SUMMARY

India expected to be home to 100 Mn fantasy sports users by the end of 2020 with the likes of Dream11, MPL, HalaPlay leading the charge

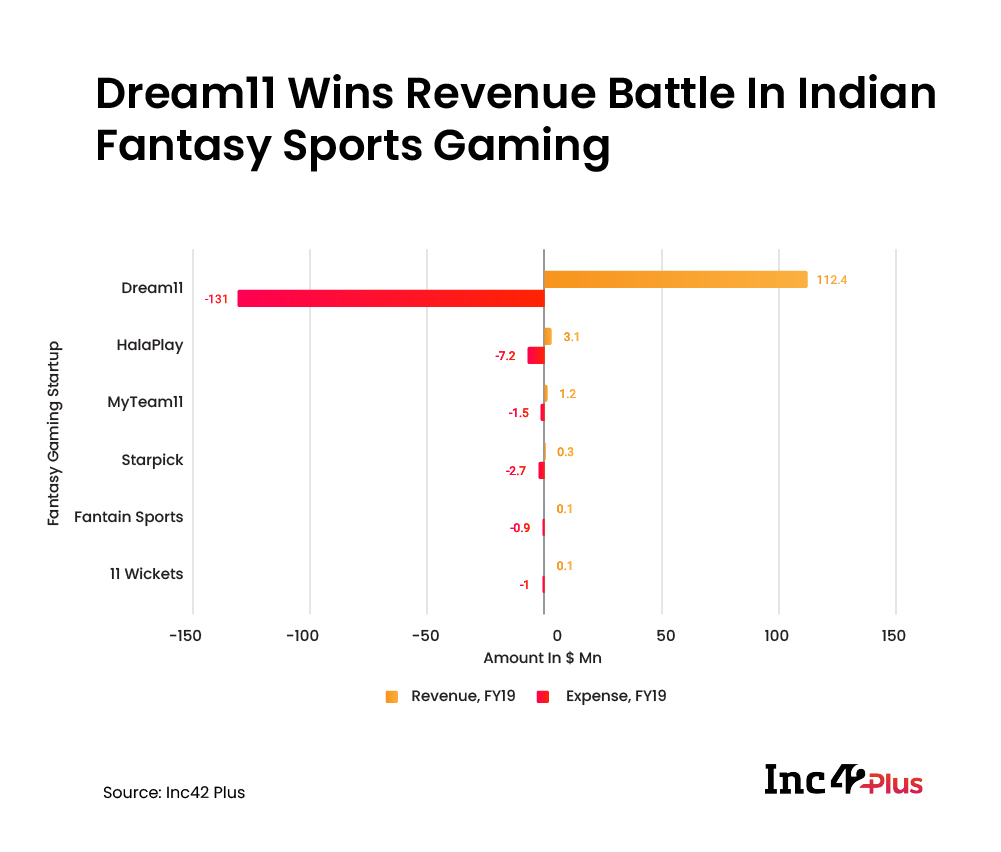

Dream11 led in terms of revenue generation with INR 801.7 Cr ($112.4 Mn) in FY19, but it did not achieve profitability due to high advertising spends

India’s fantasy gaming market is expected to grow at a CAGR of 28%, reaching a market size of $1.6 Bn by 2022

With the 2020 Indian Premier League breaking its viewership records with a 28% increase in viewership as compared to IPL 2019 according to BARC Nielsen, it is a clear indication that given the pandemic, live events are able to engage audiences in novel ways. Similar fan activity and engagement was witnessed on the fantasy sports games during IPL 2020. With the tournament being sponsored by Dream11, the attention was squarely on the fantasy sports market.

Thanks to this, Dream11 experienced a surge of 44.4% traffic volume as compared to the IPL 2019 final and achieved 5.3 Mn+ concurrent users during IPL 2020. With the fantasy games market on the rise in India, will Dream11 continue to set the pace or are there other platforms capable of stealing the limelight?

Fantasy Gaming Landscape In India

Fantasy sports gaming is considered a game of skill as per Indian law. Players create a virtual team by selecting actual players from upcoming real-world matches in cricket, football, basketball, kabaddi and more. Since points are earned based on real-world performance of the athlete, some level of skill is required to master the game, despite some element of luck or chance involved as well. As per Indian law, the key distinction is that one cannot win these games based on random chance or luck, which is why they are considered games of skill.

