SUMMARY

A group representing the crypto industry will submit recommendations for regulations to the finance and law ministries by December end

The core issue will be about suggesting changes to the Foreign Exchange Management Act, 1999, as well as the rules laid down by SEBI

Governments have long been suspicious of cryptocurrency, owing to its use for terror financing and money laundering

India's Crypto Economy

India's Crypto Economy is a brand-new weekly newsletter (delivered every Thursday) from Inc42 to help you decode the rapidly growing crypto economy and its implications on business, work and life. We launched this newsletter on the 4th anniversary of our weekly series “Crypto This Week” which completed 190 editions in May, 2021.

Indian law firm Khaitan and Company, along with Crebaco Global, a credit rating and audit firm for blockchain and cryptocurrency, will submit a representation to the Indian government, urging it to bring in concrete regulations for the cryptocurrency and blockchain industry.

The representation will be submitted to the finance and law ministries of the government by the last week of December, Rashmi Deshpande, partner at Khaitan and Co, told Inc42.

Some of the central points in the representation will be about suggesting changes to the Foreign Exchange Management Act, 1999, as well as the rules laid down by the Securities and Exchange Board of India (SEBI) to regulate the flow of money and the option of raising capital.

“Similarly, amendments in the Income Tax and GST laws would provide clarity on the applicability of tax and finally, the Indian Penal Code (IPC) along with IT laws would recognise specific acts as offences in order to impose penalties,” Deshpande added.

In October, Indian crypto exchange BuyUCoin, in its document titled, Regulatory Sandbox: The Key To Cryptocurrency Mass Adoption In India, had talked about the importance of bringing crypto earnings under the purview of tax. The document said that this would enable the government to gain from Indian users’ participation in crypto, as well as allow investigating authorities to keep a check on those who might be using crypto for the wrong purposes.

More details about Khaitan and Company’s representation to the government will be disclosed in this column when the information is provided to Inc42.

Deshpande pointed out that lack of regulations and the resultant uncertainty is like a death knell for any industry. This is more pronounced for Indian crypto players since the technology underlying their business has several nefarious use cases which need to be kept in check through proper regulation.

Governments have long been suspicious of cryptocurrency, owing to its proven use for terror financing, findings backed by the Financial Action Task Force, an intergovernmental organisation that develops policies to combat money laundering.

While this is often cited as a sufficient reason to ban crypto, FATF representatives are also known to have said that pushing emergent technologies towards a policy vacuum leads to more nefarious use cases.

“Billions of dollars invested in a sector where there are no regulations have the ability to vanish in a few days if the state decides to ban the business. However, if the laws are very much in place, the business is recognised by the government and a sudden banishment is out of the question,” added Khaitan’s Deshpande.

It is worth noting that speculation about the Indian government planning a ban on cryptocurrencies have been doing the rounds since September this year, even after the Supreme Court, in March, had set aside the banking ban on cryptocurrencies in India. However, founders of various Indian crypto exchanges such as WazirX, CoinDCX and Giottus Cryptocurrency Exchange have expressed optimism about the government keeping the industry’s views in mind and coming up with positive regulation for crypto in India.

Further, foreign-based crypto players such as Cashaa are looking to aggressively tap into the Indian crypto market, giving an indication of the buoyant market sentiment for crypto in the country currently.

“As an industry stakeholder, we are constantly in touch with the RBI (Reserve Bank of India), the Indian government, and other crypto entities which exist in the market. Hence, we feel that the Indian government is unlikely to take any decision in haste. The news doing the rounds is mostly speculative,” Kumar Gaurav, founder and CEO of Cashaa, told Inc42.

Industry experts feel that the lack of regulation for cryptocurrencies in India means that there’s a sufficient grey area for fraudsters to operate, leading to a host of crypto scams, which make use of fake wallets, coins to ponzi schemes.

