Fall In Average Ticket Size

The ongoing Russia-Ukraine war, the strengthening dollar, high global inflation, among others, have impacted the overall funding in the Indian startup ecosystem. The fintech sector is also a victim of this funding winter.

The continuous fall in funding is an indicator of the same. However, specific to the fintech sector, experts have observed three key reasons for the dwindling average ticket size:

Fall In The Number Of Mega Deals: The $815 Mn raised in Q3 2022 comprised only one mega deal above $100 Mn. OneCard, a Pune-based fintech startup raised $100 Mn in July 2022 from Temasek. On the contrary, 8 mega deals worth $665 Mn were recorded in Q2 2022. Mega deals are generally the deal makers and breakers when it comes to average ticket size. However, investors are increasingly becoming wary of writing big cheques over differences in valuation of startups.

Overlapping Business Models Within Subsectors; Need For Novelty: The novelty of fintech players is dying down as neobanking functions, lending in Tier-2 cities and beyond, embedded finance, BNPL and more become common themes across startups.

According to Nayan Gala, founder of startup investment banking platform JPIN, most of the fintech startups are building their supply side by collaborating with various financial institutions to cater to the demands of their repeat customer base. Unless service extensions are provided, the sustainability of such startups is questionable as there are many similar players present in the ecosystem.

This too adds to investors’ inhibitions, pushing them further towards early-stage startups to experiment at lower ticket sizes.

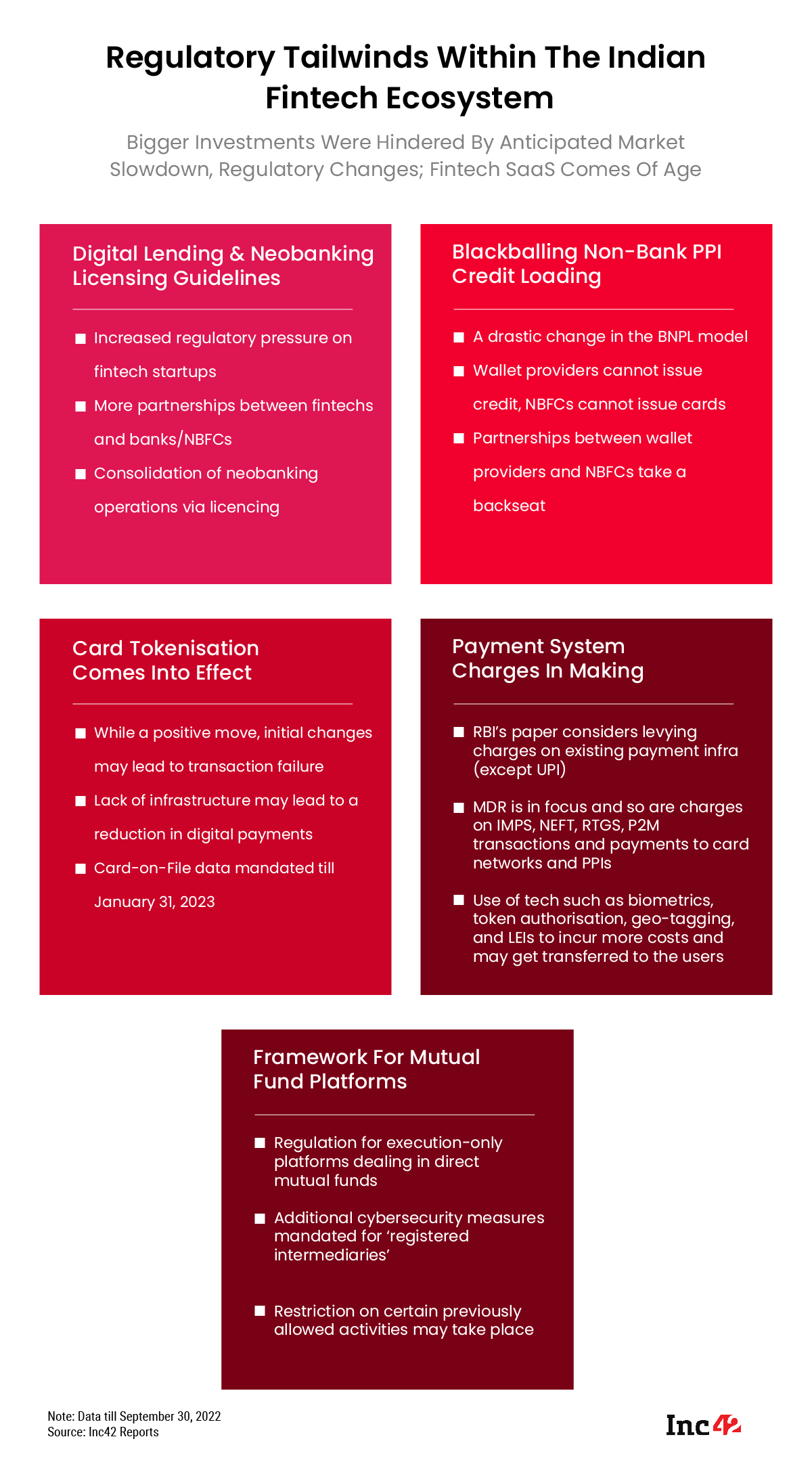

Regulatory Concerns: The year 2022 has primarily been about the tightening regulations within the fintech sector. From issuing digital lending guidelines to barring non-bank prepaid payment instrument (PPI) issuers from loading PPIs with credit lines, the Reserve Bank of India (RBI) has left no stone unturned in order to better regulate the startups in the rapidly growing fintech sector.

The segments such as digital lending and payments were impacted by the regulations, and many key players, including unicorns, had to go back to the drawing board for a change in their operational strategy.

Consequently, lending startups Jupiter, Kreditbee, Uni, and Slice discontinued some of their products.

Future Outlook Towards Fintech Sector

PayNearby cofounder Anand Kumar Bajaj said that investors are focusing on viability and efficacy metrics of the startups. The influx of money in fintech has slowed down, but will soon recover, he added.

In 2022 itself, several fintech startups got growth-stage funding, while numerous innovative ideas have also been scaled. Fintechs that are resilient, determined to bring about a change, and resolute enough to make it through the ongoing market are likely to reap the benefits going ahead.

The digitisation in financial services in India has been growing at a phenomenal pace. Besides, with the central bank looking at regulations, the fintech startups can hope for clarity when it comes to the rules of engagement.

JPIN’s Gala also identified challenges such as security problems and user privacy issues that have most commonly affected the fintech ecosystem, and the startups need to prepare to deal with them.

Many market analysts, investors, founders, and other stakeholders believe that the next-gen sectors for the fintech ecosystem are fintech SaaS, digital banking (cross-border neobanking included), blockchain, and insurance, among others.

Despite the recent decline in funding, the overall funding has increased steadily over the last few years. While the prevalent negative sentiments have made investors wary of writing big cheques, the road ahead looks promising and exciting for the fintech startups.

{{#name}}{{name}}{{/name}}{{^name}}-{{/name}}

{{#description}}{{description}}...{{/description}}{{^description}}-{{/description}}

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.