SUMMARY

While the RBI is yet to disclose the statistics for credit card transactions since October, UPI transactions during this time are likely to have surpassed credit cards by value

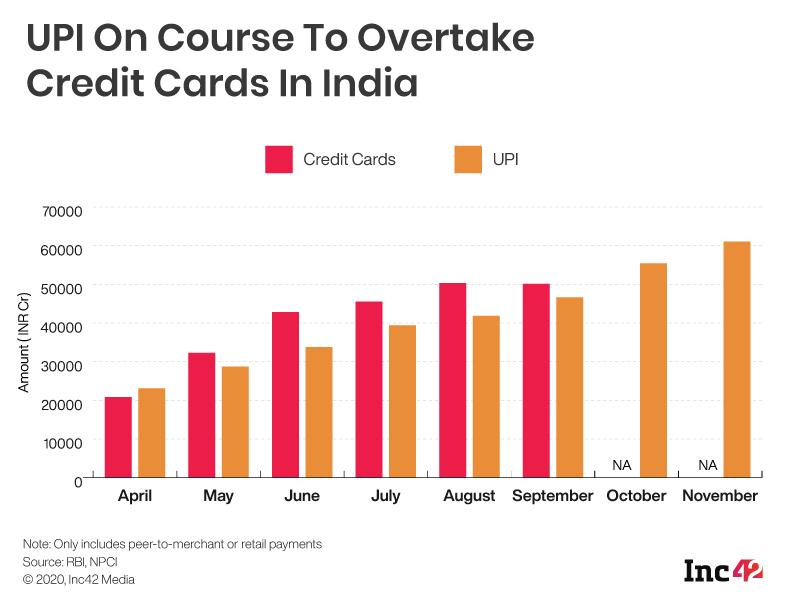

NPCI reported peer to merchant UPI transactions worth INR 61,045 Cr compared to INR 50,139 Cr through credit card transactions in September

As the payments regulator plans to enable credit products and cross border transactions on UPI, card majors Visa and Mastercard face an existential threat from Big Tech companies

With the surge in digital payments brought about by the Covid pandemic, UPI seems to have been the biggest winner as peer-to-merchant (P2M) transaction volumes have risen 12%, 8% and 11% month on month between July, August and September, respectively. During the same period, credit card transactions have grown 6%, 8% and 4% respectively.

Further, the month-on-month growth in value of P2M UPI transactions during this duration has been 16%, 6% and 11%, compared to the slowdown in value of card transactions.

While the Reserve Bank Of India (RBI) is yet to disclose the statistics for credit card transactions in October and November, UPI transactions during this time have grown 19% and 10% respectively by value. It’s unlikely that credit card transactions would have grown faster than this in the past two months to catch up, given the month-on-month growth.

In November, National Payments Corporation of India (NPCI) reported P2M UPI transactions worth INR 61,045 Cr compared to the INR 50,139 Cr reported value of credit card transactions in September. This has naturally prompted industry watchers to question whether UPI will eventually overtake credit card transactions over a longer period, especially after big ticket spending such as travel and hospitality normalise after a weak 2020.

Earlier in March this year, when the entire country went into a lockdown, almost zero footfall across retail outlets led to halving of credit card transactions from INR 50,697 Cr to INR 20,858. On the other hand, UPI based digital transactions have soared since the lockdown as users have turned to online modes of payments and ecommerce to mitigate Covid risks.

“There have been times when UPI has led the way for payments and surged ahead of debit/credit cards in volumes, even during the pre-Covid era. Last few months have cemented that lead. Additionally, there are no transaction charges for the merchant on UPI, which makes it a preferred digital payment option for them. Looking at the growth of UPI over the last few months, I believe this is here to stay,” said Suhail Sameer, group president of QR code provider BharatPe.

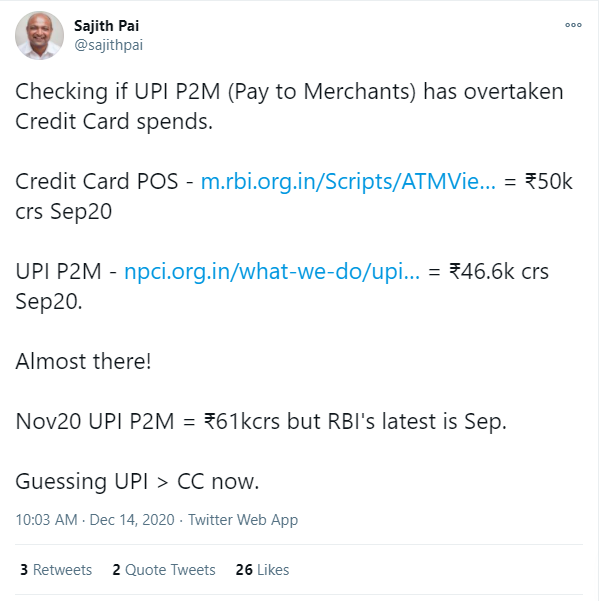

Blume Ventures’ Sajith Pai pointed out on Twitter how UPI transactions for the P2M segment have grown in the past few months to compete with credit card transactions in India, which may be ominous for credit card giants Visa and Mastercard.

