SUMMARY

A Quick Look At The Potential $500 Bn Indian Digital Payments Industry And The Recent Developments

If India’s ecommerce sector was dominated by the Flipkart-Snapdeal merger these few last months, the Indian digital payments sector was a story of many firsts. In the last month, major Indian digital payment players like Paytm, FreeCharge, MobiKwik made headlines in their own way. And not to be left behind were emerging players like Amazon Pay, WhatsApp, Hike and Google, who are making quick moves into this space.

From a stake sale to an acquisition to capital infusion and to ambitions of becoming an all in one platform, India’s digital payment players each had a unique tale to tell for 2017. And the reason behind this is simple. The Indian digital payments industry is projected to reach $500 Bn by 2020, contributing 15% to India’s GDP, as per a recent report by Google and Boston Consulting Group.

As revealed by the report, by 2020, non-cash (includes cheques, demand drafts, net-banking, credit/debit cards, mobile wallets and UPI) contribution in the consumer payments segment will double to 40%. Already 81% of existing digital payment users prefer it to any other non-cash payment methods. Indian consumers are 90% as likely to use digital payments for both online as well as offline transactions.

Indian digital payments industry is projected to reach $500 Bn by 2020.

No wonder, all the digital payment players are gearing up to leverage this rising tide of digital consumers in the coming years. They are doing so by pivoting or joining hands with traditional players such as banks and NBFCs to be able to garner a significant percentage of the 520 Mn smartphone users predicted in the country by 2020 in the Google and BCG report.

From Chat To Cash And Vice Versa: Whatsapp, Hike And Paytm

It all started with the news of Whatsapp’s entry in the digital payments space. This came right after WhatsApp co-founder Brian Acton visited India in February 2017, where he hinted that the company was looking into how it can incorporate payment services for its users.

In April 2017, a report by The Ken (paywalled) confirmed that the instant messaging app is expected to launch a peer-to-peer payment system in India. The interface is likely to be powered with the Unified Payments Interface (UPI) and is expected to launch within six months. Whatsapp has also reportedly approached SBI and NPCI for enabling UPI payments on its digital wallet.

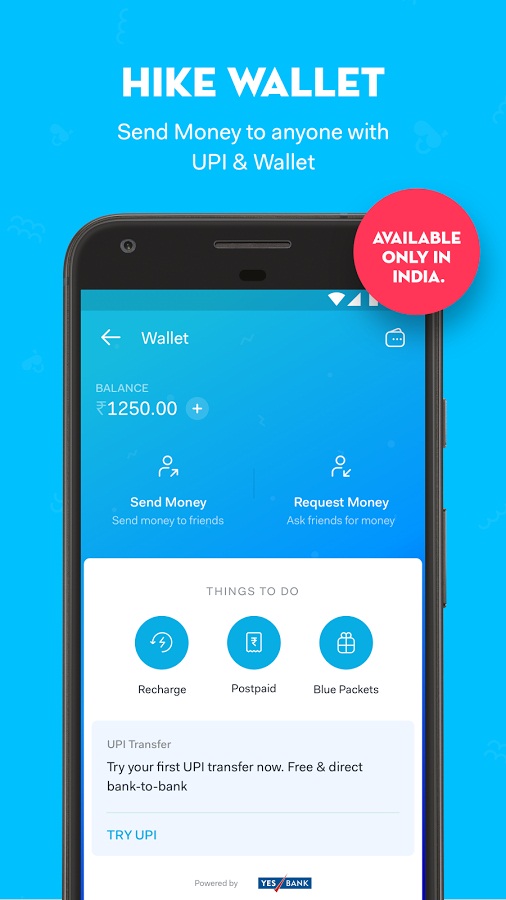

However home-grown unicorn, Hike Messenger jumped the gun and launched a UPI-enabled digital wallet – Hike Wallet – months ahead of the proposed launch of digital wallet of rival WhatsApp in India in June this year. YES BANK is the banking partner enabling the Tencent-backed company to launch UPI and the mobile wallet. Consequently, users can make free bank-to-bank transactions via UPI. This functionality will even work for users not in the messenger app.

So, while both Hike and Whatsapp are making a foray from chat to cash, digital wallet Paytm is traversing in the opposite direction-from cash to chat.

