SUMMARY

Trade finance is a critical funding source for small businesses, but 45% of global SMEs are excluded from this instrument due to collateral or lack of access to capital

Intending to bridge this financing gap, Polytrade’s cofounder and CEO Piyush Gupta announced the launch of a minimum viable product (MVP) at the 2021 World Blockchain Summit in Dubai

Polytrade’s financing platform will operate on layer-2 blockchain protocol and use smart contracts to bring efficiency and security to the entire process

Small and medium enterprises (SMEs) are universally acknowledged as the drivers of global trade and economic growth. In India, these businesses contribute 37.54% of the GDP and create employment for more than 111 Mn people. But the lack of liquidity in this sector often hinders their growth.

Consider this. An SME has bagged a sizeable overseas order but lacks the funds to fulfil the commitment. In most cases, a buyer refuses to make a substantial advance, and most small businesses fail to meet the parameters of trade finance lending (short-term credit provided to guarantee the exchange of goods) supported by banks and other legacy FIs.

A 2020 report by the International Chamber of Commerce (ICC) says banks reject more than 45% of SME applications for trade finance annually. Raising private loans from the grey market is dicey as high-interest rates (18-30%) mean paper-thin profit margins for SMEs if not downright losses. Even those with adequate funds for ongoing projects fail to finance their long-term growth initiatives, and this vicious cycle could go on ad infinitum.

Piyush Gupta, cofounder and CEO of Polytrade, was no stranger to this prevalent ‘financing gap’ worldwide as he had set up a Hong Kong-based trade finance venture called Riqueza Capital in 2014. In eight years of operations, the company disbursed $500 Mn in seller financing through invoice buying, and Gupta gained some valuable insights into the legacy business model and its loopholes.

So, at the 2021 World Blockchain Summit in Dubai, he announced the launch of a minimum viable product (MVP) — an inclusive trade finance solution that would be run on a blockchain network to eliminate paperwork, do away with business frauds and increase efficiencies (read timeliness and quicker pace of transactions) for better credit/funding guarantee.

Gupta started conceptualising the platform in the first quarter of 2021 along with Arul Prakash (COO), former head of product management at Tata Digital, and Ashutosh Sahoo (chief growth officer or CGO), a marketing professor at SP Jain School of Global Management, Dubai.

The company is not alone in delving into blockchain for a better financial solution for businesses. Ideated by Infosys cofounder Nandan Nilekani, Open Credit Enablement Network (OCEN) has been building blockchain solutions to improve financial inclusion for SMEs in India since July 2020. Taking a similar path, Polytrade intends to innovate trade finance instruments for SMEs.

But before decoding the solutions on offer at Polytrade, we need to look at how the company intends to reshape trade finance with the help of blockchain.

