SUMMARY

With consumer companies and marketplaces like Xiaomi India, Amazon, Flipkart, Zomato offering loans and creditline — is it competition or scope of collaboration for lending companies?

Unlike full-stack offerings by digital NBFCs and lenders, loan products from consumer tech companies are consumption-driven and linked to platform transactional data

Lending startups believe that most consumer companies are not serious about lending, but only using it to retain customers instead of opening up the data for use in the market

Right before its IPO in 2018, tech giant Xiaomi had pledged to make only 5% profit from its hardware products, a declaration consumer electronics companies seldom make. This led to the follow-up question: How does the company make profits then?

To this, Manu Kumar Jain, VP of Xiaomi and MD, Xiaomi India had said, “Our focus area is users and not making a profit. The secret of Xiaomi’s success lies in its marketing and advertising strategies — the biggest concern for most of the companies — an area where Xiaomi spends zero.”

While zero spending on marketing is not the case anymore, the focus on users is a lot more pertinent to the revenue model of India’s largest mobile vendor by shipment. After having launched UPI payments wallet, Mi Pay last year, the company has also ventured into digital lending with Mi Credit which offers personal loans as well as gold loans of up to INR 2 Lakh.

But, Xiaomi is a late entrant to the world of lending. In the last few years, there has been an increasing number of consumer tech companies, payment apps, and more entering the lending tech business.

Decoding the idea at The Product Summit 2020 by Inc42 And The Product Folks, Ashneer Grover, founder and CEO of payments and lending startup BharatPe said, “Like other entrepreneurs, I too received multiple suggestions that we should do this, this and this. However, for me, the key question was how I am supposed to make money out of these solutions that we are trying to offer. Is it going to be through lending? If so, then why not to enter lending directly instead of circumventing it!”

Seconding this view, Anuj Kacker, cofounder of MoneyTap, said that lending is the only business that makes money after all. That’s the key reason why everyone wants to get into lending. In the Payments business. Unfortunately, with MDR becoming near zero, there isn’t too much money in it.

While a payments app or platform entering into the lending segment does not seem too much of a stretch, but when tech companies such as Xiaomi, Flipkart, Zomato, Swiggy, Realme, Oppo, WhatsApp, Amazon, who are turning into India’s proxy lenders, make a move in this direction, it could become a big threat to digital lending startups.

With their huge and nearly unmatchable reach, these mega startups and tech giants possess the most important asset in the modern digital lending — the financial data of businesses working with them as well as behavioural and transactional data of consumers.

But, is having data the be-all and end-all of lending business? What are the opportunities and challenges ahead for consumer companies while entering the lending subsector? And, most importantly, what’s in it for the digital lending startups?

The Thirst For Alternate Lending Data

As with most fintech segments, digital lending is a game of data. Without the right credit scores or alternate lending data, lenders simply cannot take a good call on whether to give out a particular loan or not.

While India has over 504 Mn internet users as per the latest Nielsen-IAMAI report, the country’s credit and debit card penetration is woeful. According to the RBI, the total number of credit cards has only increased from 57.6 Mn in July 2020 to 57.83 Mn in September. Taking debit card numbers into account, the total number of card users has increased from 909.9 Mn to 916.54 Mn during the same period — how many are used online is not clear as debit cards are also proxy ATM cards for many bank customers.

Card transactions help immensely in building one’s credit bureau information that formal lenders analyse before extending secured or collateral-based loans. Given that people who can afford credit cards usually end up having multiple credit cards and the actual number of unique credit card users is not even 0.05% of the entire population, there remain over a billion people who are not able to get access to formal credit.

CIC Experian has referred to this as a 300 Mn opportunity of an unpenetrated market in the Indian fiscal pyramid. As per the TransUnion CIBIL report, about 30.5% of auto loan originations and 34.7% of personal loan originations in the July-September quarter were to borrowers in the below-prime category, a rise of 3.5% and 8.3%, respectively, over the corresponding quarter a year ago. This is where alternate data comes into the picture, and why digital transactions using debit cards are also being encouraged.

While banks have shied away from entering the sub-prime segment which lacks adequate banking data, ecommerce and payments companies that have witnessed a Himalayan rise in terms of their volume of transactions are banking on this data to offer credit products. The beauty of these products lies in the collateral-free nature which makes them easily accessible to the masses. However, these credit products address a very limited section of consumer finance and business finance.

