SUMMARY

Most newsmakers either quit their first venture and started out afresh or expanded their cross-border presence

Binny Bansal and Sachin Bansal made news for their dramatic exits from Flipkart; both are launching new ventures now

The extortion puzzle involving Paytm’s Vijay Shekhar Sharma is yet to be solved

This article is part of Inc42’s special year-end series — 2018 In Review — in which we will refresh your memory on the major developments in the Indian startup ecosystem and their impact on various stakeholders — from entrepreneurs to investors. Find more stories from this series here.

“All new news is old news happening to new people.” — Malcolm Muggeridge, English journalist and satirist from the 20th century

We’re taking a slight contrarian point of view here. Sometimes, in fact, often, new news is new news happening to old newsmakers. This is especially true of the Indian startup ecosystem.

Of course, people come and people go — some fading into oblivion and others simply not doing things that are newsworthy anymore — but there are some who endure, whose names hit the headlines ever so often, whose every move is tracked (in fact, even anticipated and preempted) by the media and by others in the ecosystem.

We’re talking about newsmakers among the Indian startup entrepreneurs who are influential, who are at the helm of companies that matter, whose decisions can make or break things — for them and for others.

As we at Inc42 went about our business of covering the latest developments in the Indian startup ecosystem this past year, we observed that the stalwarts of the ecosystem, the old-timers and the influentials, continued to make news — wittingly or unwittingly.

Prime among them were Paytm chief Vijay Shekhar Sharma, who was in the news for both good and bad reasons and Flipkart co-founders Sachin and Binny Bansal, for their exits post the Walmart takeover. Of course, some new movers and shakers were added to the list — for instance, prodigy Ritesh Agarwal, who took OYO international with a vengeance.

New or old, there is one strong trend that defined the year for most of the newsmakers — they either quit their first venture and started out afresh or expanded their presence in the cross-border segment.

Here’s looking at the top seven newsmakers of the Indian startup ecosystem in 2018.

