SUMMARY

A Deep Dive Into The Hyperlocal FoodTech Market In India

When industry veterans in the year 2015 debated on whether ‘hyperlocal’ will be able to replace ‘ecommerce’ in India, one segment that grabbed maximum investor attention was the FoodTech. The reasons were simple – touted to reach $78 Bn by 2018, growing at 16% YoY, it was creating high demand, looked promising for higher returns and obviously showed an option for a profitable exit.

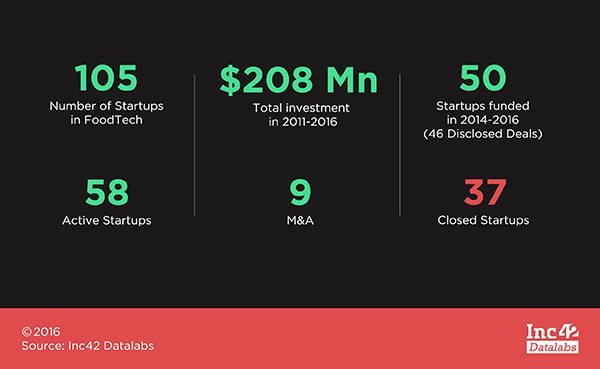

But, as they say – all that shines is not glitter. Soon, the sector became overflowed with ‘me-too’ startups lacking both – differentiation and innovation. The results were obvious. To date, out of the 105 FoodTech startups launched in India, only 58 are active. In past few months, there has been over 37 shutdowns while 9 went off the picture consolidation via M&A route.

Where on one side startups like iTiffin, Eazymeals, Zeppery, Zupermeal, Dazo, SpoonJoy, have to shutdown operations, on the other side, Tinyowl and TastyKhana grew well initially but got acquired much earlier than expected. The entry and exit of UK based JustEat was faster than one would order something online. Even among the biggies, Zomato was forced to shed its workforce and roll back international expansions, while Rocket Internet backed Foodpanda has still not found a buyer even with a rock bottom price tag of $10-15 Mn.

So what happened in past one year that slammed this sector, forcing investors to pull their legs up and stop the lavish lunches? Was it the business model execution failure or the timing is not right or it’s the tightening of investor’s purse strings that drowned the companies amidst cash crunch? Let’s have a closer look into the market.

Evolution Of FoodTech Market In India

A few years earlier, the biggest problem was “discovery” of restaurants. People faced problem in figuring out restaurants that were available nearby and how good they were? Companies like Zomato absorbed this pain by building a simple platform to address the problem of the Indian foodies.

Once the discovery problem was sorted, next came the problem of “ordering/booking” on these restaurants. And that’s what food ecommerce companies like JustEat, FoodPanda, TastyKhana tried to solve by working as the aggregator. The next in value chain was reliability in “delivery” and that’s what Swiggy is trying to solve.

So this is how food market has evolved till now: Discovery -> Ecommerce -> Delivery

“If you noticed, none of these companies do anything to the food as such. They are a content platform, ecommerce platform and logistic services serving the food market. Each of these companies has done a great job by delivering great values to the consumer. And with time these companies have gone up the value chain while also taking care of lower set of values. For e.g. FoodPanda answered both discovery and ecommerce needs while Swiggy answered all of – discovery, ecommerce and delivery needs,” said Kumar Setu, Founder, Petoo.

Companies which entered late or couldn’t deliver additional value other than above three have thus failed in recent past.

But none of these have touched the top of the value chain which is “food” itself. “When I say food – it can be companies coming up with non-traditional innovative foods, companies working on extending the life of food, companies working on a vegetarian substitute for egg and chicken and even those who are backward integrated till farms to deliver organic food experience,” added Setu.

