SUMMARY

The traditional banking sector is rapidly opening up to neobanks as value-added banking service providers

Neobanks are offering sector-specific business management solutions to MSMEs

Experts think regulatory clarity can make the process smoother for all stakeholders

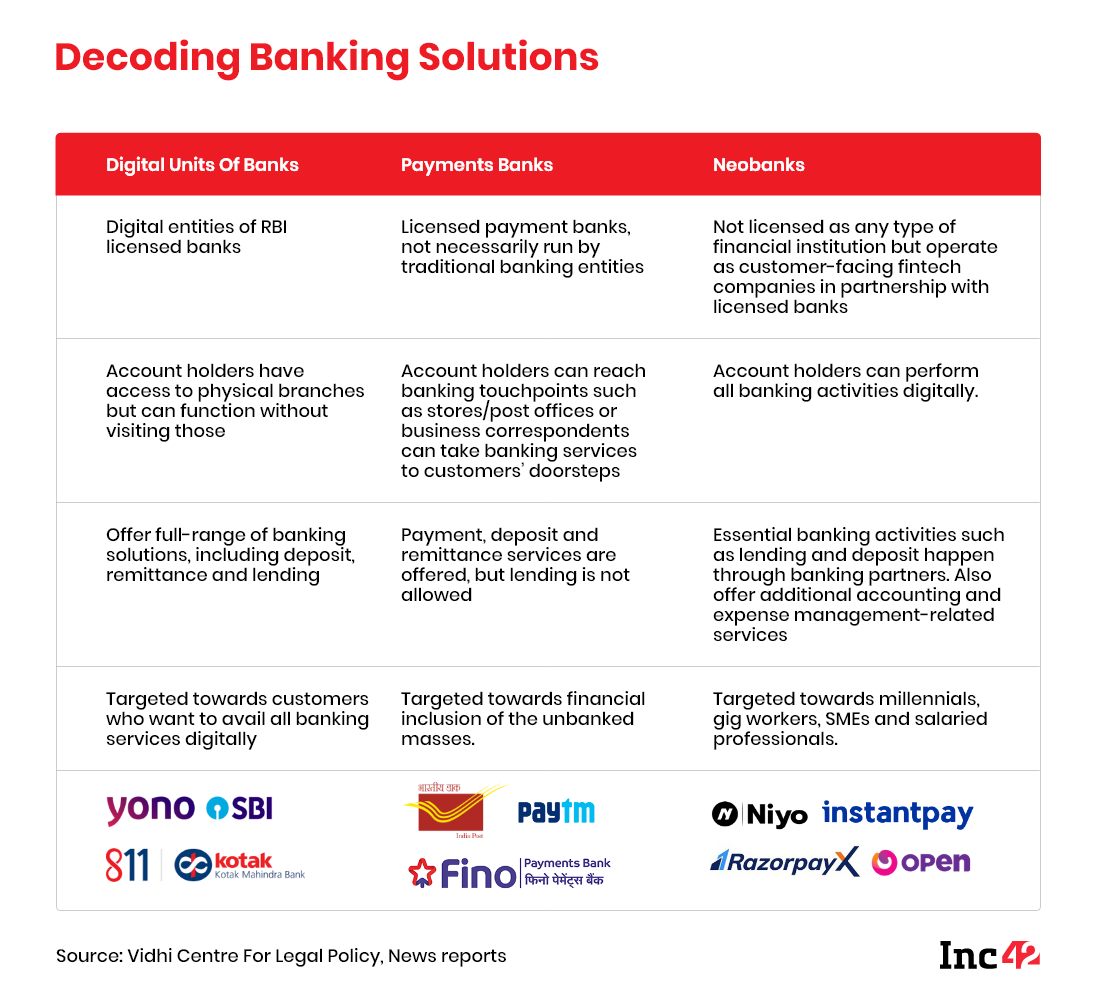

Unlike traditional banks, neobanking platforms do not have their own banking licenses in India yet. Instead, these new-age digital entities partner with traditional banks to offer full-scale banking services to small and medium enterprises (SMEs) and retail customers. The standard fare is already there, be it cash deposit, fund transfer, credit card or lending. But what matters most is the cloud-based digital-only format they have embraced, leading to quick and convenient branchless banking that has found many takers in the Covid-19 era. Of course, their offerings may not seem too different from what payments banks are doing sans the lending component. But neobank customers are more tech-savvy and do not require much hand-holding for basic banking operations.