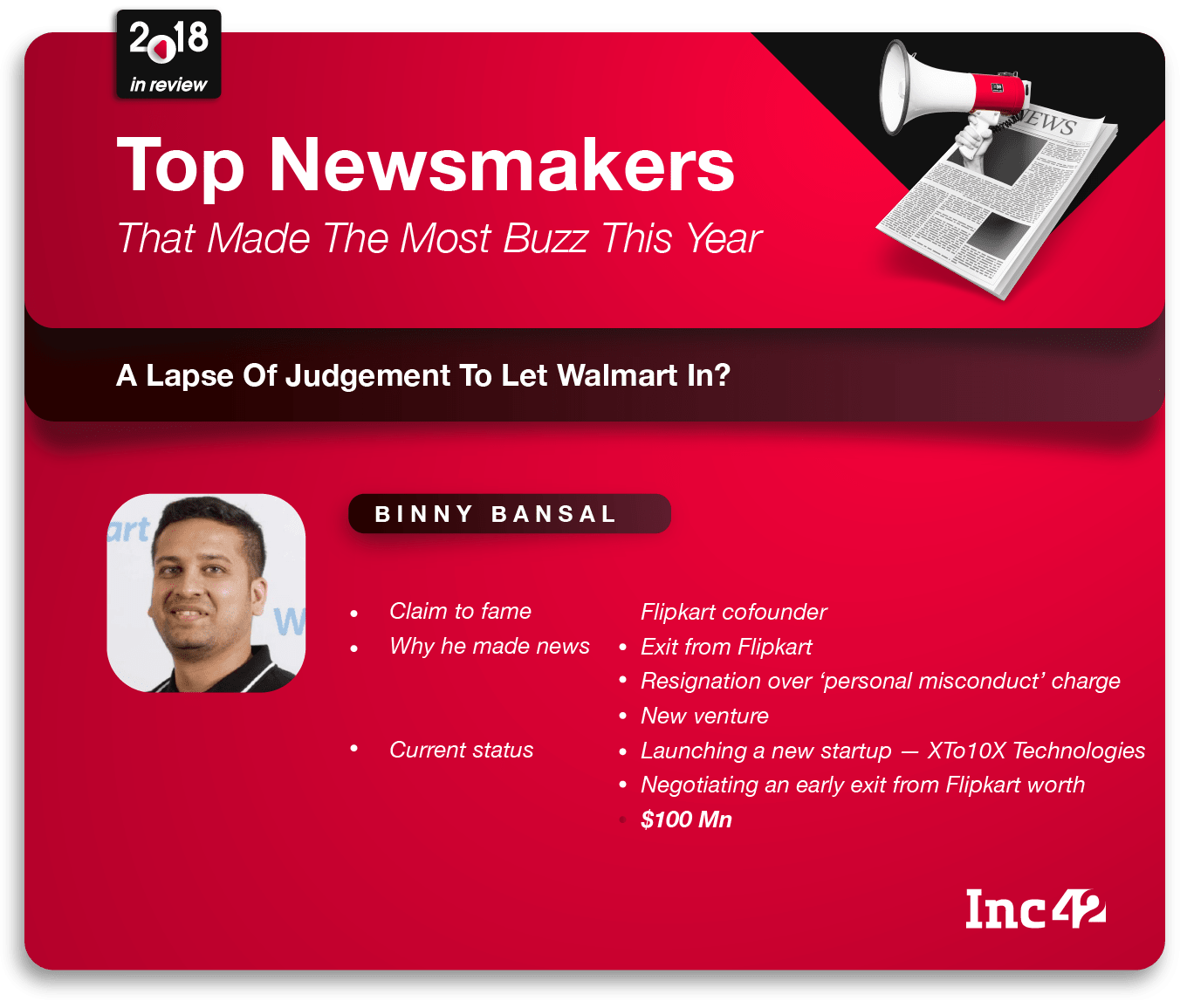

Binny Bansal: A Lapse Of Judgement To Let Walmart In?

Undoubtedly, Binny Bansal was the biggest newsmaker of the year in the Indian startup ecosystem. First came the accolades — US retail giant Walmart bought a 77% stake in India’s biggest ecommerce company, Flipkart, in a landmark $16 Bn deal. Binny also became the chosen one when Walmart decided to keep him on as the Group CEO of Flipkart after the deal while Sachin Bansal was politely asked to move on.

But uneasy rests the crown on cofounders’ heads once their companies are taken over by foreign/bigger companies. Well before the end of the year, Binny was dethroned. On November 13, Binny Bansal resigned from Flipkart under the cloud of a “serious personal misconduct” charge following an internal investigation, according to a statement by Walmart.

Once the shock over the resignation had settled, reports surfaced that the complainant was a woman (a former employee of Flipkart) who had been in a consensual relationship with Binny in 2012. Here are some other claims that emerged:

- The Bengaluru-based woman had complained to Flipkart in 2016 about Binny but the company couldn’t substantiate the charge.

- In July this year, the woman wrote to Walmart CEO Walmart CEO Doug McMillon alleging that Binny had sexually assaulted her in 2016.

- Walmart was irked that Bansal did not disclose the 2016 allegation during the Flipkart acquisition talks. The probe also found that payments had been made to the complainant.

Walmart issued a statement saying that although the investigation did not find any evidence to corroborate the allegations against Binny, it did reveal other “lapses in judgement, particularly a lack of transparency, related to how Binny responded to the situation.” Because of this, the company accepted his decision to resign.

The explanation was hardly satisfying. Flipkart employees and startups watchers viewed Binny’s resignation as Walmart’s tactic to remove the other Bansal.

However, Binny continues to serve on Flipkart’s board. As per latest reports, he is negotiating the terms of his exit and may opt for an immediate cash payout of $100 Mn (INR 701.5 Cr) from his $850 Mn (INR 5,963.47 Cr) worth stake and the rest will be due by August 2020.

You may take his startup away from an entrepreneur, but you can’t keep him away from entrepreneurship too long.

Last heard, Binny was said to be launching a startup called XTo10X Technologies with former McKinsey consultant Saikiran Krishnamurthy. XTo10X will provide technology tools, learning, and consulting services to growth-stage startups looking to scale.