“I think objectively it will enhance the efficiency of the consumer or the business lending segment. So, it leaves something where there is a fundamental demand and something which is leading to a better consumer experience,” Abhijit Ghosh, CEO of SME lender U GRO Capital, said.

The trend will only rise with companies trying to gather an individual’s non-banking data or alternate data in order to extend loans to everyone — even those with a credit history.

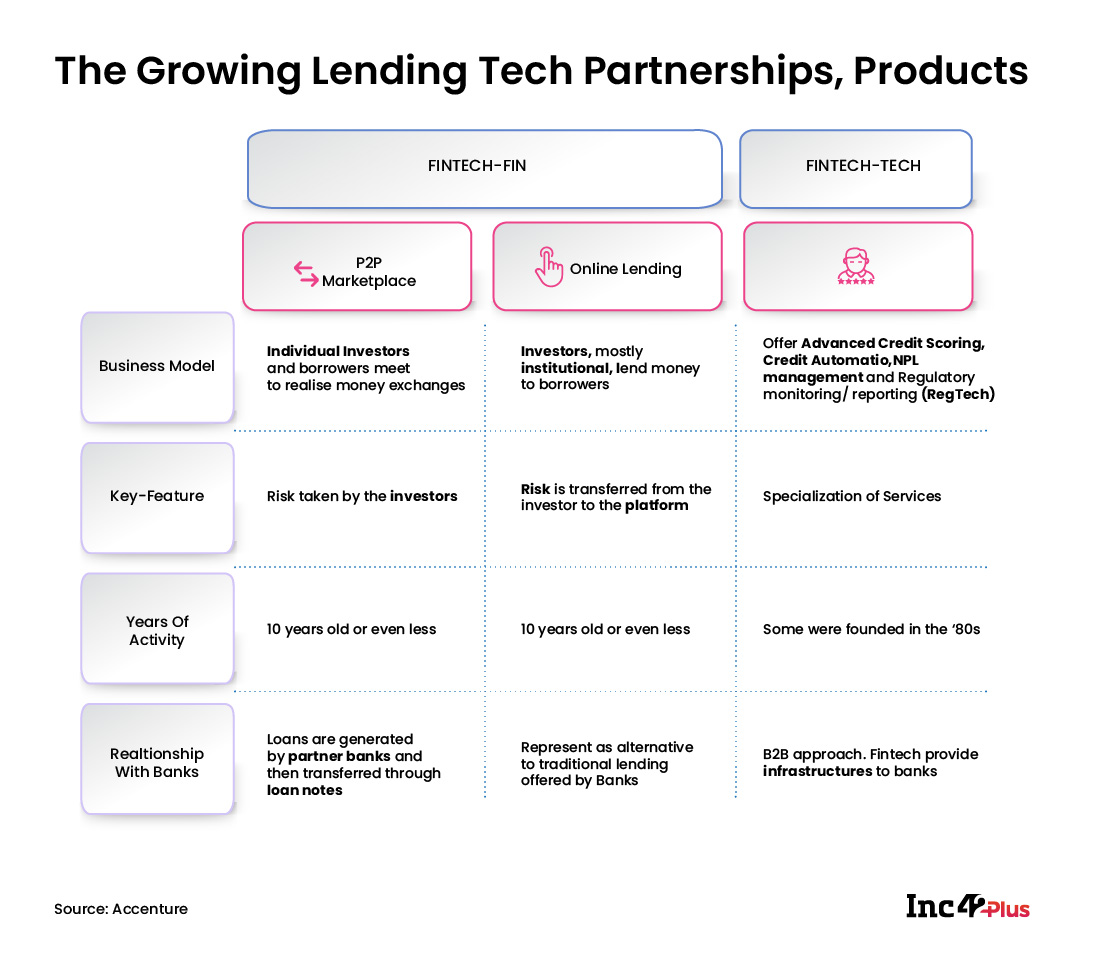

Last year, the RBI in a letter to banks and NBFCs had stated that appointing agents and permitting them to access the database of credit information companies is a direct violation of the Credit Information Companies (Regulation) Act, 2005 (CICRA). Banks and NBFCs would have to face penalties if this happens again. Amid these data protection norms, lending startups have been looking out to generate alternative data which could further be the base for lending products. This has also resulted in increased partnerships among fintech companies, ecommerce and consumer companies.