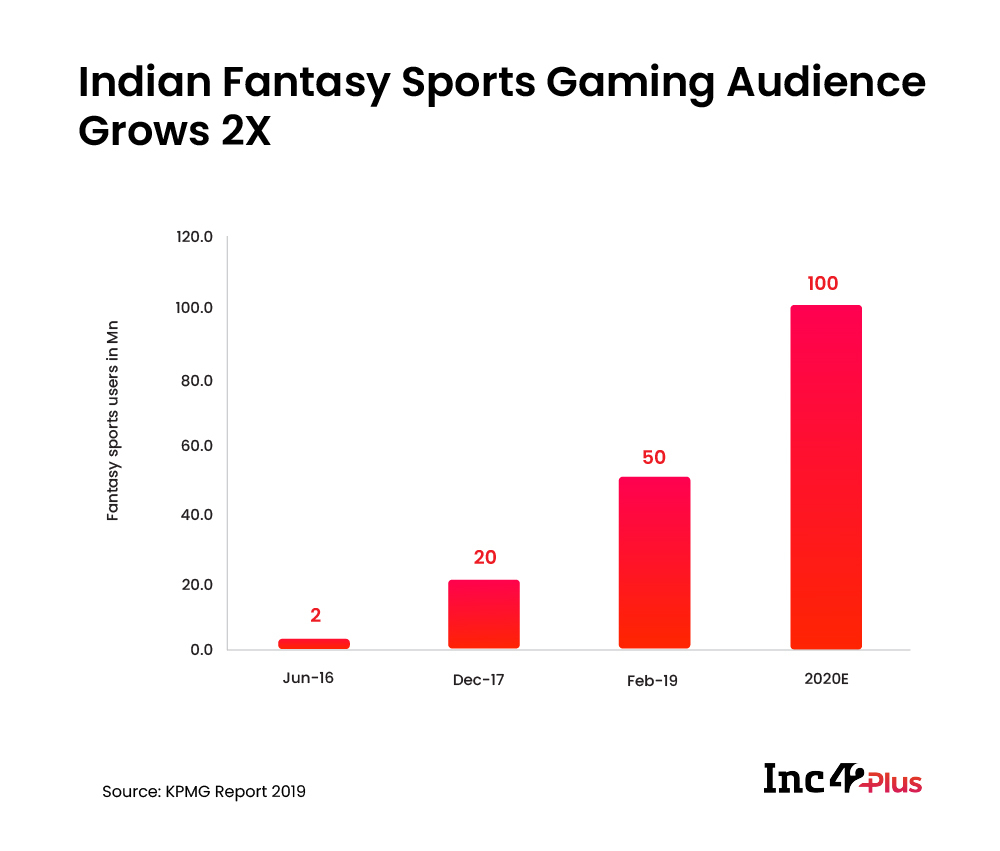

According to a KPMG report, there has been a rise of CAGR 165.9% during 2016-2020 in the fantasy sports user base in India, growing from 2 Mn in June 2016 to 100 Mn (estimated) in 2020. The major factors driving the market include the emergence of various sports leagues that have garnered interest from casual viewers, the increasing adoption for mobile games, the chance to earn extra income as well as the marketing campaigns by fantasy sports startups fuelled by investor backing.

The number of fantasy game startups has increased from 10 in 2016 to 70 in 2018, thanks to the capital inflow and backing for early-stage startups.

Nearly all fantasy sports gaming startups in India are based on the freemium model. Users can participate in free-to-join practice or casual contests, or pay to enter contests that entail cash rewards.

Competitive Scenario In Fantasy Gaming In India

The fantasy gaming market in India these days is dominated by Dream11, with Nazara-backed HalaPlay, Mobile Premier League (MPL), 11 Wickets, MyTeam11, Fantain Sports and Starpick also seeing some share of the limelight.

Who Is Winning The Fantasy Sports Revenue Battle?

Mumbai-based Dream11 is the market leader when it comes to revenue from fantasy sports games. It reported total income of INR 801.7 Cr ($112.4 Mn) in FY19, which is 251.9% higher than the INR 227.8 Cr ($33.3 Mn) revenue it earned in FY18. The company became India’s first gaming unicorn in April 2019 when it raised over $60 Mn from Steadview Capital.

However, it is yet to turn profitable (as per last disclosed financials), since it had a total expense of INR 934.8 Cr ($131 Mn) in FY19. A whopping 84% of the total expenses (INR 785.1 Cr) were for advertising and promotion, which means the company has to spend as much to acquire users than it earns from them, with other major costs also coming into play. Employee benefit expense also grew by 150.4% from the previous fiscal year, reaching INR 66.4 Cr.

