SUMMARY

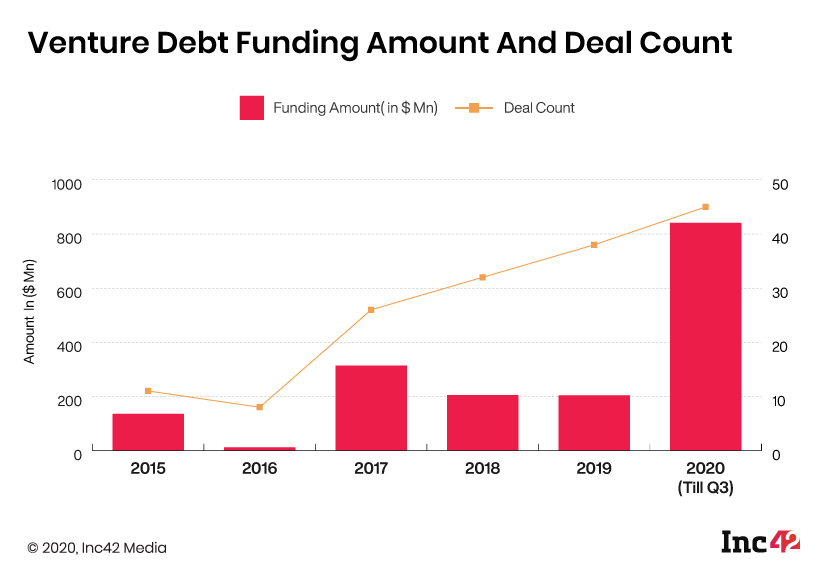

The surge in venture debt funding has been huge — the total corpus of deals in this year, till October, was $841 Mn — already four times the amount of 2019

With the Covid pandemic laying bare the lack of contingency plans, startups have been soliciting venture debt even as VCs either look away or seek lower price points for equity

The lower risk profile of venture debt and double digit returns have caught the attention of HNIs and traditional banks. The question to ask is can startups hold their own as multiple stakeholders take control of their financial resources?

If 90% of Indian startups fail in the first five years, it tells us just as much about the resilience of those that make it beyond this valley of death. But the coronavirus pandemic is no ordinary downturn and a lot of fast growing startups too have had to make tough decisions to live out this unprecedented event, called a black swan moment by one and sundry.

Aswhin Ajila, founder of 15-year-old edtech startup iNurture, was in the middle of months-long negotiations to raise a fresh round of venture capital funding when Covid-19 hit. Suddenly, investors who were forthcoming earlier tightened their purse strings and as was seen in the case of many other deals, the only way to raise funds was with a down valuation.

But Ajila was not going to give in to selling stake for a low price. “We made an informed decision that maybe we should not go for an equity raise. There was no need for us to do a downtrend from the last round or reduce our expectation because of Covid,” the founder said.

With iNurture catering to higher education, there was going to be a serious cash crunch with the academic calendar across the board being pushed back a few months due to lockdowns. The best way to extend its cash runway without selling stake cheaply was to raise venture debt and live to fight the VC battle another day.

Like Ajila and iNurture, startups across stages and sectors have turned to venture debt in the past few months. So what explains this glut?

Why Venture Debt Shone Amid The Covid Gloom

Many startups have taken the debt funding path in the last 6 months — home interiors startup Livspace got INR 30 Cr from Trifecta Capital, music streaming app Gaana raised $51 Mn from Tencent and parent company Times Internet, grocery delivery unicorn Bigbasket raised $3.5 Mn from Trifecta, while cloud kitchen startup Rebel Foods got $4.9 Mn from Alteria Capital.

With venture debt deals accounting for $841 Mn in total funding till October this year, the total amount invested is already four times the venture debt funding for all of 2019.

So why are startups gorging on venture debt?

Since nobody ever envisaged a situation like Covid-19 happening, there wasn’t a lot of contingency planning — which meant the buffer capital that startups required to get through wasn’t in place.

“In this kind of market, when the macroeconomic fundamentals are not very strong, most companies want to feel more secure. So they are keen to access more capital and if they’re not getting the valuation that they seek, the preference is to take some debt as buffer and push out fundraising to the extent possible,“ said Vinod Murali, managing partner at venture debt investor Alteria Capital, which is one of the most active venture debt investors in India.