Sachin Bansal: Games Over, Now Back To Business

In hindsight, given Binny Bansal’s unceremonious ouster from Flipkart, his cofounder Sachin Bansal’s exit from the company seems much more dignified and staid. However, at the time it happened, it created a lot of buzz, with the headlines being dominated with Sachin’s name for days and weeks on end.

Sachin saw the writing on the wall (the M&A agreement in this case) during the last stage of the Walmart-Flipkart deal talks at Bentonville, Arkansas, in late April. Walmart wanted only one founder on the board, and they chose Binny over Sachin.

It was reported that three Flipkart board members — Tiger Global’s Fixel, Accel Partners’ Subrata Mitra, and Naspers’ Bob Van Dijk — were against Sachin having a strong operational role post the takeover. The investors felt Sachin Bansal had driven the company to the edge in 2015.

The investors got their way. Shortly after Walmart put out a release announcing the acquisition, Sachin announced his departure from Flipkart in a Facebook post. “Sadly my work here is done and after 10 years, its time to hand over the baton and move on from Flipkart. But I’ll be watching and cheering from the outside,” Sachin wrote.

Adding insult to injury, Walmart excluded Sachin’s name from its official post-deal press release and the photos shared with the media.

Binny’s emotional farewell letter on Flipkart’s blog for Sachin acted as a salve, giving Sachin much-deserved credit for making Flipkart what it became. “A visionary, Sachin was instrumental in making Flipkart a tech-driven company, and ensuring the latest innovations were developed,” Binny wrote.

As they say, all’s well that ends well. Sachin left Flipkart a rich man, having reportedly made around $1 Bn by selling his entire 5.5% stake in the company.

Also, looks like he’s done with playing video games and brushing up his coding skills (as he had said he would do for a while after stepping down). He is back in the game and is looking to invest in startups.

According to reports, Sachin has launched a holding company named BAC Acquisitions along with his new partner Ankit Agarwal, whom he has known from his IIT-Delhi days. His new fund is expected to be to the tune of $700 Mn-$1 Bn and he’s eyeing the fintech and agritech sector.

Reports also said Sachin was planning to invest $50-100 Mn in Bengaluru-based electric vehicle maker Ather Energy and $100 Mn in Bengaluru-based cab aggregator Ola.

Let’s hope Sachin can do unto other founders what he did unto himself with Flipkart!

