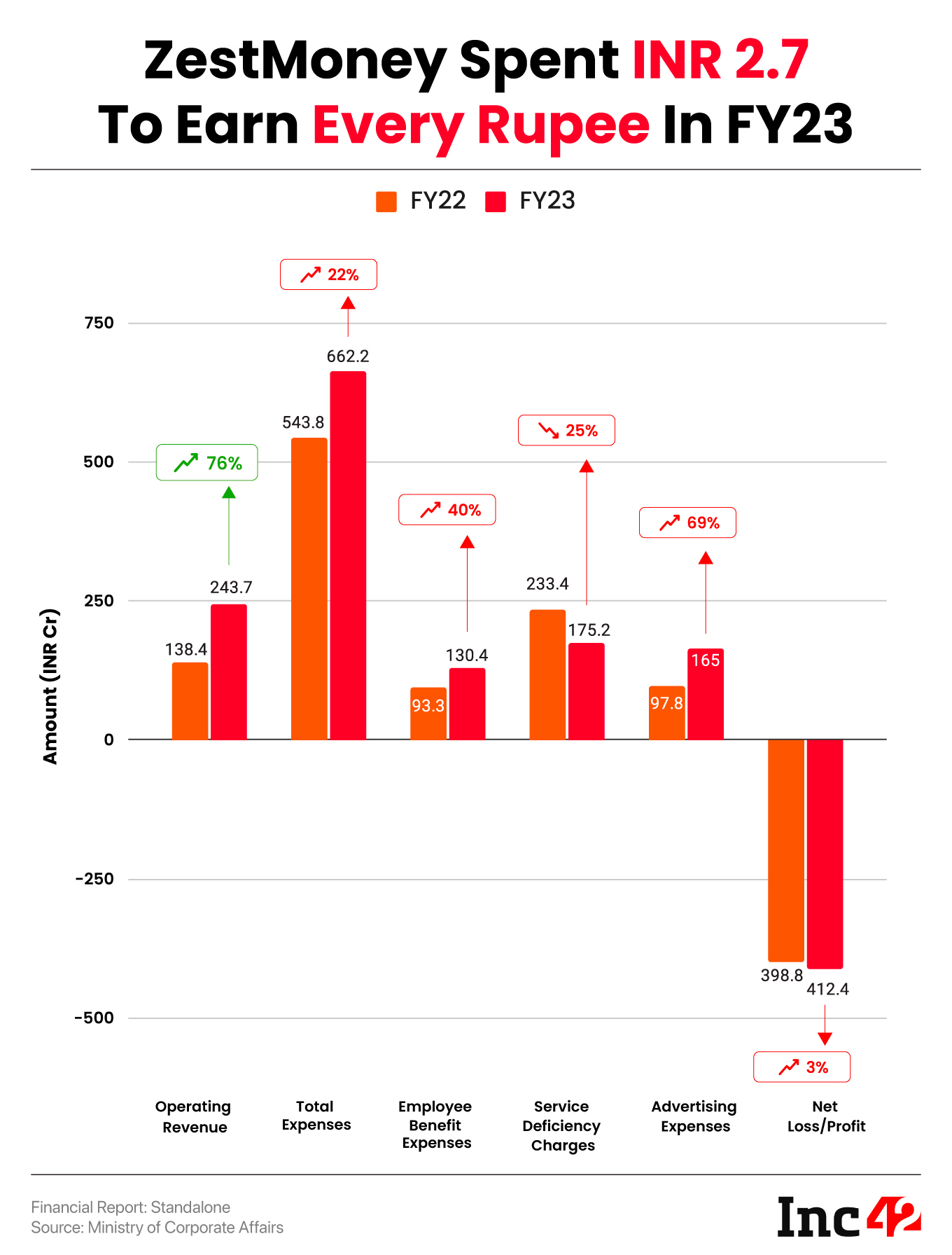

ZestMoney’s operating revenue rose to 76% to INR 243.7 Cr in FY23 from INR 138.4 Cr in FY22

The startup, which was to shut shop at the end of December 2023, spent INR 2.7 to earn every rupee in FY23

As on March 31, 2023, ZestMoney’s total cash and cash equivalent stood at a mere INR 49.6 Lakh

Inc42 Daily Brief

Stay Ahead With Daily News & Analysis on India’s Tech & Startup Economy

Troubled buy now, pay later (BNPL) startup ZestMoney reported a net loss of INR 412.4 Cr in the financial year ended March 31, 2023. This was a marginal rise of 3% from the loss of INR 398.8 Cr the startup reported in the financial year 2021-22 (FY22).

Revenue from operations rose 76% to INR 243.7 Cr in FY23 from INR 138.4 Cr in the previous fiscal year.

Founded by Lizzie Chapman, Priya Sharma and Ashish Anantharaman in 2015, ZestMoney partners with non-banking finance companies (NBFCs) to provide loans to retail customers. The startup is now on the verge of shutting down (more on this later).

Including other income, its total revenue rose 72% to INR 249.8 Cr during the year under review from INR 145 Cr in the previous fiscal year.

Where Did ZestMoney Spent?

The BNPL startup’s total expenses increased 22% to INR 662.2 Cr in FY23 from INR 543.8 Cr in the previous fiscal year.

Service Deficiency Charges: At INR 175.2 Cr, service deficiency charges accounted for 26.4% of ZestMoney’s expenses in FY23. In simple terms, service deficiency charges are the cost borne by ZestMoney for bad loans. However, this cost declined by 25% during the year under review from INR 233.4 Cr in FY22.

Advertising & Marketing Expenses: The PayU-backed startup spent almost 68% of its operating revenue on marketing and advertising expenses. ZestMoney’s advertising costs surged 69% to INR 165 Cr during the year under review from INR 97.8 Cr in the previous fiscal year.

Employee Benefit Expenses: Employee costs rose 40% to INR 130.4 Cr from INR 93.3 Cr in FY22. Employee benefit expenses comprise employee wages, gratuity, provident fund, and other employee welfare benefit costs.

At an unit economics level, the startup spent INR 2.7 to earn every rupee in FY23. As on March 31, 2023, ZestMoney’s bank balance was INR 20.3 Cr. Of this, around INR 50 Lakh was cash & cash equivalents, while the rest was in short-term FD which was provided as securities amount to the lenders against loans.

ZestMoney’s Downfall

Once the poster boy of BNPL space, ZestMoney was looking to shut shop by the end of December 2023. It’s not clear if the startup has wound up its operations yet or not.

Over the years, ZestMoney raised over $125 Mn in funding from the likes of Goldman Sachs, Xiaomi, PayU, and Quona Capital. It was once valued at above $400 Mn.

The startup’s downfall began after Walmart-backed PhonePe called off the negotiations to acquire ZestMoney. The acquisition talks fell through due to lack of due diligence, disagreements over valuation, and the shareholding structure of ZestMoney. As the acquisition talks didn’t materialise, PhonePe also waived a $18 Mn loan that it had disbursed to ZestMoney. Post this, all three cofounders of the BNPL startup quit.

Soon after, ZestMoney laid off over 30% of its workforce. The startup’s backer, Prosus, also wrote off its investment worth $38 Mn in the beleaguered startup.

As per the financial statements for FY23, ZestMoney also defaulted on payments of close to INR 25 Cr to a financial institution and debenture holders, including Alterica Capital Fund, Trifecta Capital Fund, Ghalla & Bhansali Securities Pvt Ltd.

Meanwhile, DMI Finance and Aditya Birla Finance are reportedly in discussions to acquire ZestMoney in a potential firesale.

Note: We at Inc42 take our ethics very seriously. More information about it can be found here.