The Twisted Model Maze of FoodTech In India

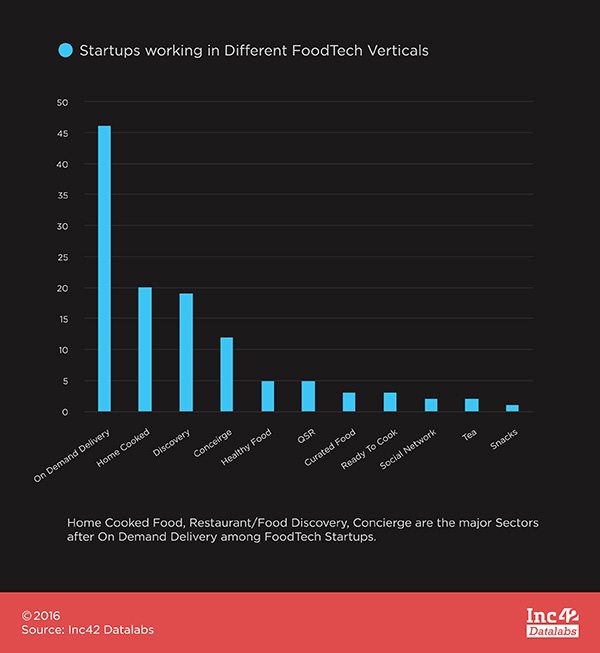

After on-demand delivery, restaurant and food discovery, concierge, home cooked food, and kitchen cloud are the most sought business models in the current FoodTech space.

On-demand delivery is the most crowded segment presently. Within top 25 cities having around 75000 restaurants, the number of daily orders over the phone for food range between 0.7 Mn and 1 Mn. Overall FoodTech startups cater to less than 50,000 orders a day. That’s just 5% of the total daily orders.

Startups working on restaurant/food discovery model initially attracted investors as well as consumers. The model offers upto 80% margins and revenues through ad sales. Zomato is a leading startup in this segment with 5000 restaurants in India advertising on its site.

Later, the startups also experimented with discovery plus concierge model, wherein they provided consumers an app for discovering restaurants and placed their own delivery personnels to pick the order from the restaurant and deliver to the customer. However, only a few have been able to make a mark in this kind of setting. For most business models, deep discounts worked in a short term, but in later stages, only those who focused on leveraging the technology and scaling in a timely manner survived, as in the case of FoodPanda and Swiggy.

Next is the Cloud Kitchen model. Cloud kitchens are basically online breakfast and brunch units that do not have a physical restaurant. Their business model runs around virtual websites/apps via which they take orders. Here the startups such as HolaChef, FreshMenu, Bhukkad own the food and delivery part of the business. This gives better margins but the challenge is to scale up with an army of chefs in various cities.

The one most sought after business model in India after these is home-cooked food model, wherein tackling the quality and complexity issues is really a daunting task. As Rajesh Sawhney, founder, InnerChef and GSF Accelerator says, “Home-cooked-food-delivery is a very tough business. It’s based on this premise that young migrants into big metros crave for home-cooked food. But the math doesn’t add up. People don’t want to pay any premium amounts for home food, but logistics and operational costs are far heavier than the “Kitchen in the cloud” business model that InnerChef follows.”