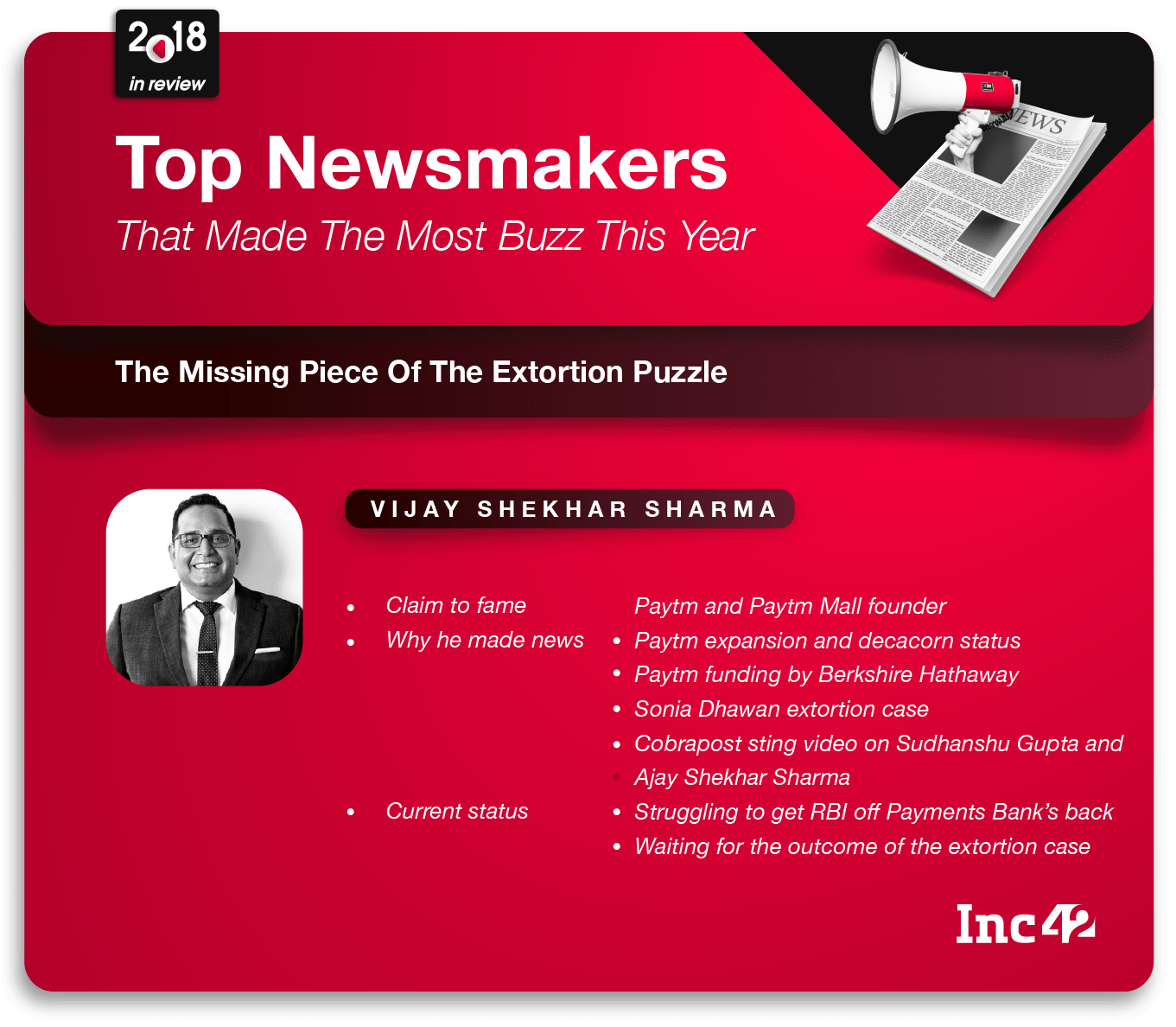

Vijay Shekhar Sharma: The Missing Piece Of The Extortion Puzzle

Vijay Shekhar Sharma, founder and CEO of digital payments company Paytm, has hardly ceased to make news since Prime Minister Narendra Modi’s demonetisation catapulted the fortunes of his company by getting millions of Indians to switch from ‘ATM karo’ to ‘Paytm Karo’.

Through most of the year (2018), the Paytm boss was in the news for his new business moves, expansion activities, and the successes of his companies, apart from a couple of big fiascos.

The good news first: In January, Vijay hit the headlines for leading his unicorn Paytm to become a decacorn with a $10 Bn valuation after a secondary share sale of ESOPs worth $47.2 Mn (INR 300 Cr).

The second-biggest news was its ecommerce subsidiary Paytm Mall becoming a unicorn in April. Paytm Mall secured a $445 Mn funding, with SoftBank investing $400 Mn (INR 2,600 Cr) and Alibaba the rest.

Here is the other news Vijay Shekhar Sharma’s Paytm made this year:

- Launch of wealth management unit Paytm Money

- Warren Buffet’s Berkshire Hathaway’s first Indian investment ($300 Mn or INR 2,178.75 Cr) in One97 Communications

- Japanese JV with SoftBank and Yahoo Japan to launch PayPay, a smartphone-based settlement service based on Paytm’s QR technology

- Launch of Paytm for Business app to enable merchants to sign up quickly and get a Paytm QR code

- RBI bans Paytm Payments Bank from onboarding customers due to breaches including close relations with its promoter group entity (One97 Communications)

However, the going was not all smooth for the Paytm chief. In May, Paytm faced its biggest (then) controversy after Cobrapost released a 13-minute-long sting video showing Sudhanshu Gupta, VP Paytm, and Ajay Shekhar Sharma, Vijay’s brother and a Senior VP at Paytm, allegedly discussing a covert political campaign and saying they had been requested by the Modi government to share user data.

