Imagine.

Imagine is a powerful word. ‘Imagine’ helps to foresee the future before anyone else has even thought about it. Imagine helps an entrepreneur question the status quo: What if instead of this, we follow that path? What if instead of doing it this way, we approached it another way?

What if instead of calling a phone recharge a recharge, it is called a deposit in the Airtel account? And what if one could use the technology behind recharges and deploy it for a bank so that a customer could simply walk into a store and make a deposit in his savings bank account just like recharging?

This idea was exactly what Abhishek Sinha and Abhinav Sinha imagined way back in 2006 while running their first company Six DEE Telecom Solutions, a telecom value-added services. Abhishek had started the company in 2002 along with a colleague from Satyam Infotech while Abhinav joined in 2005. Six DEE created value added services products for the mobile and sold it to mobile operators. As India was very competitive at the time, most of the products were being sold in Southeast Asia, Sri Lanka, Middle East, and Bangladesh.

One of the products it sold was the prepaid recharge scratch card. The platform at Six DEE automated the scratch card, eliminating production cost and distribution cost. Since the physical card got eliminated, the amount one could recharge was completely democratised.

It is then that an idea struck the duo: banks could use the same technology as used by the mobile operator for providing banking to retail outlets. At that time, a similar programme was being carried out in Kenya by Vodafone called the M-Pesa where Vodafone-enabled subscribers could send cash to other phone users by SMS. So, basically, one could leverage the booming mobile phone technology and enable payments and financial services by partnering with retailers and mobile phones.

Hence in 2007, they exited Six DEE and spent the next five months absolutely white boarding on what they should do next.

In September 2007, Eko was born.

The Gurugram-based financial services company started providing mobile money services based on USSD, SMS and IVR through its two-factor authentication (2FA) technology. It allowed customers to make secure transactions on their mobile phones, without installing software on the phone or the SIM card. And it provided peer-to-peer money transfers, cash deposits and withdrawal, wage and salary payments, micro-insurance, and micro-credit facilities to individuals through small neighbourhood shops, which became their banking agents.

Eko collaborated with banks and retailers and started to open bank accounts and enabled deposit/withdrawals for customers right at the retail store. When a customer walked in an Eko retail store, he would simply be asked to furnish an address proof, ID proof and an account would be opened for him within 10 minutes. He could conduct withdrawal and deposit transactions out of his mobile phone.

The mobile, in the hands of the customer and the retailer, acted as a point-of-sale device and the whole experience was as simple as getting a talk time recharge.

The mobile, in the hands of the customer and the retailer, acted as a point-of-sale device and the whole experience was as simple as getting a talk time recharge. Since only feature phones existed at the time, Eko leveraged the platform to enable financial transactions.

From A Business Correspondent To An Independent Startup

Being the first startup to start building mobile financial services for the end consumer in India, it faced a unique problem. None of the regulations that exist today were present back then – such as the mobile payment guideline, mobile banking guideline, and UPI among others. So in the beginning, the team completely underestimated the overbearing need to comply with regulations. Says Abhinav,

“As we did not come from a banking background, we did not give a lot of heed to regulations. So the only way for us to participate was to become a business correspondent to the bank. In layman terms it’s nothing but an outsourced bank branch. So becoming a business correspondent allowed us to source and service customers outside the premise of a bank branch.”

From 2008 to 2011, Eko partnered with SBI, Yes Bank, and ICICI along with other banks to function as their business correspondent. But it had to face a unique set of challenges at this time in its journey. While there were regulations in place to do business with business correspondents, banks had no idea how to do business in retail stores.

Secondly, as Eko’s target audience was the lower to medium income customers who were earning between INR 10K-30K in cash monthly; the banks, who were used to big ticket size customers, had no idea how to go about banking in a retail store with this audience.

Thus stemmed the problem of creating a viable financial model where all the stakeholders including the banks, Eko, and the retailers, were able to make enough margins with respect to the capital and time they were to individually put in. Hence even though Eko was growing continuously, it was losing money on every customer it transacted with.

Explains Abhinav, “Initially, it was economically strenuous, and we were not creating any value, in terms of startup perspective. Hence, we were not able to attract a lot of capital. Because, at the end of the day, we were agents to the bank and unless they realised that it was important to create an economic model for all the stakeholders, it was very difficult for us to influence the business model. Hence in our earlier days, we relied on ourselves, family and friends, and the grant from the World Bank because the economic model we were trying to build was not stable.”

Also, since it was not an independent service provider, providing services to banks which were in turn giving their service to end customers, all indirect or direct expenses were borne by Eko. On the flip side, the revenue it earned was shared with the banks.

