SUMMARY

With New RBI Guidelines, P2P Lending Platforms Can Register As An NBFC

The Reserve Bank of India (RBI) has finalised norms for peer to peer (P2P) lending platforms. Reportedly, the final guidelines are likely to be released in two to three weeks.

As stated by a Finance Ministry official to PTI, “We have given our comments to the RBI. The guidelines should be out soon. The norms will be out before July-end.” RBI had floated the consultation paper for P2P lending platforms in India in April 2016.

Furthermore, the Finance Ministry has also proposed to register these institutions as Non-Banking Financial Companies (NBFC). Post registering as NBFC, these portals will come under the purview of RBI regulations.

As stated in the consultation paper, “RBI has powers to regulate entities which are in the form of companies or cooperative societies. However, if the P2P platforms are run by individuals, proprietorship, partnership or Limited Liability Partnerships, it would not fall under the purview of RBI. Hence, it is essential that P2P platforms adopt a company structure. The notification can, therefore, specify that no entity other than a company can undertake this activity. This will render such services provided under any other organisational structure illegal. Alternatively, the other forms of structure may be regulated by the State Governments.”

P2P Lending: Definition And Global Regulations

P2P lending can be defined as a use of an online platform matches lenders with borrowers, to provide unsecured loans, as per definition stated in the consultation paper. The interest rate may be set by the platform or by mutual agreement between the borrower and the lender. The platform provides the service of collecting loan repayments and doing a preliminary assessment on the borrower’s creditworthiness. The fees go towards the cost of these services as well as the general business costs.

As per an October 2016 report released by accountancy firm KPMG and the Cambridge Centre for Alternative Finance, the global P2P lending market is worth $130 Bn. In 2015, the cumulative lending through P2P platforms globally, at the end of Q4 of 2015, reached 4.4 Bn GBP, according to data released by Peer-to-Peer Finance Association (P2PFA).

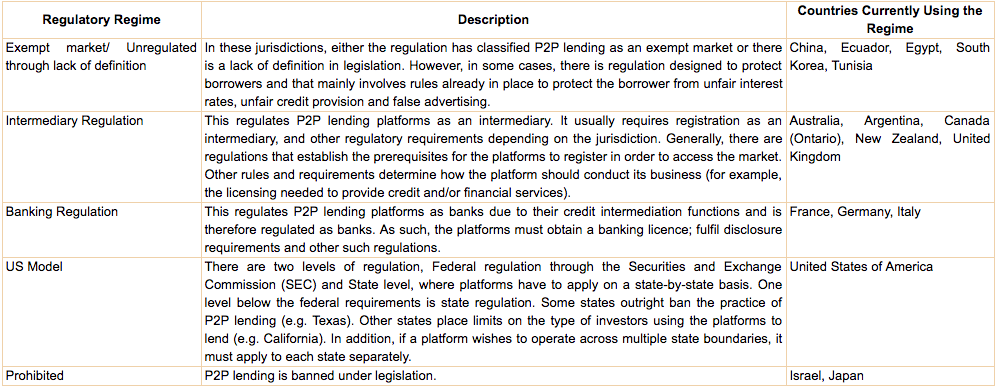

The consultation paper released by RBI mentioned five ways in which P2P lending has been regularised globally:

P2P Lending In India: The Proposed RBI Guidelines

As per the proposed guidelines, the regulatory framework would majorly encompass the following regulations:

- Permitted Activity: The platform could be registered only as an intermediary and will be prohibited from giving any assured return either directly or indirectly. It will be allowed to opine on the suitability of a lender and creditworthiness of a borrower and will prohibit the platforms being used for any cross-border transaction.

- Prudential Requirements: Prudential requirements will include a minimum capital of INR 2 Cr, with a prescribed leverage ratio and prudential limits on maximum contribution by a lender to a borrower/segment of activity.

- Governance Requirements: This includes a set criterion for promoters, directors, and the CEO, with preference to a financial sector background. Also, the guidelines may also require the P2P lender to have a brick and mortar place of business in India.

- Business Continuity Plan (BCP): The platforms need to put in place adequate risk management systems for smooth operations. A BCP and backup for the data needs to be put in place since the platform also acts as a custodian of the agreements/cheques etc.

- Customer Interface: Confidentiality of customer data and data security would be the responsibility of the platform. P2P lending platforms may be prohibited from promising or suggesting a promise of extraordinary returns. Also, the current regulations applicable to other NBFCs will be made applicable to the P2P platforms in regard to recovery practice.

- Reporting Requirements: Platforms will need to submit regular reports on their financial position, loans arranged each quarter, complaints etc. to the Reserve Bank. The bank may come out with a detailed reporting requirement.

Recent facts revealed that, by the end of 2016, an estimated $4.5 Bn worth of loans were disbursed through online P2P lending platforms in India. The launch of India’s digital stack – Aadhar, eKYC and digital payments– is further paving the way for the shift to a cashless economy. Also, the way the Indian government is pushing SME/MSME policies, online P2P lending will open new doors of opportunities for them.

P2P lending startups currently active in India are Faircent, LendBox, Capital Float, Indifi, IndiaMoneyMart, Monexo, Rupaiya Exchange, Capzest and more. While many countries like China, Australia, Germany, New Zealand, etc., have already regularised their P2P lending norms, how well the proposed RBI guidelines will level the playing field in India will be worth watching.

(The development was reported by The Hindu)