Bernstein expects strong medium-term growth potential in the 35%-40% CAGR range for Indian internet companies in 2023

Bernstein said that Zomato is its top pick in its internet coverage and maintained an ‘outperform’ rating and INR 90 price target (PT) on the foodtech giant

Bernstein has a “market-perform” rating on Nykaa and a PT of INR 185, which implies an upside of 20% to the stock’s last close

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

The sharp funding slowdown in the startup ecosystem will benefit startups which are market leaders in the Indian internet segment as they focus more on profitability as an additional growth vector, according to brokerage Bernstein.

“Profitability continues to be the core focus for India internet. Listed internet players have made significant progress towards getting to profitability in 2022 and with a focus on economics to continue in 2023…We expect strong medium-term growth potential in the 35%-40% CAGR range for internet names,” Bernstein analysts said in a research note on Thursday.

The brokerage said that the market consolidation due to the funding slowdown will benefit leaders in the Indian internet ecosystem in 2023.

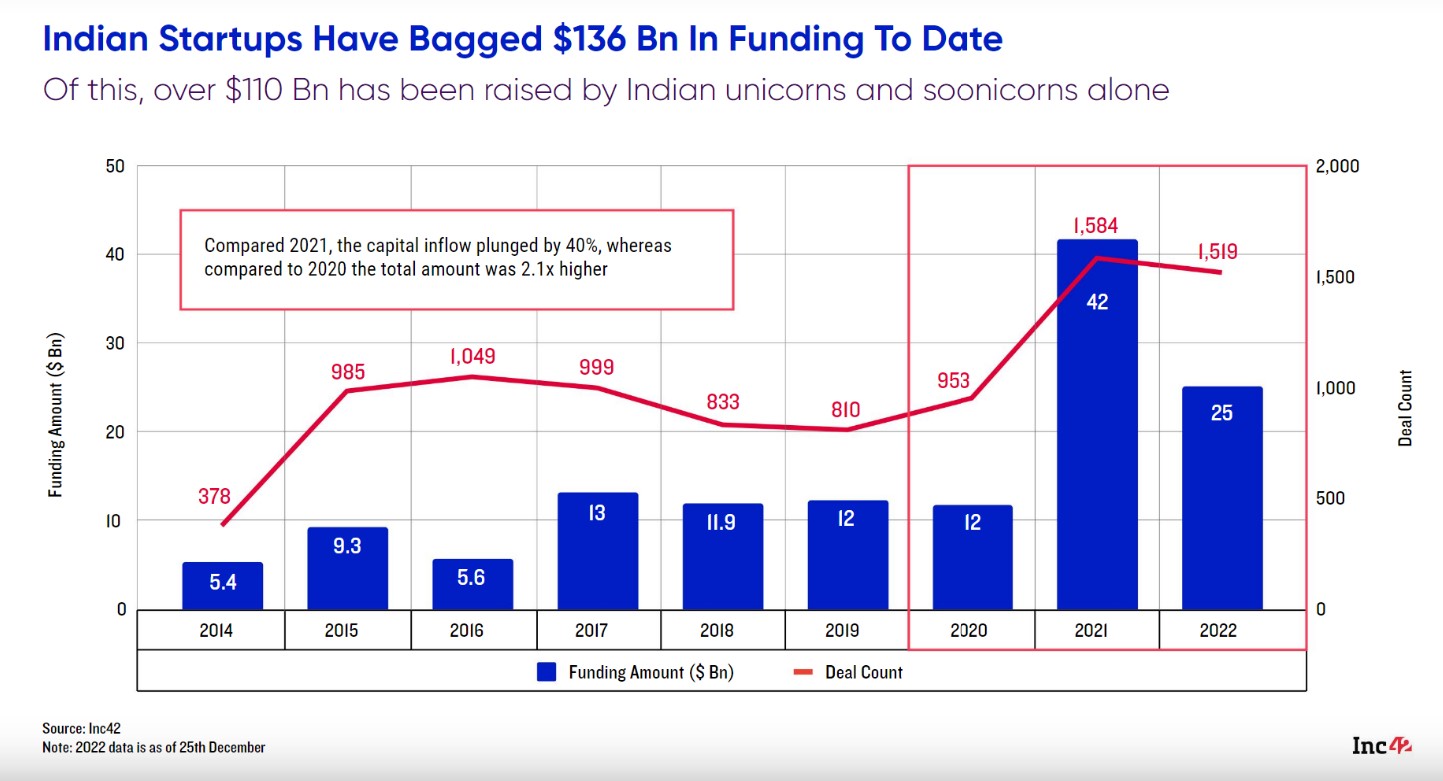

It is pertinent to note that a funding winter has wreaked havoc in the Indian tech startup ecosystem in 2022. As per Inc42’s latest Annual Indian Startup Funding Report 2022, Indian startups raised $25 Bn in funding in 2022, registering a 40% decline from the previous year.

The entire India tech segment was hurt by the global economic slowdown, high inflation, increasing interest rates, and the Russia-Ukraine war in 2022. From a steep valuation decline for the listed new-age internet stocks to the postponement of IPOs due to volatility in the market, the Indian internet segment, along with its global peers, witnessed a tough year.

As Bernstein noted, Indian internet stocks that listed in 2021 saw an almost 30%-50% correction in stock prices, across ecommerce, food delivery and fintech segments. Zomato and Nykaa, which saw strong listing gains of about 80%-90% in 2021, declined 57% and 55%, respectively, in 2022.

With investors becoming cautious, many tech companies have doubled down on their focus on profitability, which has led to restructuring and mass layoffs at many companies.