Neobanks might have got a boost during the current pandemic that calls for restricted movements and digital payments. But the model is now being tailored to meet fast-evolving customer requirements, especially in the B2B space.

More than 15 companies are currently operational in India, including key players such as Open, Namaste Credit, NiYO, SBI YONO, Kotak 811, Hylo, PayZello, InstaDApp, 0.5Bn FinHealth (YeLo), Forex-Kart, Walrus, Neo-Bank, Fin.in and RazorPay X. And most of them have forayed into business management solutions such as cash flow analysis, tax filing, payment collections (generating links to accept payments on behalf of businesses), payroll management and accounting management to cater to their corporate clients. The cherry on the icing is: Neobanks do not have lending curbs like small finance banks as the capital comes from their partner banks’ lending books.

Neobanks have been a draw for investors too, as they are focussing on small and medium enterprises (SMEs), a mostly underserved and untapped market in India. For example, Open Financial Technologies, India’s first SME-focussed neobank, has already raised close $40 Mn from Tiger Global Management, 3one4 Capital and Beenext. According to the MEDICI India FinTech Report 2020, neobanks in India had raised a total of $139.8 Mn in FY2018-19.

Why Open’s SME-Focussed Playbook Matters

With more than six crore MSMEs operating in the country, Open’s focus area has enormous potential compared to legacy banks. The latter has not scaled optimally to provide such value-added services due to their legacy frameworks’ technical limitations.

Open was set up in 2017 by Anish and Ajeesh Achuthan, Mabel Chacko (all of them former employees of the payment gateway firm PayU) and Deena Jacob, former CFO of TaxiForSure. Besides helping small businesses with payments management, reconciliation and access to working capital through lending solutions, Open also offers a slew of GST and tax filing services, which remain a major compliance hurdle for SMEs. One of its key solutions covers payment collections for SMEs, an essential requirement for businesses, the founders say, based on their PayU experience.

As of December 2020, Open has more than 500K SME customers across 15 partner banks and claims to process $15 Bn-plus in annualised transactions. Its revenue model includes pay-per-use charges, subscription fees for premium services and revenue share with app developers on Open’s app store. Its annual subscription plans range from INR 4,999-9,999. Paid plans allow businesses to have role-based access control, low transaction charges for collections and payouts and a variety of services.

The company currently offers three types of accounts – starter, growth and enterprise – which cater to single-ownership companies, slightly larger partnership-based organisations and bigger private limited companies, respectively.

“Even before the pandemic, single-ownership businesses were a major target segment for us and now comprises around 45% of the customer base. Since the pandemic, we have seen many freelancers and even YouTubers, who run their operations online, joining our platform. With our technical solutions in place, we have been able to help them with a web presence and online stores so that they can reach a bigger customer base,” says Ajeesh Achuthan, chief technology officer of Open.

What Is The Scope For Neobanks In India?

Most Indian banks have their own bouquet of digital banking solutions which covers the neobanks’ focus areas. So, does the country require a digital-only model operating in the cloud? For traditional banks already overloaded with thousands of banking applications and APIs, offering such business solutions to small businesses is too much of a distraction.

Ajay Rajan, global head, transaction banking, at Yes Bank, told Inc42 co-owning customers via neobanks (like Kaleidofin and NiYo) has been a win-win partnership for them. “Legacy banks can offer value-added services through neobanks to address a larger market. Whether we offer existing customers HR management solutions through a neobank or whether a neobank customer needs a nodal bank account at the backend, we can co-own these customers and offer plug-and-play solutions for all.” Neobanks and their partners split the fees based on the transaction value.

However, there are gaps in the B2B banking space which neobanks can help address over and above the current SME and retail banking solutions they offer, he adds.

Sanjay Swamy, the managing partner of venture capital firm Prime Venture, concurs, saying that effective partnerships will allow neobanks to serve several underserved markets.