Last week, Paytm announced its grand ambition to take on the market share of in-app chat services in India such as WhatsApp and Hike. The Alibaba Group-backed company is now in the process of integrating a WhatsApp like in-app chat service on its native app. With this launch, Paytm is aiming ambitiously to replicate the success of Tencent’s WeChat business model in China.

WeChat’s mobile payment service, WeChat Pay, is the primary payment method for offline purchases in China, with 93% adoption rate across Tier I and Tier II cities. The reason cited for such a wide adoption of mobile for making offline payments is that people do not prefer to carry cash with them. Plus, it’s easy, fast, has cashback and no extra fees for the transaction.

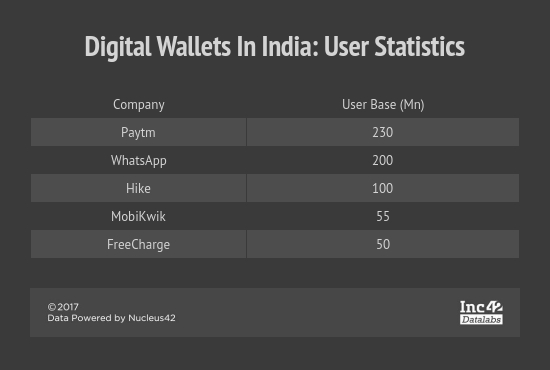

As per reports, Paytm will launch the service in the next few weeks and it will bet live probably by the end of this month. With its current user base of 230 Mn in India, Paytm’s attempt to replicate the in-app chat service model is an attempt to capitalise on its growing user base and increase the number of transactions on its platform. Additionally, this will help the company in strengthening its grip on the Indian digital payments market where other hawk-eyed players have set their sights.

And two of them are tech giants Google And Amazon. But more about them later. First, a look at the other incumbents in the payments space.

FreeCharge And Axis Bank: A Lost Opportunity Or An Ally Gained In Indian Digital Payments Space?

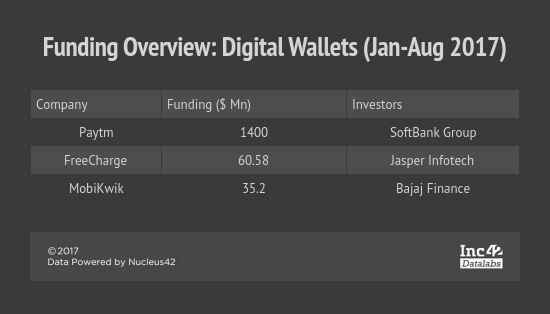

If newer players are lining up to crash the digital payments party, some older players have crashed out of it. One of them was Snapdeal’s beleaguered digital payment wallet FreeCharge, which was sold to the country’s third-largest private sector lender Axis Bank for $60 Mn last month.

What was unique about this deal was that, for the first time, an Indian bank went shopping for a digital wallet and bought it for a mere 15% of the $400 Mn selling price to parent Snapdeal in 2015.

Clearly FreeCharge, despite its early entry into the payments party and its 50 Mn user base, had lost out to rivals Paytm, MobiKwik and PayPal, who also were incidentally in the race to buy it. FreeCharge was not able to capitalise on the boom in payments after the demonetisation drive last year at the pace rivals Paytm and MobiKwik did. This happened either due to lack of resources or proper direction by the management, given parent Snapdeal’s own struggles. But it was clear that FreeCharge had to find a suitable ally if it had to survive.

And Axis Bank rode in as the knight in shining armour, hoping to leverage FreeCharge’s expertise as well as its user base to strengthen its presence in the country’s burgeoning digital payments space. Axis Bank is hoping to double the customer base of the bank through this acquisition and leapfrog its digital journey by multiple years. The acquisition will now give the bank access to high-quality technology that traditional companies usually struggle to build, as compared to agile Internet startups.

A digital wallet at a reasonable price, the agility of an Internet startup and in-house tech expertise all put together fit the bank’s longer term vision of making digital payments a compelling proposition to its customers. While for FreeCharge, this is a second shot to run as an independent business under Axis Bank and a chance to probably reduce a little of the wide gap between competitors. It remains to be seen if the tech advantage which the bank is hoping to leverage will enable it to vault into the same league as Paytm or MobiKwik in the Indian digital payments space.