Nazara-owned HalaPlay, founded in 2017 by Swapnil Saurav, Prateek Anand, Ananya Singhal and Aman Kesari, also saw a big revenue jump in FY19. Its user base grew by 1700% from 2017 to 2019 from 500K to 9 Mn, while it saw 741.9% growth in revenue, reaching $3.1 Mn from $0.4 Mn in the previous fiscal year.

Jaipur-based fantasy gaming startup MyTeam11 incurred the least loss of INR 2.1 Cr ($0.3 Mn) among all the fantasy gaming startups we compared in fiscal year 2019. The company reported revenue of INR 8.5 Cr ($1.2 Mn) in FY19 with total expense of INR 10.6 Cr ($1.5 Mn) in FY19.

Is Fantasy Sports Gaming Profitable In India?

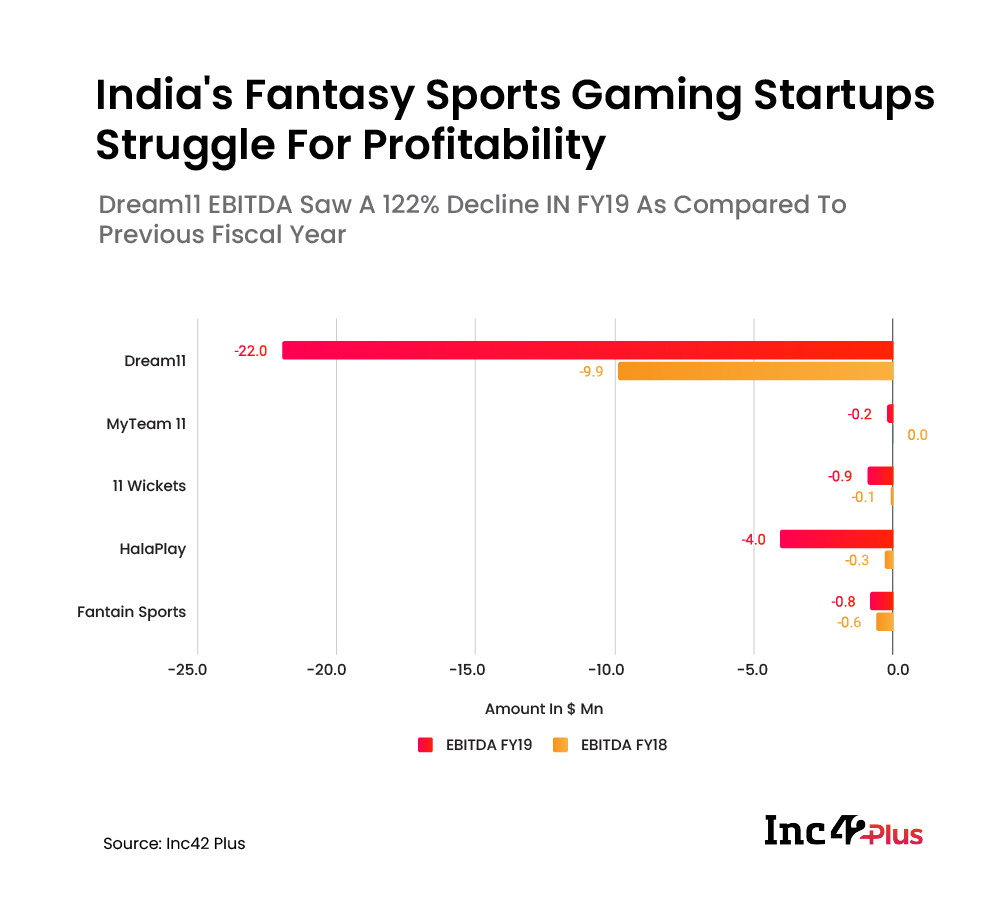

Despite the rocket growth seen for revenue and users, fantasy sports gaming is still a niche category in India. Companies are finding it difficult to gain operating profitability and have had to spend a lot to reach and acquire users. Growing the user base and driving engagement is key to widening the funnel choke-point and converting high-quality users into paying users. The cash burn of the past couple of years has kept startups from becoming EBITDA positive.