Make no mistake. It’s not as if venture debt firms have lent money left, right and centre out of benevolence.

A closer look at the funding data shows that these deals picked up from July as startups spent the first few months of the pandemic firefighting the disruptions caused by the lockdowns such as no-touch and supply chain breakdowns.

As a result, the deal flow in April, May and June was quite sparse but then a trend started to emerge.

Apart from the demand from startups, another key factor that has fuelled the venture debt surge is that many B2C companies have seen growing traction and while operations were hampered, the demand remained high. In a short time, many B2C startups had to rebuild capacity even as available workforce was scarce. This led to increased spending in many directions, even though the Covid-19 impact had dented the revenues of these companies as well.

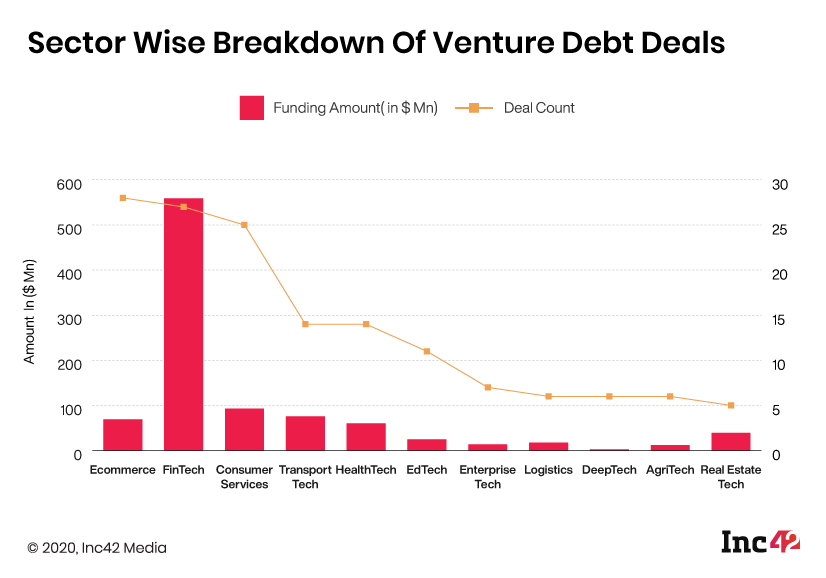

“As we came to Q2, it became clearer that Covid has actually stimulated a greater level of growth and demand in certain sectors such as edtech, healthcare, ecommerce, agritech. It was a leap forward in terms of adoption and conversions,” said Rahul Khanna, managing partner at venture debt firm Trifecta Capital.

Hinging on this optimism, Khanna’s fund made 19 new venture debt investments between April and October, totalling INR 255 Cr. Of these, nine were for new companies whereas the remaining were for the existing portfolio.

Are Startups Getting A Raw Deal?