And that brings us to our next incumbent MobiKwik, which is harbouring the ambition of entering into the Unicorn Club.

MobiKwik And Bajaj Finance: Another Marriage Of Financial Services And Digital Payments

So, while Axis Bank chose to shell out $60 Mn to add a digital wallet to its own wallet Lime, NBFC Bajaj Finance made a strategic move last week by picking up an 11% stake in digital wallet MobiKwik for $35.2 Mn.

For Bajaj Finance, this deal will enable it to offer its customers a complete buying experience, through a mobile wallet. It will provide customers with a one stop solution for all debit and credit spends. Just like Axis Bank, the addition of a digital wallet to Bajaj Finance’s arsenal means it is better equipped to fight upcoming payment banks.

And, of course, just like Axis Bank, Bajaj Finance chose the less expensive way of entering digital payments by acquiring a stake in a digital wallet rather than build a platform from zero, which would definitely have taken more time and resources. Unlike the country’s largest lenders – State Bank of India, HDFC Bank, ICICI Bank and Yes Bank – who have their own wallets, namely SBI Buddy, Payzapp, Pockets, and Yes Pay respectively. Some of these have also forged partnerships with fintech startups. For instance, Chillr has a partnership with HDFC.

Bajaj Finance gets straight access to MobiKwik’s 55 Mn customers. Also not to be forgotten are the 10,000 merchants on Mobikwik-promoted payment gateway aggregator Zaakpay, which was hived off as a wholly-owned subsidiary of One Mobikwik Systems with a separate business head and a dedicated engineering team this May. Zaakpay already counts major players such as Uber, Zomato, Domino’s, Instamojo and IRCTC among the 10,000 merchants on its platform. The company plans to double the number of merchants this year.

For its part, MobiKwik gets more financial prowess to fight rival Paytm as well as inch closer to the ambition of entering the Unicorn club in India, something that co-founder Upasana Taku had revealed earlier this year. This would imply that the funding raised from Bajaj Finance will likely be part of a larger funding round as the company is looking to raise $100Mn-$150 Mn in funding to take its valuation to $1 Bn.

But until the time this transpires, it has at least bolstered its user base with this deal by securing access to the 22 Mn customers of Bajaj Finance.

One thing that is now common to all the three major wallet players is that now they are all more or less associated with financial services firms. Paytm added a payments bank to its folds this year, FreeCharge is now owned by a bank, and MobiKwik now has an NBFC as an ally.

These strategic moves are important given that AmazonPay is already making a quiet splash and Google looking to make a run for the Indian digital payments space in the next few months.

Global Tech Giants Come Roaring In Indian Digital Payments Space

When Amazon and Google are raring to make a go for any space, one can be sure that space is getting hot enough to place your bets on. And this is what can be surmised for the Indian digital payments space as well.

As per National Payments Corporation of India (NPCI) Managing Director and Chief Executive A.P. Hota’s statement last month, Google is in advanced talks with NPCI to integrate its digital payments service, Android Pay, with UPI. The company has completed discussions with NPCI, which has, in turn, requested the Reserve Bank of India to consider the firm’s application. Google announced the launch of Android Pay globally in March 2015. Android Pay is a mobile wallet that can store credit cards, debit cards, and loyalty cards etc. Basically, it allows users to make contactless payments using their smartphone at selected retailers. The digital payment is service is similar to Samsung Pay and Apple Pay.

Hota stated, “Google is testing UPI-enabled payments. The Reserve Bank of India has to look into it. Facebook and WhatsApp are in preliminary talks as well. Google and apps such as WhatsApp and Facebook will have a pervasive presence in India. Such an integration is technologically possible but we are waiting for the Reserve Bank of India’s approval. Such a move can make a difference as these companies can bring in volumes.”

As per Hota, Google is developing a separate India-focussed app, which it will name differently, in integration with a bank. It is expected that Google will launch a UPI-enabled app within the next two-three months for mobile payments. If this happens, it could be a big boost, given that Android is the dominant operating system in India. This also poses a big threat to incumbent players.

But while Google isn’t alone – with Facebook, Amazon, and Whatsapp also in the fray – it might beat them to be the first to launch a UPI-based payment system. Facebook had also announced in March 2015 that it would enable peer-to-peer payments through Facebook Messenger called M.