Stellaris Venture Partners’ Ritesh Banglani, who has invested in startups such as TaxiForSure, Lifecell, TrulyMadly, Vogo and mFine, however had a different view. He was of the opinion that a true comparison would include debit and credit cards.

As per the data, both debit and credit card transactions took a hit immediately after the lockdown in April. From a high value of INR 141,265 Cr credit and debit card transactions in October 2019 the value dropped over 65% to INR 43,856 Cr in April 2020. As of September the number stands at INR 104,987 Cr.

Card Giants Face Existential Threat From Big Tech And UPI

The credit and debit cards market has long been a duopoly of Visa and Mastercard globally, outside of China where the two firms have been kept out to protect homegrown payments enabler UnionPay until recently. What this has meant is that the two companies together handle 90% of global card payments outside China. In India, the RuPay card has been promoted by the government as an alternative, but has considerably low penetration in comparison to Visa and Mastercard.

The two companies have enjoyed their dominance over the past few decades as payments technology was complicated and once they had built a massive network of customers and merchants across the globe, it was difficult for a challenger to break through that moat. The fact that Visa became the most valuable financial services company in the world ahead of global banking major JPMorgan Chase in March this year is a testimony to the fact that solving the payments puzzle is a huge money spinner.

But that dominance is nearing its end, or so it seems as 55 countries around the world have created national payments systems which can replace the payments rails created by the card giants.

In India, it is UPI which has become an existential threat to Visa and Mastercard. UPI service providers like GooglePay, PhonePe, AmazonPay have managed to make inroads to replace cash for certain use-cases and now they might now also be threatening the credit card turf of the card companies. UPI-based credit products are not far off from launching in the Indian market.

However, at least one of the two card giants is not feeling the heat yet. Porush Singh, division president, Mastercard South Asia told Inc42, “In a market that is still predominantly cash based, healthy competition presents a great opportunity for migrating to cashless practices and bringing innovative payment solutions. With over 138 Cr population, the market is large enough for all participants to make a meaningful contribution to the “Digital India” vision of the government.”

He further added, “Mastercard has always partnered with fintechs to further digital commerce and bring innovative solutions to the market – going forward, this will only increase. Our recent collaboration with PineLabs and Zoho, and investment in Signzy is a testament to our commitment to develop solutions that will drive digital acceptance at the grass roots. Our flagship Team Cashless India campaign has a goal to equip 1 Cr merchants in India with digital payments acceptance capabilities making India the largest acceptance market in the world.”

The Threat of Credit By UPI Players

There are just two differentiating factors that Mastercard and Visa enjoy today — seamless usability for cross border transactions and the dominance in credit cards. Both these moats are something that national payments body NPCI is looking to breach.

“Credit/overdraft option on UPI will be a game changer for the payments industry. Micro-credit virtual card across UPI network may see a new set of credit availing users emerging in the country,” Deepak Abbot, cofounder of digital gold loans provider Indiagold and former Paytm growth chief, told Inc42.

In October last year, ET reported that NPCI was planning to enable UPI payments in the UAE and Singapore to take first steps in creating a global product payments product.

As for the credit products front, NPCI CEO Dilip Asbe has been quoted saying: Asbe also underlined that the next big opportunity for NPCI could be in credit, “The next big wave in India will be in credit. Credit is a big opportunity for us at NPCI, but we have to see if the regulator feels so.”

While NPCI just builds the basic structure on which more products can be created, it is fintech companies who ultimately build the crowd-pulling products on top. The next big products would be related to credit and insurance, now that payments has been solved.

And with Big Tech players like Google, Amazon and Facebook holding the reins of the UPI market at present along with deep-pocketed giants such as Walmart’s PhonePe and India’s most valuable fintech startup Paytm, it is likely that at least in India, the two card giants — Mastercard and Visa — will soon face a stern challenge for the credit pie.

With inputs from Romita Majumdar and Deepsekhar Choudhury