By the end of the year, this was overshadowed by a bigger controversy when Vijay’s former secretary and Paytm vice-president, corporate communications, Sonia Dhawan, allegedly made an extortion bid on the Paytm chief and his family.

A series of twists and turns followed along with many contradictory and confusing developments.

The three accused are still languishing in jail as their bail pleas were rejected. Last heard, Sonia’s lawyer had filed a fresh bail petition in Surajpur district court while Jain filed his petition in the Allahabad High Court. Rohit managed to get a stay on his arrest.

Noida Police recently said that they had a breakthrough in the case, claiming that they had multiple witnesses against the three alleged conspirators.

There are so many missing links that the puzzle still hasn’t be pieced. The big question, however, remains: What is this so-called “personal data” that could have affected the company and its founder if revealed in the public domain?

Hopefully, we will know in 2019.

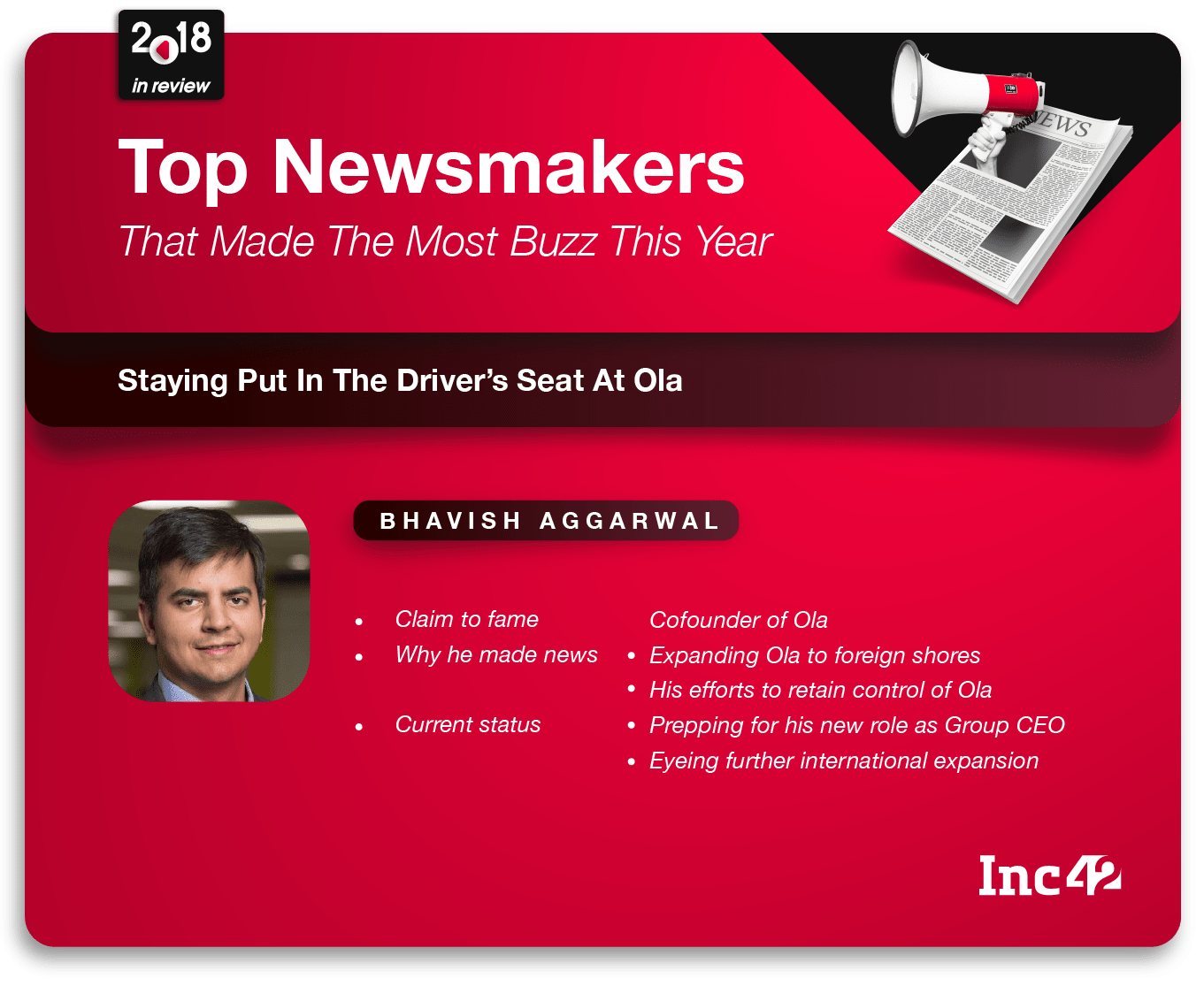

Bhavish Aggarwal: Staying Put In The Driver’s Seat At Ola

Ola cofounder and CEO Bhavish Aggarwal found himself in the news quite often this past year — for everything from raising a billion dollars in funding, expanding to global markets, top leadership rejigs, driver protests, to saving its equity stake from SoftBank.

Ola started 2018 on the right foot, strengthening its strategy to enter foreign markets such as Australia, New Zealand, and the UK — all goals that it achieved as the year went by.

At a time when the Flipkart cofounders were cornered into exiting after the Walmart takeover, Bhavish was in the news most for deploying every trick in the book to hold on strong to Ola. His biggest fight is with Japanese conglomerate SoftBank, which owns 26% in Ola and has been eyeing a greater stake in Ola.

Earlier this year, Bhavish and his cofounder-CTO Ankit Bhati amended Ola’s Articles of Association to secure their rights and restrict the ability of its investors to increase their stake. Any transfer of equity shares by Ola investors representing 10% or more of the company’s capital will need to be approved by the cofounders.

Not one to give up easily, SoftBank is reportedly looking to invest $1 Bn (INR 7036.6 Cr) in Ola’s next funding round. However, Bhavish is trying to keep Softbank at bay and may now look to a new investor to pad up its finances.