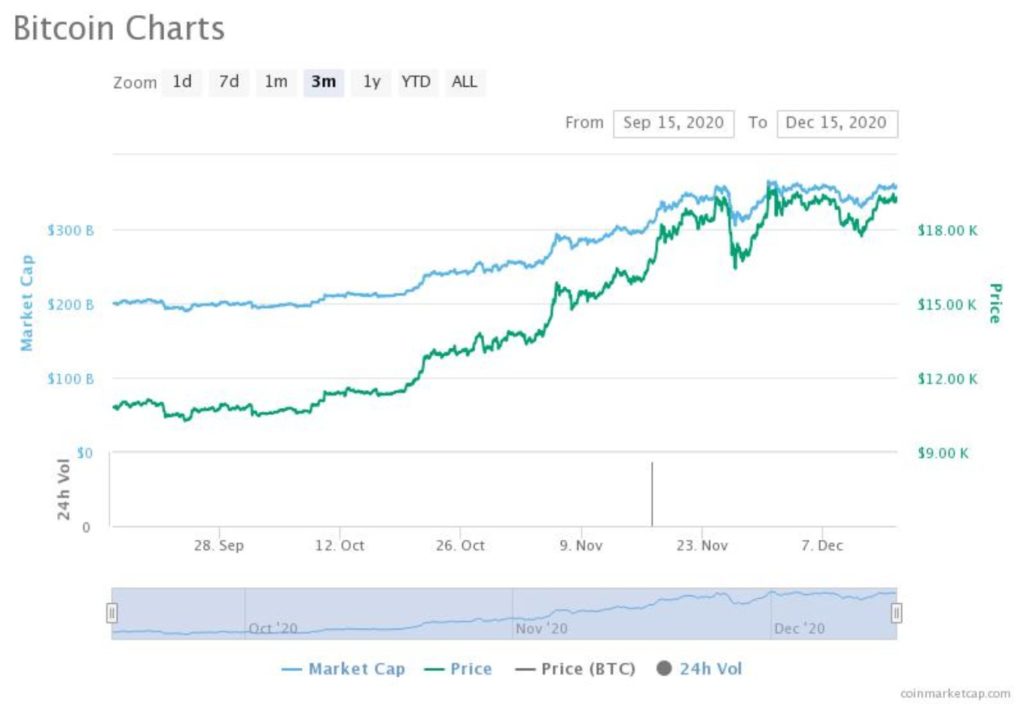

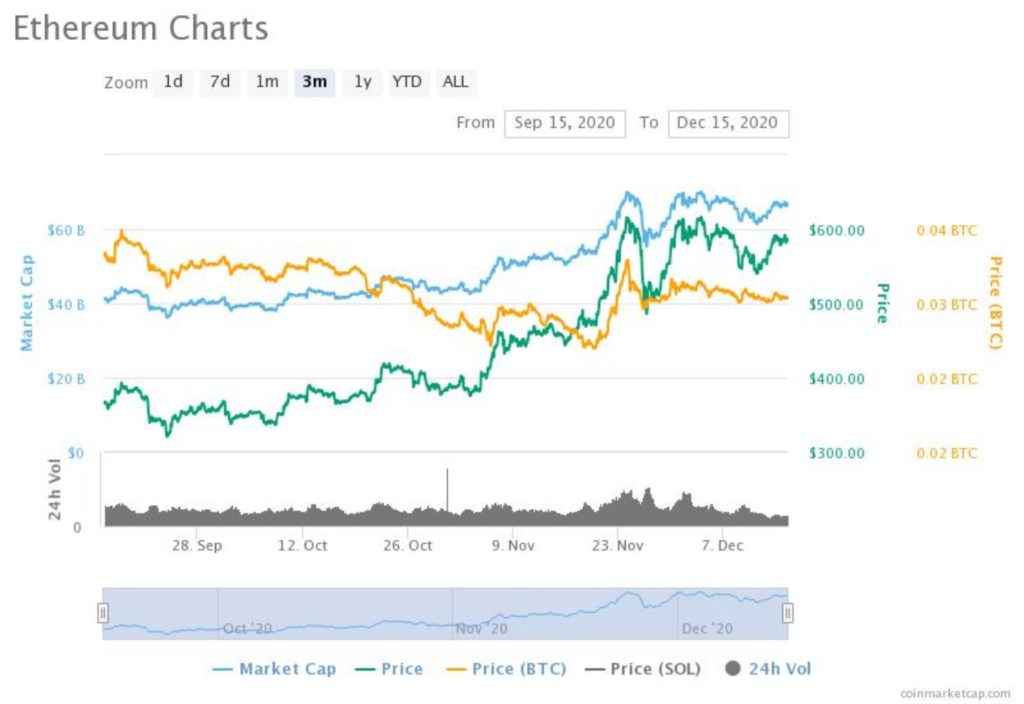

Prices

At the time of writing, Bitcoin was trading at $19,302, a 2.23% increase from last week’s price of $18,880. Its market cap was around $358 Bn.

Ethereum was trading at $585, a 1.73% increase from last week’s price of $575. Its market cap was around $66 Bn.

Other News

From Fake Coins To Ponzi Schemes: India’s Crypto Scams Once Again In The Limelight

With the recent case of a Gujarat cryptocurrency trader arrested in connection to a money-laundering probe related to an online betting racket, we look at the most notable crypto scams to have emerged out of India in the last few years. Read the full story here.

Rich Dad Poor Dad Author Explains Why Bitcoin Will See $50,000 Next Year

The price of Bitcoin is heading to $50,000 in 2021, according to the best-selling author of Rich Dad Poor Dad, Robert Kiyosaki. Kiyosaki pointed out that a “wall of institutional money” is coming to Bitcoin in 2021, which could push the price up further. You can read the full Cointelegraph story here.