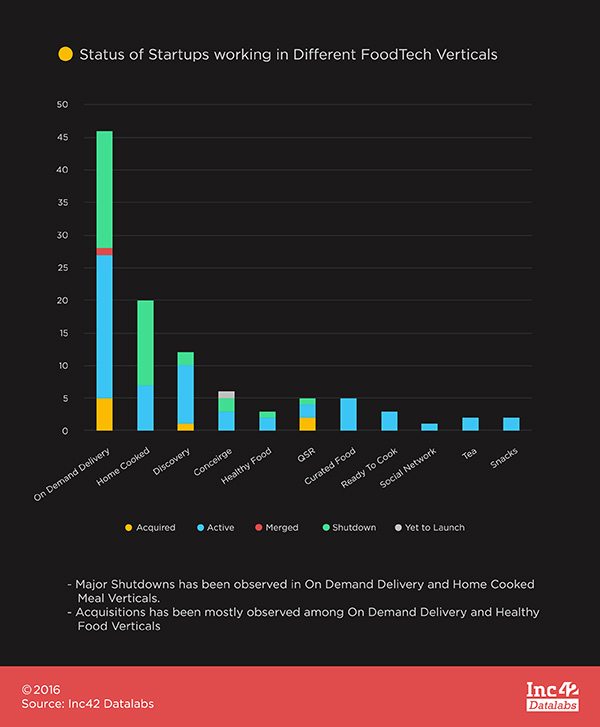

In past few years, 65% of startups in home-cooked food segment either got acquired or were shutdown. Angel Investor, Ajeet Khurana, aptly says, “It’s not enough to merely automate the food ordering experience. One need to put forward some outstanding examples such as in lines of InnerChef (great food), FreshMenu (great menu), and Zomato (strong social presence).”

However, in the opinion of Setu, home cooked food delivery has been a business with huge operational and quality control challenges, which cannot thrive in the long run.

“Imagine how will you put quality check processes in place when food is cooked at multiple homes spread across city and how will you manage the operational challenge of picking up food, packaging it and delivering it to the customer economically while also scaling it up across geographies. The solution itself is too complex to solve a problem. So I don’t think a home-cooked food business can thrive, let alone survive, and they have to transition to central kitchen model or come up with some other innovative solutions to simplify the solution,” said Kumar.