In the latest news, the Ola cofounders split the company’s responsibilities, with Bhavish overseeing its international expansion as Ankit leads the charge against Uber in the domestic market. According to reports, Bhavish is expected to become group CEO while Ankit takes up the role of CEO.

Clearly, Bhavish has bigger plans for 2019 and doesn’t want to cede any market share to Uber as he expands Ola abroad.

Ritesh Agarwal: No Reservations About Taking On The World

In the year gone by, Indian startup prodigy Ritesh Agarwal added as many feathers to his cap as his company OYO added rooms to its inventory — 50K a month to be precise. At this pace, OYO, which has 330K rooms across 500 cities and 12,000 franchised hotels at present, will have 2.5 Mn rooms by 2023, surpassing Marriott (exactly what Ritesh is aiming at) with 1.4 Mn rooms.

The 24-year-old founder, who has taken OYO to superlative heights in just five years, achieved every entrepreneur’s dream — entering the unicorn club with an $800 Mn funding — this year. The round, led by SoftBank and with participation from existing investors Lightspeed India Partners, Sequoia Capital, and Greenoaks Capital, valued OYO at $5 Bn. The funds will be used to solidify OYO’s position in India and expand further internationally.

In December, Singapore-based cab-hailing company Grab invested $100 Mn as part of the same round in OYO.

Ritesh has been expanding OYO internationally at a rapid pace since he shifted its business model from hotel aggregation to franchise in 2017 and 2018 was a landmark year in this regard. Let’s take a look back:

- In June, OYO announced its China launch with 11,000 rooms in 26 cities, including Guangzhou, Shenzhen, and Xiamen

- Around the same time, OYO forayed into Jakarta, Indonesia, with three hotels offerings

- In September, Ritesh launched OYO in the UK with four properties and 80 rooms in London

- In October, OYO started testing waters in Japan, offering rooms in 15 properties in and around Tokyo

- Its latest overseas expansion has been in Spain and Portugal

Ritesh also managed to fix OYO’s relationship with online travel aggregator MakeMyTrip Ltd after a two-year breakup, making OYO rooms available on MakeMyTrip and GoIbibo.

