The story of immense prospects for growth of SaaS model in India is now well established in the circles of entrepreneurs and institutional investors. The market currently is largely outward facing and the destiny for Indian companies is majorly dependent on growth in the global markets. This however, is not bad news. The global SaaS market for 2015 stood at USD 31 billion as per NASSCOM and is expected to grow at a CAGR of 18% to reach a market size of USD 72 billion by 2020. Indian SaaS market is expected to exhibit an even steeper rise, growing at CAGR of 27% and breaching the USD 1 billion mark by 2020.

It is absolutely critical however, that the growth story is embraced by venture capital and private equity funds, for they will be a very important cog in the wheel. The deal activity so far indicates that we do not have much to worry in that aspect. Investors are keen on scalable B2B business models as the caution has returned to the cash guzzling B2C ecommerce segment. It seems that most of the major B2C categories have been played out with emergence of two or three top players clearly established.

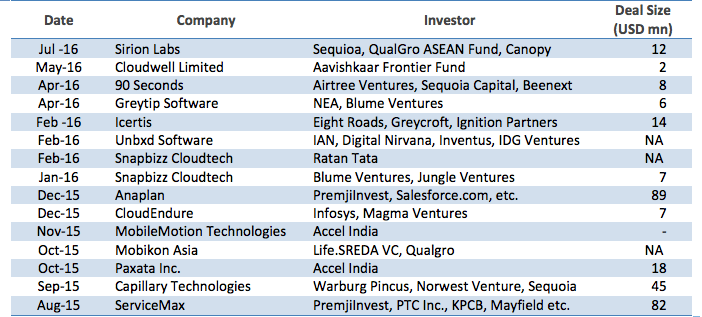

Table 1: Select recent investments in SaaS companies

The funding momentum is expected to continue in the medium term as the ecosystem grows. As per NASSCOM, over 40% of India’s total 150 SaaS firms have been founded post 2010. The quantum of deals will see a major jump once few of the companies reach scale through recurring revenues. As more and more entrepreneurs take the leap, the growth path that the new companies adopt will be key in differentiating the successful from the ‘me too’. Raising investment should not be confused with success, because if the cash is not deployed in a strategic manner, failure can be swift. Companies in the B2B segment are mostly young. Hence there failure does not make headlines yet. However founders would do well to draw lessons from a spate of shutdowns in the B2C segment such as Peppertap, and Spoonjoy. For the more curious, a must read case study could be the rise and fall of Webvan, a company that had managed to raise USD 800 million from marquee names Sequoia Capital, Softbank and Goldman Sachs, before filing for bankruptcy way back in 2001.

The Discovery Phase

The need for establishing a product market fit is often highlighted for SaaS companies in the initial phase, and rightly so. The business model for a SaaS company may look a lot different within 2 years from the idea that led to their incorporation. In this period, the founders should channel all their energy towards finding the elusive product market fit. A desirable product will not be built just by coding software in dimly lit room, cut-off from any and all human contact, the most comfortable habitat of some of my most talented coder friends. It will be an iterative process involving the most critical stakeholder – the customer. It becomes extremely important to have a few potential customers who are ready to try out the product and provide feedback. A typical cycle would involve building one product, listening to customer feedback, and iterating till the product is nothing less than exceptional.

Expectations of generating revenue in the early phase would more often than not lead to disappointment. Hence it is absolutely critical to minimize costs in the early phase. Hiring too many sales people is a luxury which should be avoided, even if you can afford it. In fact the founders should ideally be the only sales people employed to minimize cash burn. As for the funding, the lesser the number of chefs at this stage, the better it is. This phase should ideally be bootstrapped with the good graces of family and friends. Raising external funding at this stage can in fact be counterproductive. Buoyed by infusion of funds, if a half-baked product is marketed, it can lead to closing of doors with potential customers for good.

Acceleration

Once the “Eureka” moment of achieving product market fit is achieved, the next phase of growth can begin. At this point the product should have evolved to a phase where potential customers find it value accretive and scaling up to add more customers becomes viable. The feedback and improvement process should never stop, however the focus should shift from making fundamental changes to adding features.

The customer acquisition costs (CAC) at this phase may be high, hence it is absolutely critical to make sure that the customers adopt and get used to the product. Rather than approach a customer at the end of contract, the sales person should be in continuous contact with the customers in the initial phase to make sure that the product is well understood and used to maximum potential.