Boosting Trade Finance With Blockchain

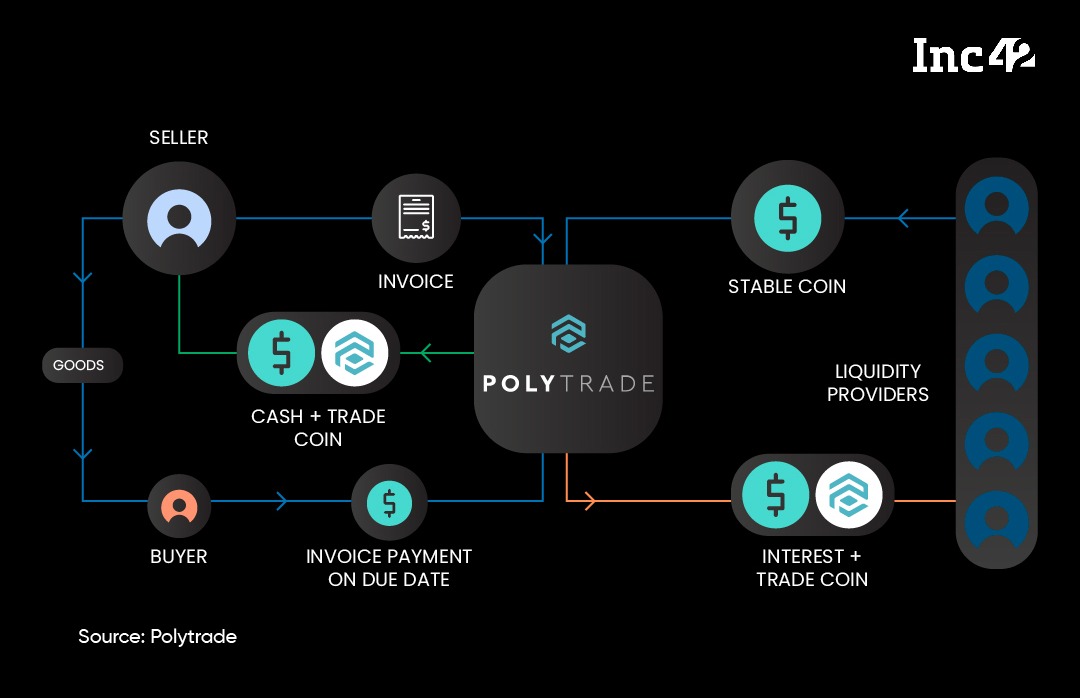

In simple terms, trade finance is a popular method where a ‘finance’ company buys the invoice/s from a seller of goods at a discount and makes an immediate payment, while the full amount is collected from the buyer at a later date. This benefits the seller company as the firm does not have to wait out the mandatory credit period of 60-90 days or suffer from delayed payments.

The buyer company makes the payment as per agreed terms and conditions, and the ‘financier’ also covers the buyer’s credit risk for this period. Like other traditional business loans, this process involves thorough due diligence, collateral from both buyer and seller, a third-party valuation of the goods to be exchanged (including quality, quantity and pricing) and original documents such as purchase orders, invoices, bills of lading and more.

Based on the risk assessment, the seller is given a rate of interest that Polytrade charges in case the buyer defaults. At the time of disbursement, the trade finance startup keeps aside 20% (as reserve fund) of the total invoice amount on which processing fee, interest payment and a small commission fee is levied.

Although the terms and conditions may vary widely when the ‘financing’ happens, Polytrade has kept things simple for the benefit of the SMEs. Here, the invoice amount is disbursed to the seller right after the goods are shipped, and the company deducts a fee from the amount payable. But the crux lies elsewhere.

A quick look at the trade finance procedure mentioned here tells us it can be an excruciating exercise with a high rejection rate that leaves many small sellers in the lurch. Add to that issues like duplicate POs, invoices and bills of lading and a lack of seamless information flow across legacy platforms, and these are bound to increase fraudulent activities. Gupta, however, realised that taking the entire operation to a secure blockchain network could easily address today’s pain points.

To begin with, Polytrade has opted for a layer-2 (L2) blockchain protocol for enhanced security, an upgrade to layer-1 (L1) that largely focusses on scalability. Second, and most importantly, the entire funding validation and disbursement process is built around decentralised finance or DeFi, a financial model that does not rely on traditional intermediaries or require manual approvals for financial decision-making.

Gupta thinks a key reason for large-scale funding rejection could be improper asset valuation as existing FIs follow a standard procedure that needs to be improved. In other words, new parameters must be integrated into the current system to widen inclusivity without compromising on risk assessment. Incorporating them in the legacy system will take a long time, to say the least, and in many cases, a policy overhaul. But with a blockchain-powered platform in place, Polytrade can easily add and update all validation criteria. The company has also added a new metric regarding project completion for better comprehension of business performance.

Polytrade keeps these parameters on-chain, and assessments happen via a smart contract so that the system can automatically validate use cases as and when all parameters are met. The outcome is transparent and tamper-proof as no manual intervention is required at any point. Better still, it only takes up to 10 days to reach an outcome in the absence of manual decision-making. Payments are also done using a smart contract on the blockchain.

How Polytrade’s Vendor Portal Works For SMEs

Polytrade’s platform features three core service areas, and the most significant part includes its trade finance operations via a dedicated vendor portal. Here is how it works:

SME onboarding and risk assessment: Sellers can approach Polytrade and submit applications for invoice selling on this portal. First-time users have to undergo e-KYC verifications and risk evaluations as part of the onboarding procedure. But at this phase, Polytrade reviews a company’s documentation and historic performances manually (off-chain) to ensure that only the most eligible businesses get registered on the platform for funding. According to Gupta, this procedure is completed within 24 hours compared to 7-14 days taken by legacy FIs.

Approval from credit insurers: The next step includes getting a guarantee against the PO/invoice. The company works with many off-chain credit insurance agencies worldwide that conduct their due diligence for both the buyer and the seller before approving or rejecting an application based on the risk exposure. This takes about a week to complete.

Validation by blockchain: Once an external agency approves an invoice, all relevant data is added to the blockchain by the Polytrade team, and a smart contract automatically checks it against the set parameters and disburses the invoice amount to the seller.

User-friendly to the core: A key challenge is to keep the user interface simple and uncluttered as the company is targeting SMEs that may not be too familiar with blockchain setups and find it difficult to navigate a complicated, tech-heavy site. So, Polytrade has developed a user-friendly interface similar to a mobile application. Businesses only have to fill in the data and add documents at designated spaces, and they will be notified when their applications are approved.