When you create so much impact (read disruption) in a market, it is bound to have an equal and opposite reaction. OYO, with its unicorn tag and marquee investors, is now facing the brunt of budget and mid-market hotels across the country, who claim that their businesses are suffering due to deep discounting, high commissions, and arbitrary contract changes by OYO. The company, however, dismissed the allegations as “misguided and misplaced”.

After a blockbuster year, OYO approved the addition of 2,000 stock options to its ESOP, with the aim of “motivating employees and giving them a chance to enjoy the benefits of phenomenal growth the firm foresees.”

Ritesh was also named the ‘youngest self-made entrepreneur’ in the Barclays Hurun India Rich List 2018.

For the future, Ritesh has his eyes trained on consumer needs. “Having your ear close to the ground helps build unparalleled conviction about the severity and scale of the problem you’re solving,” he said at a Lightspeed event.

We’re sure it’s the conviction that has brought the young entrepreneur this far and will take him further in the new year.

Kunal Bahl: The Second Coming Of Snapdeal

Ecommerce startup Snapdeal’s story will go down as an inspiration in the annals of startup history. From a near-death situation to cash-flow positive, Snapdeal cofounders Kunal Bahl and Rohit Bansal have scripted a turnaround story like no other.

While this year-ender special is about Kunal’s reasons for making news this year, here’s the backstory of Snapdeal’s struggle for those not in the know.

2018 has been the second coming of Snapdeal. It all restarted with the launch of Snapdeal 2.0 in August 2017, once the cofounders had warded off a hostile takeover bid engineered by its investors.

“We were going to fall off a cliff if a call was not taken immediately to continue to build the business,” Kunal was cited as saying. They envisioned Snapdeal 2.0 to make a gross profit of $23.3 Mn (INR 150 Cr) in the next 12 months.

Snapdeal 2.0 was a pivot to a pure-play marketplace and a move to divest Snapdeal’s logistics and digital payments non-core assets. It was the sale of FreeCharge to Axis Bank for $60 Mn that brought back lost hope for Snapdeal to revive from the ashes.

And revive it did.

In July this year, Kunal and Rohit shared with their Snapdeal “family” in a letter that the company had become cash-flow positive in June.

In November, Snapdeal was reported to be back on track. In FY18, the company trimmed its losses by 87%, recording a loss of $84.7 Mn (INR 613 Cr) in comparison to $642 Mn (INR 4,647.1 Cr) in FY17, on a consolidated basis.

Kunal even shared the story of Snapdeal’s struggle, and success, in a post on Linkedin that started: “A day doesn’t go by when someone doesn’t ask me this question – ‘So, how are things now at Snapdeal?’”

Apart from pivoting and selling non-core assets, here’s what the Snapdeal team did to affect the turnaround:

- Fixed the economics of the business, and then resumed growing it

- Went back to its roots of catering to the needs of the value conscious buyer

- Improved the experience for its buyers and sellers, keeping the economics in place

- Stabilised the culture and ensured the team was aligned to the company’s plans

- Implemented a time-bound plan to become cash-flow positive and free the company from fundraising cycles

Amid its climb back to profitability, Bahl and Snapdeal was also dragged to the court by its sellers Veepee Electronics and Spacewood Furnishers over alleged non-payment of dues.

Meanwhile, Snapdeal converted the preference shares of all its stakeholders, including SoftBank and Nexus Venture Partners, into equity shares. The move will help attract new investors if the company wants to stick to the private route.

As Kunal wrote in his Linkedin post, “What one needs to muster, right when you are at the bottom of the abyss, is the grit and courage to continue.”

Well, the Snapdeal cofounders mustered that grit and courage. And the results are for all to see.

Kunal Shah: Full Reward Points For Launching Cred

After three years of staying under the radar, serial entrepreneur, Freecharge co-founder, and Delta-4 theorist Kunal Shah made a comeback this year and how. He launched a startup based on the most ingenious of ideas — incentivising paying one’s credit card bills on time.