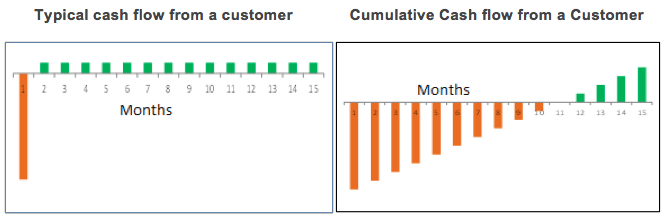

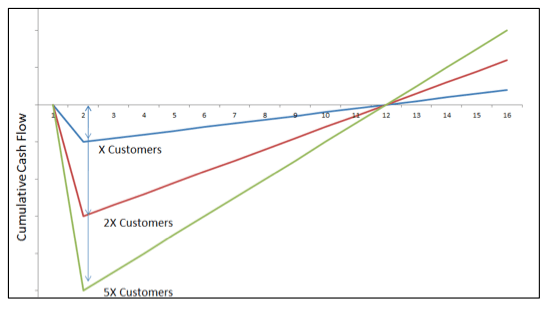

This phase will require investment into skilled sales personnel, which in turn requires cash. An angel or VC at this stage would be ideal to support the entrepreneur. The long term business model for the company will now become the focus. SaaS models typically front load CAC with a long tail of recurring revenue A typical SaaS company will exhibit a hockey stick free cash flow curve and rapidly increasing operating margins with scale. At any investor meeting, the unit metrics of acquiring a customer will always be at the fore front. Monitoring a few key metrics can help to keep a handle on cash burn.

Customer Acquisition Costs: CAC can be a simple measure calculated by Aggregate Sales and Marketing Costs for a period/ Number of New customers added for that period. It will vary depending on whether your customers are SMEs or large corporates. SaaS models have high upfront CAC which is slowly offset by periodic revenue inflow.

Hence the funding requirements should be linked to the schedule of customer acquisition and billing growth rate. New Companies may target a billing growth (quarter on quarter) of at least 10%. Anything above that would definitely make investors sit-up and take notice. If a company goes for acquiring a large number of customers at the same time, the cash flow trough will be deeper, needing more infusion at one time. For a consistent product CAC, should ideally go down with maturity.

Churn: The success of a SaaS (or any other company for that matter) will depend on how successfully they can keep customers coming back to their offering. Losing a few customers along the way is natural, however companies should strive to keep the churn below 5%. This stands true for both customer churn as well as revenue churn. Adding new customers cannot compensate for losing old ones as you don’t incur CAC for retaining customers. Post sale contact by sales person is critical to reduce churn. A customer, who struggles with the adoption in the initial phase, is less likely to renew subscription at the end of the contract. It’s somewhat akin to purchasing a gym membership, where in if the customer is most enthusiastic about using the resources at the beginning, and tapers off, if not paid attention to. As the company grows in scale, controlling churn keeps on getting more important.

Average Billing Period: The billing period or the length of the contract varies from monthly to quarterly to yearly. It should ideally move to longer tenors as the customer becomes more comfortable and reliant on the company’s products. However, since it could largely depend on the vendor payment processes of large clients; companies should not lose sleep over the billing period.

Life Time Value (LTV): The LTV per customer will dictate the pricing matrix of for a company. It can be defined as Average Gross Margin per Customer per month * Average Life of Customer in months. The Gross Margin from each customer over the life time must move upwards either by upselling a more premium product or cross selling other services to the same customer.

The LTV and CAC together provide one of the most tracked metrics of a SaaS company i.e. the LTV/ CAC ratio. A ratio of 3x to 4x is considered acceptable for most business models globally. The product pricing should ideally be done in a way to recover the CAC within one year.

A whole host of other ratios may be derived from the above data points. Promoters will frequently run into terms such as Monthly Recurring Revenue and Dollar Revenue Retention. Unit metrics may be built for customers, products and even sales personnel. Detailed review of such metrics can run in to tens of pages.

The good news is that founders of most of the SaaS companies typically have a special place in their heart for numbers and analytics. The same is true for the professionals at Venture Capital and Private Equity funds. Hence, most numbers can be easily tracked and corrective action can be implemented to ensure a smooth journey towards scaling up.

The emergence of the next billion dollar SaaS company from India is not that far away. In fact, the space is large enough for multiple such companies to emerge specialising in different product segments and industry segments. SaaS is currently below 10% of the overall software sector in India. With the weight of institutional investors behind them, we will see this number changing rapidly.