The Big Game: Numbers And Consumer Retention

One of the key factors driving consumer tech companies into the lending game is, of course, that it’s a user retention tool. Put simply, users on loan books, even if a company like Xiaomi is only a loan originator, are more likely to feel a sense of loyalty because the company has seemingly taken a risk on the user’s behalf. It’s an age-old and useful tactic that has been revived by tech startups, whether to retain users or service partners.

Back in 2015, leading car-hailing platform Ola had started offering daily car loan repayment schemes for its Ola drivers who otherwise would have been unable to buy a car. The amount was anywhere between INR 600 to INR 1,500 depending on the model of the car.

Later, Uber too launched a similar scheme for its drivers. Besides, both companies have also partnered with lending companies in order to be able to offer micro-lending services to their drivers. However, the aim and opportunity in these cases is totally different from that of a lending startup. It was to arrest the flow of drivers to rival platforms. Some would argue that features such as daily loan repayments create a captive service partner base and eases operations in many cities.

It’s another story that the SBI later suspended its partnerships with both Ola and Uber amid mounting defaults and Ola which currently offers Ola Money Postpaid and Ola Credit had applied for NBFC licence from the RBI last year. Car marketplace Cars24 has also applied for an NBFC licence to offer similar financial services to the automobile market, while Droom acquired NBFC Xeraphin to enter the credit market for automobiles.

In the case of Amazon, Flipkart, WhatsApp and Xiaomi’s Mi Credit, the goal is more inclusive — building an ecosystem that could help retain users and consumers. Despite having a large consumer base, all four companies have been running on low-profit margins.

While Amazon India and Flipkart have been running on huge losses, WhatsApp, despite having over 400 Mn users in India, has reported just INR 57 Lakh in profits in 2019. Facebook, since its acquisition of WhatsApp, has been trying hard to bring in monetisation to WhatsApp through payments and the next big area could be lending. While the company has officially not revealed any plans of becoming a digital lender, reports suggest that WhatsApp would bank on its potential user base of local retailers and kiranas to become the default hyperlocal app for rural India and consequently a financing partner for those retailers. It remains to be seen how much of this pans out given that WhatsApp has still not fully launched its WhatsApp Payments product in India.

Similarly, if Amazon and Flipkart, both boast of having over 100 Mn registered consumers in India, Xiaomi, with over 30% market share in the smartphone business and a healthy lead in the smart TV and home electronics segment has been the largest smartphone vendor in the Indian market. With lending products and features, the idea is to enable and add more consumers as well as retain them since loan tenures range from three months to over three years.

The lending products offer consumer companies an opportunity to bring in more transactional data during the same period. If the consumers have been able to pay on time, the data enables them and their lending partners to come up with more customised and increased creditline offers, thereby creating a long term association with consumers. Furthermore, there comes a plethora of networking, partnership opportunities.

But again, the thought is never about replacing financial services players, which is perhaps what makes lending startups more confident about consumer companies not being a threat.

Amazon, which had ventured into lending back in 2011, has issued $5 Bn across more than 20,000 SMBs in the US, Japan, and the UK till Q1 2019. The company has entered into dozens of partnerships across the globe. In India alone, it has partnered with ICICI, YES BANK, Bank of Baroda and more for interest-free EMIs and other credit products. The company also offers creditline i.e. Pay Later facility through Amazon Pay to its customers.

Foodtech giant Zomato has tied up with lending startup InCred to help partner restaurants and cloud kitchens get easy credit facilities and loans. Similarly, Ola, Uber have made multiple partnerships with fintech startups, banks for offering loans, insurance and payment solutions to driver-partners. But they are also turning into potential loan origination partners for digital lenders and other consumer companies into lending.

Threat To Lenders Or Healthy Competition?

The growing trend is largely in sync with the Open Credit Enablement Network (OCEN) and account aggregator (AA) model which would enable lenders and consumer tech companies to come up with a bucket of customised credit offers for consumers as well as MSMEs. However, this might take 12-24 months to be implemented, according to Mithun Sundar, CEO of Lendingkart Finance, one of India’s largest digital SME loan providers.