The FY 2015-16 Funding Trends In FoodTech

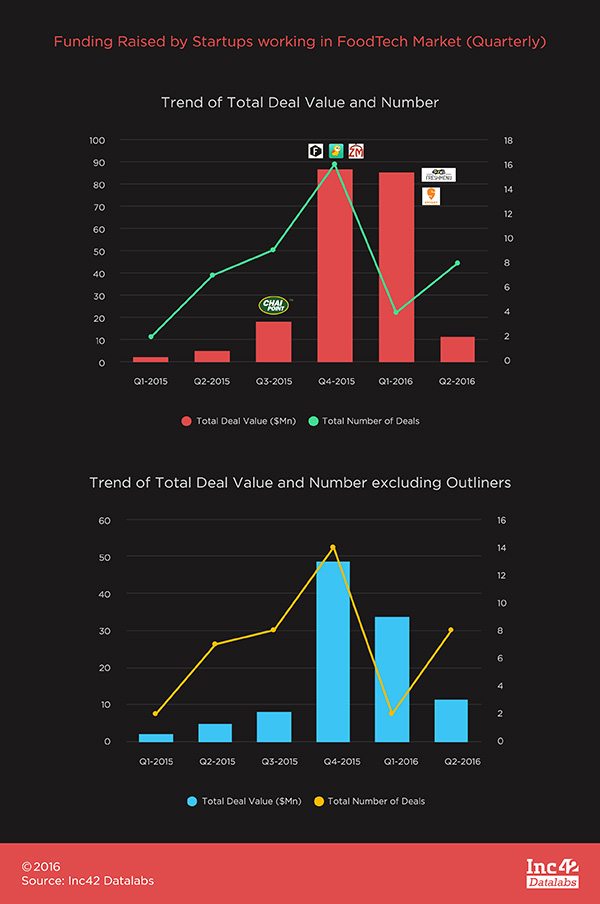

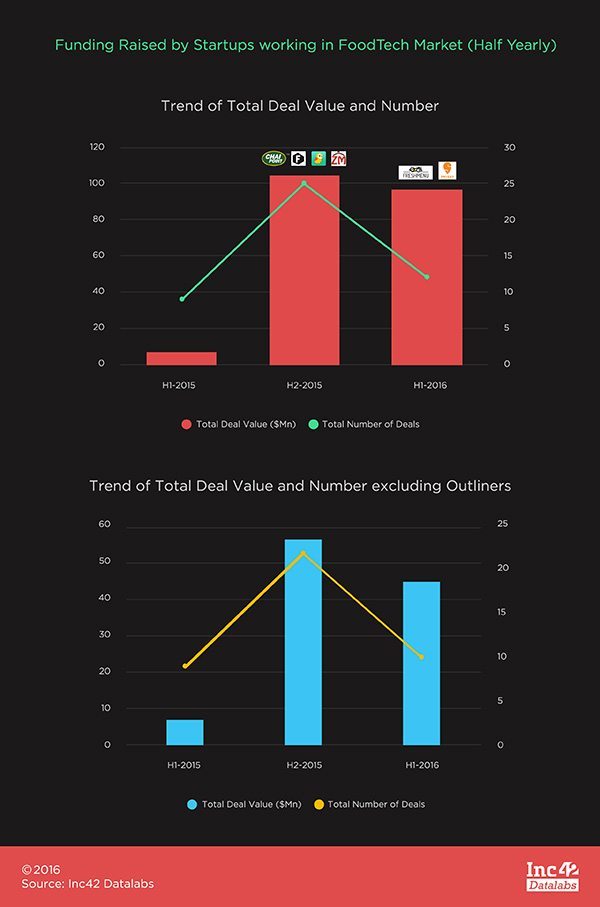

The quarterly funding trends observed a definite drop in total deal value and a total number of deals between Q4 2015 – Q1 2016 (by 31% and 86% respectively).

Where even the early stage startups like Chaipoint, Fassos, TinyOwl, etc. were able to raise funding in the second half of 2015, the current year witnessed major fundings into late stage startups like FreshMenu and Swiggy.

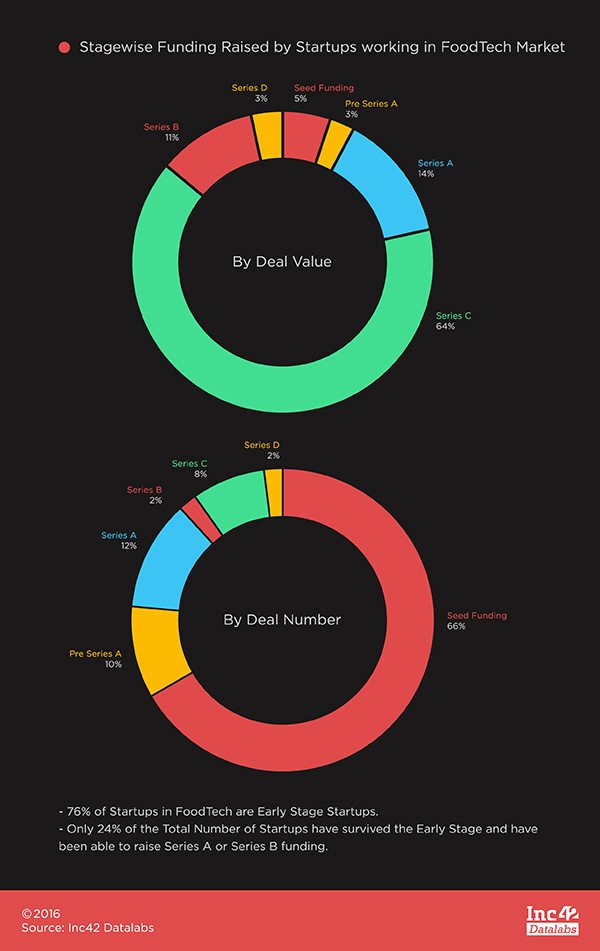

Of the total 105 FoodTech startups, 76% are in early stage. Of these, only 24% survived the early stage and are able to raise Series A and Series B funding.

As interpreted from above analysis, 95% of the total deal value is secured by 24% of late stage deals. Does that mean the market is heading towards Pareto Optimality? “Not actually,” said Krishna Vinjamuri, Principal, Lightbox Ventures. “I think this is a temporary dip in early stage funding. Startups that tailor their offerings around changing customer lifestyle trends will get funded in the future,” Krishna added.