His new venture, CRED, has taken some time in the making and Shah has let the idea simmer well and proper and ripened it to perfection. Which shows in the resounding reception CRED has received. Shah’s Twitter timeline is full of posts by people thanking CRED for everything from Sleepy Owl gift hampers to paying their phone EMI.

Get paid for paying your credit card bill! Who else could’ve thought about such an idea! Mind blowing, awesome, seamless experience!! Makkhann as they say!! Kudos @kunalb11 and team #Cred ! #killthebill

— Varun Doshi (@Varunrd) December 5, 2018

So why is CRED making all this buzz? Well, the startup, which is in its beta phase, targets consumers with high credit scores and allows users to pay their credit card bills, rewarding them with ‘CRED Coins’, which they can redeem against various products and services. It has partnered with over 30 brands, including UberEats, Sunburn, CureFit, and Ixigo and has about 100 more lined up.

Kunal, who’s very active on Twitter, announced the launch a couple of days before Diwali (November 7) introducing CRED as “a platform to celebrate and reward the most creditworthy people of India.”

Excited to announce Cred, my new startup after 3+ years of playing on the sidelines.

A platform to celebrate and reward the most creditworthy people of India ??

Team working hard to get the beta out in a few weeks.

Happy Diwali everyone. pic.twitter.com/TbQaSO4OFo

— Kunal Shah (@kunalb11) November 5, 2018

Although Shah did a good job of keeping CRED under wraps, he hinted at the comeback with the following tweet in January:

After enriching 2016 with YC, 2017 with Sequoia and perpetual insight hunting, excited to startup again in 2018.

Tinkering with some ideas in healthcare and education.

Onwards and Upwards.

— Kunal Shah (@kunalb11) January 24, 2018

He also uses Twitter to promote the startup and as a sounding board to validate his ideas by running polls on credit card usage such as ‘How do you load your digital wallet’ and ‘Did you ever get an incentive or benefit for paying your Credit Card bills on time?’

In June, reports surfaced that Shah had secured a $30 Mn funding from Sequoia Capital and multiple foreign investors for his new venture. Sequoia and Ru-Net had also invested in Shah’s earlier venture, FreeCharge. Shah, who has a strong bond with Sequoia, which he leveraged again this time around.

Shah has been a serial entrepreneur with ventures like PaisaBack and the coupon-based app for mobile recharge, FreeCharge, launched in 2010. FreeCharge was bought by Snapdeal for $450 Mn and was later sold to Axis Bank for $60 Mn.

A philosophy graduate, Kunal likes to keep things under the radar and his reclusiveness during launching CRED only had the media hounding him.

“Before implementing an idea, one must make sure that the business will be at least Δe=4 to make it brag-worthy,” Kunal has been famously quoted. Kunal’s Delta-4 theory, if understood correctly, can help businesses across sectors do well.

We’re sure Kunal must have applied his Delta-4 theory to CRED as well, as his new idea is completely brag-worthy!

Other Newsmakers Who Deserve Mention

Some who did not make it to our list of 2018’s newsmakers also deserve mention. Masayoshi Son, the CEO of Softbank, for disrupting the venture capital business in India with his aggressive investments — from Flipkart and Paytm to OYO and PolicyBazaar. Kalyan Krishnamurthy, who was appointed group CEO of Flipkart after Binny Bansal’s resignation, for surviving the Walmart acquisition when the co-founders couldn’t.

Smriti Irani deserves special mention for her premature comments on the Indian government’s bid to regulate digital media, which eventually resulted in her having to step down as the Union minister for information and broadcasting.

On April 3, the I&B ministry issued an amendment to the guidelines for the accreditation of journalists in an attempt to curb fake news. Within 24 hours, the notification was withdrawn following instructions from the Prime Minister’s Office (PMO).

That’s a big win for digital media, and we hope it remains that way. If the media’s voice were to be muffled in the garb of regulation, how would we bring you all these news and developments from various quarters, stories of failure, courage, and success of newsmakers such as the ones above?

As we make a new start in the new year, we promise to keep bringing you all that’s newsworthy from this year’s newsmakers and others. And we wish greater success to the Indian startup ecosystem!