Meanwhile, there is a huge deficit in terms of supply, availability of data as well as standardisation of the entire loan procedure. For instance, there are lending companies that take weeks for approval, then there are companies that approve the loans at a click. Besides digital lending startups, consumer tech companies entering the space and their partnerships with NBFCs and lenders have in fact made it easier for companies to mine data cumulatively and approve lending products instantly.

Drawing the bigger picture, InCred’s Saurabh Jhalaria said that it is about increasing the penetration in India. So viewing it as a threat to lenders is narrow.

“Out of 40 Cr eligible borrowers, hardly 5 Cr -10 Cr are covered under the formal channel. This leaves a bunch of people in need of access to credit and these people are now building their credit history through checkout finance. Some of these occur at the point of sale and that’s how they are now being inducted into the world of lending. Thus, these consumer companies are helping add a significant number of people to the lending and build their on-time EMI payment habits,” Jhalaria said.

Like Jhalaria, Paisabazaar’s business head Gaurav Aggarwal asserted that one must not forget that the goal of consumer companies is always to boost consumption of their platforms. This is because of the sheer nature of these consumption loans, these loans are typically for smaller amounts and for shorter periods. Even if consumer companies are lending, the nature and goal of these loans are not the same as of a lending company, added Aggarwal.

Digitising Traditional Indian Lending

With India being a consumption-driven market, lending as a business and credit offerings by consumer companies have co-existed in India since time immemorial. Amazon, Xiaomi, Flipkart, Ola, Uber, Zomato and others have simply formalised what has always been there in the informal market of India, said founders for several startups.

Kirana stores have been maintaining hand-written ledgers, extending short-term or rolling credit to selective buyers. The buyers are used to paying the same after a month or so. Similarly, retailers buy products from wholesalers and pay later. So the sub-prime segment of Indian consumers is well familiar with this credit-based buying. Something that consumer companies today want to leverage on.

The nature and range of consumer companies’ loans are limited in comparison to the full stack products offered by lending companies, Vishal Chopra, founder and CEO of Moneyonclick, argues.

“Flipkart and Amazon offer credit features over products like TVs, fridges and so on. The consumer companies are not going to offer you loans for marriage of a family member or education of a brother or medical treatment. This is what we are for,” Chopra said.

At the same time, one also needs to understand that lending companies are not very keen to offer loans for consumption, particularly in bad times like pandemic. They don’t consider consumption as a right choice for loan applicability. Therefore, barring a few such as Mi Credit which offers gold loans as well as personal loans, most of the consumer companies are extending credits in categories or areas where lending companies do not directly want to cater to.

In the Moratorium Conundrum article of this Playbook, we have discussed how demand and supply were badly hit during the lockdown. With banks having stopped issuing the fresh loans, and a significant number of consumers unable to pay their existing EMIs on time, consumer companies were severely impacted. The lockdown has impacted consumer companies equally, believe lending startups.

Short Fling Or Serious Affair?

Right from offering working capital loans, loans for new businesses, educational loans, farm loans to home loans and car loans, entering lending is way more serious than simply lending for consumption, personal finance.

MoneyTap’s Kacker argued that just because consumer companies have access to customers and their data, it does not mean that they can run a lending business. It is way more serious. It is about streamlining the entire operation right up to the collection part.

So far, for consumer companies, lending has been offered as a feature, not as a business product, he added.

Similarly, Anubhav Jain, founder of lending startup Rupifi, which is looking to play a bridge role under the OCEN model between lenders and borrowers, believes only one out of nine consumer companies are even serious about core lending. It is unlikely that even among those any would compete with digital NBFCs and lending startups in the long run. Jain said most consumer companies either want to enable more customers to buy their products or want to monetise the data directly. In both cases, they don’t need to enter lending, but have a choice to partner with the ecosystem, which helps minimise the risk involved in lending.

Given the fact that there is no match between supply and demand, as far as lending is concerned, the role of consumer companies has only helped meet the unmet demands, creating a huge chunk of partnerships and product models for lending companies. Like MoneyTap’s Kacker, the true-blue lenders are not particularly worried about the competition and look at it as a way to expand the potential customer base and create better borrowing habits.

“Core lending is way more serious than flirting with it to promote consumption.”