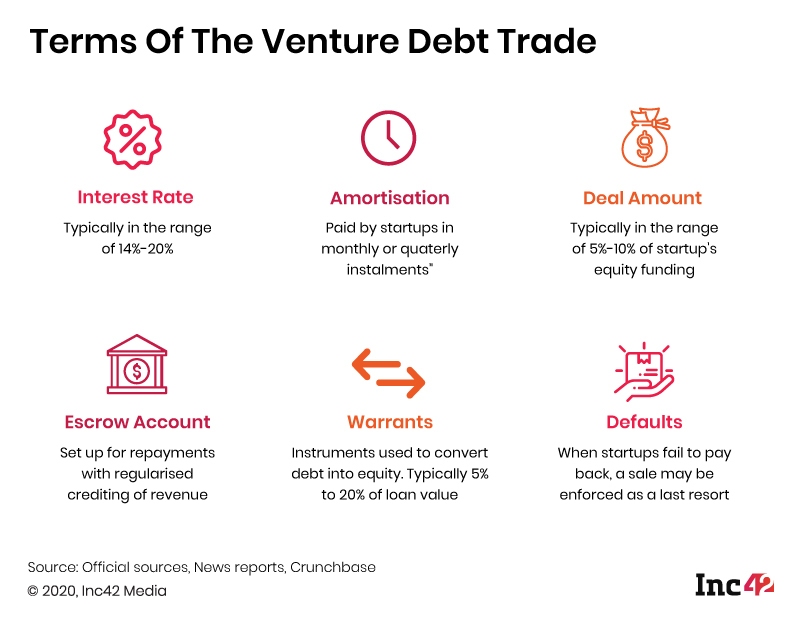

Startups usually prefer to raise multiple venture debt rounds from the same fund as relationships reign supreme in an ecosystem that doesn’t depend on credit bureau scores, unlike traditional bank and NBFC loans. Due to this and the absence of any hard assets as collateral, venture debt is priced anywhere between 14%-20% — a lot higher than the business loans that banks offer.

So, venture debt fund managers seek three things as an alternative guarantee — a consistent stream of revenue which is why most deals are with Series B onwards startups, the presence of adequate equity financing in the form of VC money and a common escrow account where the receivables of the company are collected for a month for servicing the loan. While the repayments may be divided into monthly or quarterly installments, the entire term of the loan is generally in the range of 24-36 months.

“In the case of digital startups, in most cases, there’s no hard asset to give as collateral but a soft asset such as IP of the company,” said Rajesh Sawhney, a seasoned entrepreneur who runs startup accelerator GSF and is the founder of cloud kitchen company InnerChef. Sawhney himself is an angel investor in a slew of startups.

But what use is the IP or the digital platform if the startup itself is a failure?

To hedge against the high risk that is associated with not having collateral, venture debt firms also include a provision in the deal of warrants that can be used to convert a part of the debt — usually in single digit percentage but may go as high as 20% in some cases— into equity during a later VC round.

While startups view the quick realisation period of 1-2 months when cash from venture debt funds start trickling in from the time the discussions start, they may also end up getting a raw deal since the lenders are prone to make take-it-or-leave-it offers as compared to VCs who indulge in long negotiations.

“What happens is that many venture debt funds don’t want to spend too much time on negotiations and legal documentation. Since the product is a lot more commoditised than venture capital, they would not spend too much of overheads on the cost of lending,” said Gerald Manoharan, partner at corporate law firm J Sagar Associates which has a focus in startup deals.

The Dangers Of Debt Turning Sour

Of course, part of the lure of venture debt is the hands-off approach of investors; they rarely interfere with the day-to-day workings of the business and hardly ever seek a board position in the funded startup.

But they still keep the option of pulling the plug on the deals on the basis of business realities through two clauses called material adverse change or MAC and abandonment.

MAC is normally triggered between the date when the term sheet is signed or the investment agreement till the time the cash is disbursed — which could be anything like one of the founders resigning or a severe economic downturn, any situation that an investor thinks affects the viability of the deal.

J Sagar’s Manoharan said, “What happens is that MAC becomes a trigger for enforcement of the debt. So the promoter will say, ‘I understand somebody has left my company, but that doesn’t mean to say the company will shut down, I will still be able to pull it up’. But then the thing is you need to have a defined clause in the contract to pull your trigger somewhere. So that’s where they (venture debt firms) bring it in.”

The second and bigger clause of concern is abandonment — a provision that allows a venture debt firm to back out of the deal midway if it feels that the company won’t have enough equity financing in its bank account to be able to service the debt.

“For instance, a startup may seek venture debt funding to tide over five to six months if it has signed a term sheet with a prospective VC investor and the transaction is taking some time to close on account of diligence. In the meanwhile, if the VC deal goes south that may possibly give the fund the right to ask you to return the money,” the legal expert explained.

But what if the startup’s cash flows have dwindled and it can’t pay back?

The first plan of action in cases of defaults is like any other lender — restructure the debt by extending a period of moratorium till the startup can get back on its feet and begin timely repayments. If it seems that a new round of equity financing can help, a venture debt firm may also use its network to solicit a VC round.

When all of those options are exhausted, the last recourse is to find a buyer. While debtors always have the IBC (insolvency and bankruptcy code) path to fall back on, venture debt firms don’t take that path generally as they like to keep the noise low in such circumstances.