Gaining Recognition With Remittances

A trigger was needed to change the tide.That came in 2011-2012, when instead of focussing on account opening and deposits, Eko pivoted to conducting transactions around remittances. This was driven by the realisation that the economically active urban customer who wanted to send money back home was ready to pay.

It was at that point that Eko’s customer base started growing at a rapid rate, with thousands of them walking into stores.

Eko’s proposition to its end customer was to start remitting money through Eko rather than going to a post office and sending money orders. Or relying on risky and time-intensive informal networks like friends, families, hawala couriers or bus drivers etc. It’s here that the banks also realised that remittances were a fantastic game as far as economic value was concerned.

And that’s when a business model was created. This led to Eko also attracting its first set of investors in 2011.

But Eko’s struggles to scale still persisted on account of its dependence on the banks. Says Abhinav, “We were dependent on banks; so if we wanted to go to any city, we had to ask permission from the bankers. And if they did not allow, we could not scale to that city.

“ The other problem was we could not charge differently for different geographies. The amount which a guy wants to pay for the service in Delhi varies significantly from what he can pay in another state. And banks do not charge differently for same product in different geographies. So we realised that scalability of the product with the bank was very difficult.”

Pivot Number Two: Eko Wallet

Luckily for Eko, the financial services scenario was gradually changing and by then wallet licenses were out. Hence, it realised it was better for it to become a wallet rather than staying as a business correspondent with the bank. Becoming a wallet meant becoming an independent service provider, which enabled it to charge in whatever manner it wished as it would be a directly regulated entity by RBI.

Hence, Eko applied for its license in 2013 end and received it in March 2015. Finally, in December 2015, it launched its semi-closed prepaid wallet service in partnership with the National Payments Corporation of India (NPCI) and RBL Bank Limited (formerly The Ratnakar Bank Limited). Eko’s current license is valid up till March 2020.

Through the Eko Wallet, users can send deposits or remittances to any bank account in real-time using Immediate Payment Service (IMPS) extended by the NPCI. Through the PPI license and partnership with NPCI, Eko’s own customers can also send real-time remittances to any bank account. Besides, the platform also offers utility bill payments, retail merchant payments, one-click mobile payments and other emerging mobile money capabilities via its apps and point-of-sale presence.

Eko will quickly be moving to integrate with other interfaces extended by the NPCI including AEPS, APBS, BBPS, RuPay, UPI, etc. to leverage the payments infrastructure to its fullest. It is also looking to offer a multitude of new products and services in the payments domain using its wallet license, product assets, and NPCI partnership.

Adding 650k+ Wallets Monthly, Clocking 15 Mn+ Users

For Eko, the real scale up happened once its wallet license came in. It has been more than a year since the waller has been completely operational and traffic volume has more than doubled. In April 2016, Eko touched close to 14.9 to 15 Mn registered customers. Over the last eight years, Eko has transacted over $2.6 Bn(INR 18K Cr) over 10,000 merchant points without a single instance of fraud. About 600K-650K wallets are being added every month. Also, it has entered into partnerships with about 35 partners who help it in acquisitions of stores.

Says Abhinav, “ With the wallet, came the luxury of designing the products that we wanted to, price it in the manner which is right for the customer, customise for geographies, and scale it in any geography we wish to. Today, except for a few states we are present in almost every state in this country and have close to 10,000 Eko stores right now.”

Mostly these stores are local neighbourhood shops in areas with high migrant-worker populations where the shop owners are often trusted members of the community and are able to explain how Eko works to their customers. Consequently, the company has provided a platform to more than 4,000 retail merchants to enable these transactions and provide another source of earning.

Eko is now close to hitting $74 Mn(INR 500 Cr) worth of transactions in a month and in six to eight months, is targetting $150 Mn(INR 1,000 Cr) worth of wallet transactions. Currently, remittances are the biggest revenue generator, with the customer getting charged 1.5%-2% of the transaction value.

In case of recharge or bill payment transactions, if the operator pays Eko a commission, then nothing is charged from the customers. In some cases, where the operator doesn’t pay anything, a minimum customer fee of INR5- INR10 is charged from the customer.

Now that Eko already has a considerable portion of the customer’s wallet share (money being remitted via Eko), it is trying to understand the other transactions in the light of its customers and digitise them as well.

We are trying to create an ecosystem of merchants around the store aspiring to make him start funding his Eko wallet for more than just remittances and utilities.

Explains Abhinav, “In the Eko store, we are already converting his (the user’s) cash to digital money, so our next step is how do we make him start doing transactions such as grocery, fuel purchase, spending on eating out, and miscellaneous daily and monthly needs through the wallet. So we are trying to create an ecosystem of merchants around the store aspiring to make him start funding his Eko wallet for more than just remittances and utilities.”