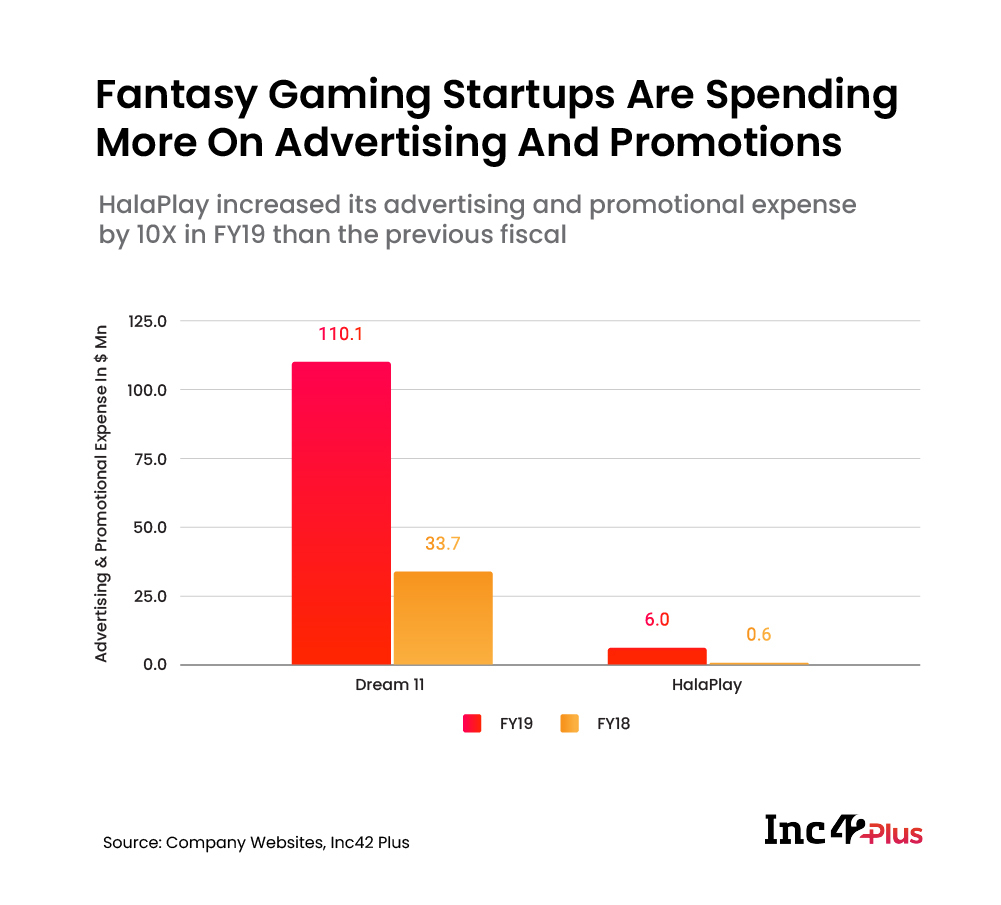

Dream11 went aggressive with the advertising and branding last year. Its advertising and promotional expenses grew by 3.4X, from INR 230.3 Cr in FY18 to INR 785.1 Cr in FY19. The company roped in MS Dhoni as its brand ambassador in March 2018 and launched an elaborate campaign around the former Indian national team captain.

Dream11 went aggressive with the advertising and branding last year. Its advertising and promotional expenses grew by 3.4X, from INR 230.3 Cr in FY18 to INR 785.1 Cr in FY19. The company roped in MS Dhoni as its brand ambassador in March 2018 and launched an elaborate campaign around the former Indian national team captain.

HalaPlay also increased its advertising and promotional expense by 10X in FY19 compared to 2018 and launched campaigns featuring cricketers, similar to the competition.

In 2019, gaming startup MPL roped in Indian national team captain Virat Kohli as its ambassador, an association that was renewed in early 2020. MPL is one of the pacesetters in the gaming arena and also operates other games besides fantasy sports games.

Fuelled by these massive endorsements to expand reach, India’s fantasy gaming market is expected to grow at a CAGR of 28%, reaching $1.2 Bn by 2022.

This makes India the next hot spot for fantasy sports enthusiasts and companies, backed by growing interest around international sporting events as well as domestic leagues. However, in recent months, there has been some negative spotlight on the sector as some political leaders and entities have called for an examination of the business models of these startups in an effort to understand whether there is any component of gambling involved.

The big test for India’s fantasy sports gaming startups will be tackling any possible regulatory overhaul of the market, along with the search for sustainability in terms of revenue generation. As startups and the audience base mature, new revenue models are likely to emerge to expand the India fantasy sports gaming opportunity.

Know more about the rising popularity of India fantasy sports in the latest release from Inc42 Plus —Mobile Gaming In India: Market Opportunity Report, 2020