While foodtech giant Zomato has set its timeline for achieving an overall adjusted EBITDA breakeven between Q4 FY23 and Q2 FY24, fintech firm Paytm is looking to achieve breakeven at the EBITDA level by the end of September 2023.

Bernstein said that Zomato is its top pick in its internet coverage. The brokerage has maintained an ‘outperform’ rating and INR 90 price target (PT) on the foodtech giant, which implies an upside of 60% to the stock’s last close.

“Within our internet coverage, Zomato declined 55% but held up in the second half (+10%) as the company focused on a path to profitability (breakeven),” the brokerage said.

In fact, shares of Zomato declined to INR 41.65 by July 2022 from INR 137.45 on December 31, 2021. However, the shares ended the last year at INR 59.35 on the BSE.

Zomato reported a 42% year-on-year (YoY) decline in its consolidated loss to INR 250.8 Cr during the September quarter of FY23. However, acquisition of loss-making Blinkit did increase its loss on a sequential basis.

On the other hand, profitable beauty ecommerce giant Nykaa also came under severe pressure on the exchanges last year as many institutional investors dumped its shares. However, Bernstein has a “market-perform” rating on Nykaa and a PT of INR 185, which implies an upside of 20% to the stock’s last close.

Nykaa has a market leadership in the fast growing online beauty and personal care (BPC) segment and a large potential market opportunity in the fashion segment, but existing competition presents downside risks, analysts at Bernstein noted.

“Nykaa has demonstrated strong GMV growth in the past and healthy unit economics. But current valuations, which are at a premium to ecommerce/other internet players and BPC companies, keeps it market-perform,” the brokerage said.

Nykaa reported a 344% YoY rise in its net profit to INR 5.2 Cr in the September quarter of FY23, largely helped by a strong growth in its BPC segment. Its GMV also rose 45% YoY to INR 2,345.7 Cr during the quarter.

Bernstein believes that the internet stocks’ value drivers, which include attractive market structure and improving unit economics, remain intact.

Shares of Zomato ended marginally down at INR 56.2 on the BSE on Thursday, while Nykaa were up marginally to end at INR 154.

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.