“As a venture debt player, IBC is generally the least preferred resort since business operations come to a standstill & the IBC route would only publicise their default further jeopardising any chance of pivoting the business model or attracting a buyer. In these cases, we would prefer to work with the company and assist them to look for a buyer or a strategic investor that may help them revive their fledgling business” added Ankur Bansal, cofounder and director of venture debt investor BlackSoil, which has invested in the likes of OYO, Purplle, EarlySalary, BTI Payments, Chumbak, Holisol, iNurture, Homelane, Letstransport, Rentomojo, Bajaao amongst others.

Why Startups Flock To Venture Debt Despite Downsides

The primary reason startups seek venture debt rather than traditional loans is because banks ask for hard assets as collateral and guarantees from company directors.

This was one of the key factors for iNurture too. Recapping the decision-making process, Ajila told us, “Personal guarantees cannot be given by the directors as most of the directors on the board of startups are venture equity people. Since we are not an ideal fit for bank loans,we have to rely on venture debt. Most of the banks, whether they’re private or public, have similar requirements which is that you have to give 2X of the loan amount as collateral”.

For other startups, venture debt is a gateway to bigger rounds, especially, if they can prove that they have been able to keep the revenue steady and had regularised returns for their venture debt investors. For online jeweller Melorra, venture debt served to grow its network of venture debt providers and therefore attract VC interest. Plus, it helped in balancing business goals.

Founder Saroja Yeramilli said, “While one is more conservative in their approach and wants to make sure that there is enough cash in the bank, whereas equity players egg you on for greater growth. This helps us to manage our business in a better fashion.”

However, the two main use-cases of debt financing for startups are extending the cash runway before raising the next VC round and preventing the dilution of equity in the company.

“I don’t think we should look at venture debt as a vanilla solution for a bridge round. The bridge round is best when it is done by the existing investors in the company. Venture debt is best when you are taking it for the purpose of enhancing growth by way of plugging in as working capital,” said Ashish Fafadia, chief financial officer of VC firm Blume Ventures.

In Search Of Lost Value

The debate of equity vs venture debt funding ultimately boils down to one factor — the risk and return on capital for investors.

While VC funds promise returns in the range of 30%-40%, in reality their performance has been way lower as the country’s startup ecosystem grapples with the problems of fewer exits and difficult listing norms. This is one of the reasons that high net worth individuals have lately been betting their money on venture debt given its lower risk profile.

“HNIs have allocated capital to alternate assets, including equity investments in startups. Despite the higher risk, such equity investments have fetched average return 15-18%. So the venture debt providers are going out and telling the same investors ‘Why take so much risk, for 15 odd percent average returns when we can get you the same return at lower risk?’”, said Suraj Malik, partner at financial consulting firm BDO India.

Another key reason that has driven HNIs towards venture debt is that central banks in key markets have undertaken huge rate cuts in the last 18 months. This has meant that the return from fixed income assets such as fixed deposits have touched rock bottom and lost attraction even as an avenue to park their money as inflation would erode value.

Since the corpus size of an HNI is large, they’re able to make diversified investments to earn a slightly better return. Moreover, even a quarter or half a percent more of returns makes a significant difference to them as they could be putting in sums ranging from INR 5-10 Cr in a single asset class.

Another attraction for HNIs is that they can know where their money is parked and what exactly they are getting into.

“If you want to go to a mutual fund portfolio there will be 20 issuers and you don’t know which fellow is at risk. This year the Future Group, Zee, DHFL, Vodafone and Essel were at risk. So HNIs today want to know who is it that they are giving money to and if there is a covenant or a contract that will protect them in terms of a downside where at least they have the first right of benefit,” said Santosh Joseph, CEO and founder of wealth management company Germinate Wealth.

While the venture debt firms ensure they have the first right over the startups revenues, and HNIs have locked their eyes on it as a secure avenue of compounding their wealth, the industry is sure to become bigger in the coming days with bigger pools of investible resources.

Moreover, the juicy returns from this asset class is something that has even caught the notice of large scale creditors like public and private banks. Though they won’t still lend to startups directly from their books, they are happy to share the venture debt pie by co-investing small sums.

With venture debt becoming a cherry on top for multiple stakeholders, what remains to be seen is how it affects startups — will it act as a force multiplier for startups or make them pawns in a game that’s not in their interest?