Setu, however, put this forward in a different manner. According to him, if we just talk about the food delivery market, it’s moving towards Pareto Optimality and thus it’s in everyone’s best interest if companies start consolidating in this space letting 1-2 winners emerge out of it. But if we talk about this in the context of funding for FoodTech companies, we are nowhere close to Optimality.

“There are hardly any real FoodTech companies and the worst, there are hardly any investment going into this sector. The time has come for funding to support the growth of real FoodTech companies even if these are not so lean in nature (and hence not liked by the typical investor). There are no more lean businesses which can be created in food market as all the lower value chains have been taken care of by some amazing companies in recent past and time has come to pump the money to grow the businesses in the higher value chain. The time has to come up for the real FoodTech to stand up and investors/media to provide the support it deserves and needs,” added Setu.

Whereas, Sawhney and angel investor, Sanjay Mehta, are neutral on this and believe that capital eventually consolidates towards the players with a long term vision, strong execution and sound unit economics. The food business is no different and it will always be the case where maximum investments are garnered by top few performing startups but there is scope for many to exploit the food space with innovation.

Future Of FoodTech In India

In the first wave of exuberance, there is always a rush of startups. This happened in EdTech, ecommerce, hyperlocal grocery and also in FoodTech. According to Sawhney, the year 2016 is a year of cleansing while 2015 was a party year for startups. Startups that continue in hangover will die, however, the one who change, pivot and adapt will survive this capital squeeze and will eventually emerge stronger in 2017.

Krishna, on the other hand, believes that the current FoodTech market is very large and unorganised. The game is still early and new businesses can be created provided they add value that customers care about. There are multiple business models like full stack, marketplace, etc. that can co-exist and grow into large businesses.

Further, there has been a definite fall in funding for FoodTech startups, and major number of shutdown are happening in the early stage. Ajeet added that, of the entire spectrum from full stack business models (e.g. Box8) to thin layer business models (e.g. Runnr), it’s the thin layer ones that are dying fastest.

Sanjay further explained that one should understand that food technology is not IT but how innovative one is in providing the food experience using real food technology. For e.g how juices were made by cold pressed methods to retain nutrition is true FoodTech & not an app?

But does this suggest that the FoodTech sector is moving towards saturation? It’s a no according to Setu. He believes that funding slow down has nothing to do with saturation as funding can not be a yardstick to measure the potential of a market. But it does affect and slow down the growth of a market for sure.

Unfortunately, shutting down of companies serving lower value chain has affected the fund flow to actual food tech companies trying to address the top of value chain. “And I can just hope and wish that there are enough visionaries in media and investor community who can see through this maze and support the real FoodTech companies who are actually trying to transform the food market. He doesn’t see FoodTech companies shutting down because there are hardly few which are actually FoodTech companies. What we have seen in recent past is – hyperlocal delivery startups (which are nothing but logistic companies operating in food space) or delivery focused food companies (can be called QSR 2.0) with only differentiation being dark stores compared to customer facing outlets – taking a hit.

“It’s unfortunate to label these companies as FoodTech and marking the sector as a failure when the sector has not even taken off and there is a lot that needs to be done in food. It’s like labeling textile market as a failure if one of the ecommerce companies selling clothes shut down. There are a lot of pain areas in food market which can be addressed with the proper use of technology and science. And that’s why I believe food tech hasn’t failed. It’s the media and ecosystem in general which has painted the wrong picture by labeling anything to do with food as food tech,” added Setu.

All in all, the Indian Startup ecosystem is too nascent to make any solid forecasting of its market future. The ecosystem, being flooded with too many Me-too models, has made recognition of disruptive ideas or technologies in food industry difficult. However, the shift in the funding scenario in the market would churn out the flawed businesses and is expected to allow execution and growth of true innovation in the FoodTech industry.

[With inputs from Ankan Das And Pooja Sareen; Graphics by Satya Yadav]