Building A Crypto Pool Via Lender Portal

After creating a vendor solution for smooth trade finance operations, the next challenge is building a liquidity pool so that the lack of finance does not hold back businesses. As a blockchain-first company, Polytrade has decided to onboard cryptocurrency holders (a mix of retail and institutional investors) to stake their stablecoins on its lender portal.

Staking is the process wherein lenders provide their cryptocurrencies to a network to fund the pool. In turn, the network rewards the stakers with additional coins. The lender portal of Polytrade helps create a liquidity pool for funding businesses. The lenders can also earn rewards (extra coins) for their role on the platform.

Similar to peer-to-peer lending that assures a steady cash flow when one invests some surplus money, crypto lenders on this platform will earn 6-8% interest, a much higher rate than the average market returns of 5% or less. Polytrade says it is able to provide higher rates by giving out a percentage of its commission earned on business transactions.

A seller can opt to get funding in stablecoins or fiat currencies. The company will use crypto exchanges to convert its stablecoins to make things easy for Indian SMEs. As India has yet to decide on crypto’s legal status, all such conversions will be done overseas, and only fiat money will be paid to sellers through bank transfers, thus removing the impact of any negative regulation towards cryptocurrencies, now or in near future.

TRADE Coins To Drive Tokenomics

Polytrade will also launch the platform’s native cryptocurrency called TRADE coins. These will have multiple use cases and help build trust among various stakeholders. Both sellers and buyers will be eligible for TRADE coins as an incentivising tool, while lenders will get it as a reward on top of interest for funding the crypto pool and validating transactions. A buyer with a high number of coins will indicate higher creditworthiness, and extensive collections held by lender-validators will signify their impeccable track records.

Another use case will be ensuring the registration of genuine sellers with long-term business prospects. At the time of its public launch, the Polytrade platform will be free for all, and any business meeting its existing parameters can raise trade finance. But going forward, there will be only paid access, and sellers will have to buy annual passes using TRADE coins to operate here.

The startup intends to use an optional parameter at a later stage wherein sellers will receive a reduced rate of interest as long as they raise an invoice in multiples of 100 of the TRADE coins’ value held by them. For instance, if an SME has $1,000 worth of TRADE coins, it will get a discounted rate of interest for raising up to $100K.

TRADE coins will also be used as a governance mechanism to identify the highest stakeholders who will be allowed some decision-making power in running the protocol.

The total number of coins have been fixed and pre-minted at 100 Mn tokens.

Of Admin Portal And Contingency Plans

The final block in the Polytrade network is the admin portal that controls the rest of the applications. It will add new guidelines, change parameters, deploy new processes, mandate documentation and carry out other administrative functions. This is the only part of the platform that is not entirely automated and requires manual intervention. However, the company claims that such interventions are exceptional, and normal workflow will remain automated.

The admin portal will also perform tasks like requesting additional documents, validating e-KYC status and sharing the details for the financing deals. Gupta describes it as the bridge between DeFi and centralised financing (CeFi) for seamless operations.

Although Polytrade has a three-layered risk assessment system in place, it has prepared a set of contingency plans in case of defaults. In case of a shortfall after credit insurance payout or if a lender wants to withdraw his stablecoins when the company is facing a liquidity crunch due to payment default/s, it will prioritise settling the lender’s account. In such a scenario, Polytrade will use TRADE coins to settle its liabilities.

“The lenders are essentially providing us with a safety net. So, retaining their trust is most important for us. They will be paid at the earliest even during a contingency,” says Gupta.

Polytrade has also partnered with the SME Chamber of India for the year 2022 to help increase its market penetration. The partnership will enable the trade finance startup in spreading more awareness for its blockchain solution.

The long-term plan is to create a metaverse for trade finance where the entirety of the operations will take place on-chain. Working in that direction, the company has already onboarded Bengaluru-based Polygon (previously MATIC), a blockchain scalability platform, as its first customer, that will help Polytrade build a completely decentralised trade finance protocol.

Polytrade has told Inc42 that it will initially launch the lender portal in December this year to ensure adequate liquidity before hitting the market. The final product is set to be released in the first quarter of 2022, and the subsequent transition of processes to blockchain will continue until the second quarter of 2023.

Given the current scenario, the need for a systemic change in trade finance has never been so essential. In 2019, the Asian Development Bank published a report that said $1.5 Tn worth of trade finance requests are rejected every year, and it can go up to $2.5 Tn by 2025. (To add context, the UK’s GDP in 2019 was $2.83 Tn). However, such massive gaps also signify huge growth opportunities for trade finance companies like Polytrade, provided the blockchain technology proves its effectiveness in risk management.