Similarly not to be left behind in the Indian digital payments race, ecommerce giant Amazon has fuelled an additional $20 Mn (INR 130 Cr) into digital payments entity, Amazon Pay India, as per regulatory filings. In April 2017, the Indian arm of the ecommerce company secured the license from the Reserve Bank of India (RBI) to operate a prepaid payment instrument (PPI). As per the RBI website, Amazon Online Distribution Services Pvt. Ltd secured the licence late last month.

Later in May 2017, the tech giant company had routed more money to the digital payments business, Amazon Pay India. As per regulatory filings with the Registrar of Companies (ROC), the company has poured in about $10.45 Mn (INR 67 Cr) in Amazon Online Distribution Services, through its Singapore and Mauritius unit.

This makes the ecommerce behemoth the latest entrant in the country’s booming digital payments space. And, by the looks of it, Amazon wants to enter with a bang. As reported earlier, Amazon Pay is all set to scale up its wallet business in India by planning to enter into strategic partnerships with government bodies such as electricity and insurance companies. Globally, this year, Amazon Pay’s customer base has swelled to over 33 Mn customers.

Interestingly, a few days ago, the satirical publication The Onion circulated fictional advice for all the determined entrepreneurs from Amazon CEO Jeff Bezos which read, “Value your customers, hire well, find a market that isn’t being served, and realize that someday I will utterly crush you.”

While these words are satirical and not Jeff Bezos’, they are pretty much rooted in reality. When Amazon first entered India in 2013, it gave a big boost to the ecommerce sector, fuelling intense competition as well as millions in investor backing, leading to a dog fight in the space that is now legendary.

Editor’s Note

With a tech behemoth like Amazon quietly entering Indian digital payments space, incumbent players like Paytm, MobiKwik, FreeCharge, as well as those entering in the future, are pretty much warned that the space will be disrupted in a big way. Paytm has a significant head start in the space but as more and more Indians come online, they will be spoilt for choice as far as modes of digital payments are concerned.

As the above-mentioned players make the Indian digital payments space a hotly contested one, not to be forgotten are the numerous other players in the digital payments ecosystem who will also receive a thrust with increasing digitisation. Be it international players like PayPal, or homegrown players like PayU India, (which now has Citrus Pay in its fold), Paynear, Instamojo, CCAvenue (which merged with InfiBeam in February this year), and Oxigen, among others. Recently, the global leader in digital payments PayPal has even announced the launch of two Technology Innovation Labs at the Chennai and Bengaluru Tech centres. The lab is the first by PayPal in India and the third after US and Singapore.

PayPal had been fairly aggressive in 2016. Last year, the company revealed its intentions to grab a pie of the $500 Bn Indian digital payments market by empowering homegrown startups. It also came up with PayPal.me– a peer to peer payment feature targeted at freelancers, casual sellers, and B2B sellers in India to receive payments from customers around the world simply by asking them to click on a personalised link. Similarly, Instamojo, which incorporated a digital wallet in its payment gateway in September 2016, is also hoping to break even and reach 1 Mn users by next year.

In the light of these developments and the onslaught of so many players, how will the Indian digital payments space shape up? Angel investor Sanjay Mehta thinks, pretty well. Sanjay told Inc42, “I would say, the more the merrier. Let the market size grow in multi folds with each platform offering the best value proposition to consumers. I would be excited when I see cross border payments beginning on any one these like RemitGuru.”

Sampad Swain, Co-founder and CEO, Instamojo also believes that big players entering digital payments space is a great move. He says, “This will bring a large swath of consumers into the market with many experiencing digital payments for the first time. Having said that, a lot remains to be done in for businesses – especially for micro and small businesses. That’s the market Instamojo is excited about! Small businesses’ needs extend further than payments like compliance, e-commerce services, logistics, financing, promotions etc. This allows them to sell easily, manage their business efficiently and grow faster.”

But whoever wins or loses, one thing is certain – the Indian digital payments space will benefit hugely. As per Hota, last year, the volume of digital payments was 9.2 Bn, of which 3.5 Bn had been contributed by the NPCI. This year, it is aiming to contribute about 11 Bn digital transactions in India. With Google’s Android Pay, Amazon, Facebook, and WhatsApp aboard the UPI gravy train and pushing hard for mobile payments; this number may be well within the reach.