“There could be three approaches here – savings-led, credit-led and wealth-led neobanks. As long as these startups (neobanks) choose the right partners to work with and the right target customers, they will always have an opportunity to do well,” he says.

There is a catch here. Unlike technology service providers which support the banks’ backend tech, neobanks are customer-facing entities. Hence, it requires robust and comprehensive regulatory protections.

According to a recent report by think tank Vidhi Legal Policy, existing arrangements between traditional banks and neobanks under the partnership model is likely to be subject to indirect supervision of the Reserve Bank of India under its outsourcing and business correspondent guidelines. “In the absence of a regulatory framework, ambiguity regarding the role of such neobanking platforms may arise when contracts do not clearly demarcate responsibilities between various actors,” the report notes.

Growth Plans In Covid Times And Beyond

Could neobanks become redundant when legacy banks expand their tech capabilities and offer a whole new range of diversified services? Experts do not think so. “Both (legacy and tech-focussed neobanks) can exist side by side while helping each other grow. Neobanks are simply taking banking services to a wider audience who have specific business requirements. These new entities bear the risk while banks manage the underwriting,” says Siddharth Pai, founder and managing partner of 3One4 Capital, an early-stage VC firm.

A closer look at their services further clarifies how they bring value to users by adding fintech solutions on top of legacy banking services. For example, InstantPay delivers full-stack banking solutions for businesses with instant activation facilities. Niyo addresses the requirements of blue-collar workers and also provides billing solutions to users travelling abroad. As long as neobanks can identify their target market segments, which will be a good fit for their banking and business solutions, there is scope for them to grow.

But there could be major challenges in terms of sticky customers and scaling up as the pandemic and lockdowns have triggered a massive slowdown across sectors. Open, for instance, has to reassess its growth plans. Although the neobank has expected to reach 1 Mn SME customers by September 2020, the target may not be achieved before March 2021. The startup is not profitable yet, but its current focus is on crystallising its banking play. One of the critical steps towards profitability will involve upgrading the free-of-cost starter accounts to fee-based growth and enterprise accounts.

As of now, Open works with partner banks such as ICICI Bank, IndusInd and IDFC Bank. But its plans go well beyond providing partnered banking solutions as it is keen to evolve into a neobank incubator. Achuthan has told Inc42 his company has already spent around two years building its APIs to integrate with other banks. Open wants to take this expertise to fintech companies to differentiate itself from other neobanks who are offering banking solutions only. However, the main chunk of its revenue will still come from its banking solutions. It also provides an end-to-end lending platform, from underwriting to disbursement, in partnership with non-banking financial companies (NBFCs) to position itself as the go-to customer lead generator.

The company did not share revenue details or when it expects to turn profitable, but upgrading its 20% paid subscriber base to more than 80% will be the game changer, says Achuthan.

Achuthan thinks neobanks, especially the SME-focussed ones, have more channels to generate revenue than traditional banks which do not offer business management solutions.

He may not be wrong in his assumption. In November this year, UK-based neobanking unicorn Revolut announced that it had managed to break even just five years after its inception.

“Many other SME-focussed neobanks who launched less than three years ago are on their way to profitability. These banks can definitely become profitable, and you will see a lot of them going for IPOs, driven by multiple monetisation rails which are not dependent on banking services,” says Achuthan.

What are the biggest challenges ahead of them in this market?

Initially, the key challenge was to convince banking partners to come on board, says Achuthan. Now that the company has 15-odd banking partners, Open has reached a position where its solutions are trusted.

“The next phase requires rapidly scaling up our solutions and the team. We want to expand from around 150 to a team of 400-plus across engineering and sales. This initiative will also include taking our services to new markets,” he adds.

The neobank is already in the process of integrating with other neobanks and fintech solution providers in the US so that it can offer its solutions to a mature market. On the funding side, the company is comfortably placed for another couple of years.

According to a 2020 report by Matrix Partners and McKinsey and Company, neobanks are yet to report profitability, but the long-term outlook of this sector remains bullish. However, for long-term sustainability, creating some regulatory frameworks will ensure that banking and neobanking roles are clearly defined, say some fintech experts. Until then, with an active user base of 500 Mn and growing, neobanks have much to cheer about.