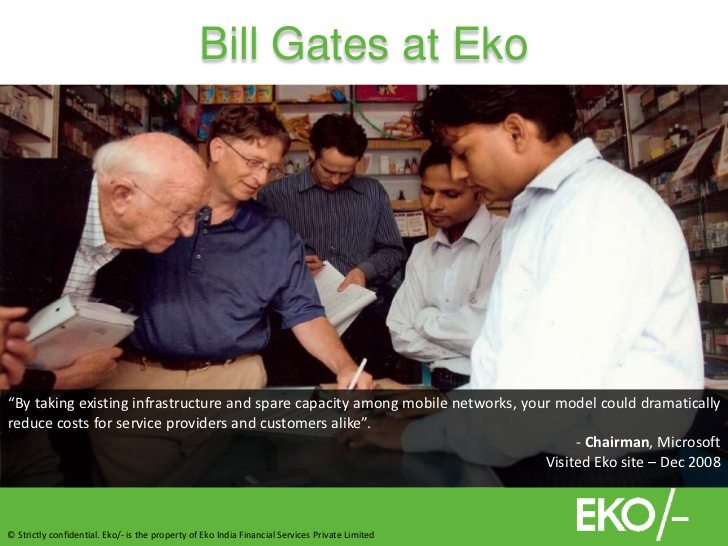

In its journey till date, Eko’s efforts towards financial inclusion for all has not gone unnoticed. Bill Gates himself visited Eko’s Uttam Nagar, New Delhi-situated mobile banking project, in November 2008. Thus, in 2009, it received a grant of $1.78 Mn from CGAP Technology Program which is housed within the World Bank and co-funded by the Bill & Melinda Gates Foundation.

In 2011, came its first round of institutional funding wherein it raised $5.5 Mn led by Chicago-based Creation Investments Social Ventures Fund I. Other investors like Promus Equity Partners and a consortium of high net-worth individuals (HNIs) also participated in the round.

The Digital Payments Party In India

With one of the largest unbanked population in the world, India is an exciting market for non-banking financial services. And with recent efforts being made to enable the right kind of environment, policy, and infrastructure, a lot is happening in the sector.

One of the biggest players Paytm, which has also received a payment bank license last year, is expected to raise another $60 Mn from Taiwanese semiconductor maker MediaTek. It has already crossed 80 million digital wallets users in India doing over 60 Mn transactions a month and has clocked a gross merchandise value run rate of $1.5 Bn in the last 15 months.

Snapdeal-owned Freecharge, Mobikwik, Citrus Pay, and Oxigen also have their own independent wallets. In a bid to mark its presence in the digital wallet services, even Amazon India has applied for a semi-closed wallet license with the Reserve Bank of India.

But Abhinav is not bothered by inherent competition. He says,

“I don’t think in a country like India one or two players can satisfy the needs of this country. If you look at the telecom industry also, there are many players in the space, though, of course, only three to four players get the bulk of market share and customers. Similarly even the payments space in India will have three to five really big players who will satisfy the needs of the payment industry and not just one big player.”

More so, how Eko looks at its target segment is slightly different as compared to other wallet players.

Eko largely caters to the urban, economically active customer segment earning between INR 10K-INR 50K in cash on a monthly basis. Adds Abhinav, “This segment basically earns in cash and spends in cash. These are urban customers such as cab drivers, security guards, working in beauty parlours, and restaurants, and they are savvy with tech, aware of things that are happening. Now if you if you look at the popular e-wallets, a cash earning-customer cannot use them as they can be funded only by credit cards and debit cards.

“So the customer segment that we are looking at is very huge in India, almost 80%. Hence we are creating a large network where customers can walk in our stores, get themselves an Eko wallet, and fund it with cash. Plus our transaction time is a mere 30 seconds,” he adds.

The full digitalisation drive of the government will further help Eko basis the fact that its target audience will continue to earn in cash and hence, will need options to convert that cash to digital money for various purposes. The concept of digitalisation is making customers socially digital, and Eko wants to make them financially digital. Therefore it is fully leveraging platforms and infrastructure including Aadhaar, NPCI, smartphones and riding on the digital wave.

Editor’s Note

In order to accelerate the evolution of a successful and economically viable payments process in India, the focus should be on building simplified products for users and addressing true customer needs.

In this regard, Eko scores in its simple and secure approach to provide digital inclusion to the unbanked. Eko is bridging the gap between traditional banking infrastructure and people who do not have access to banking.

In its endeavour to make spending from wallet a regular habit of its targetted audience, it should be able to leverage further growth and scalability. Yet research has shown that one out of two non-users haven’t used digital payments because they found the product too complicated to understand and 61% of non-user merchants find it too complex to use.

For a country that looks poised to skip the plastic generation and jump to mobile faster than any nation, this shows that there is still a vast expanse waiting to be tapped. And Eko has probably touched just the tip of the iceberg.