SUMMARY

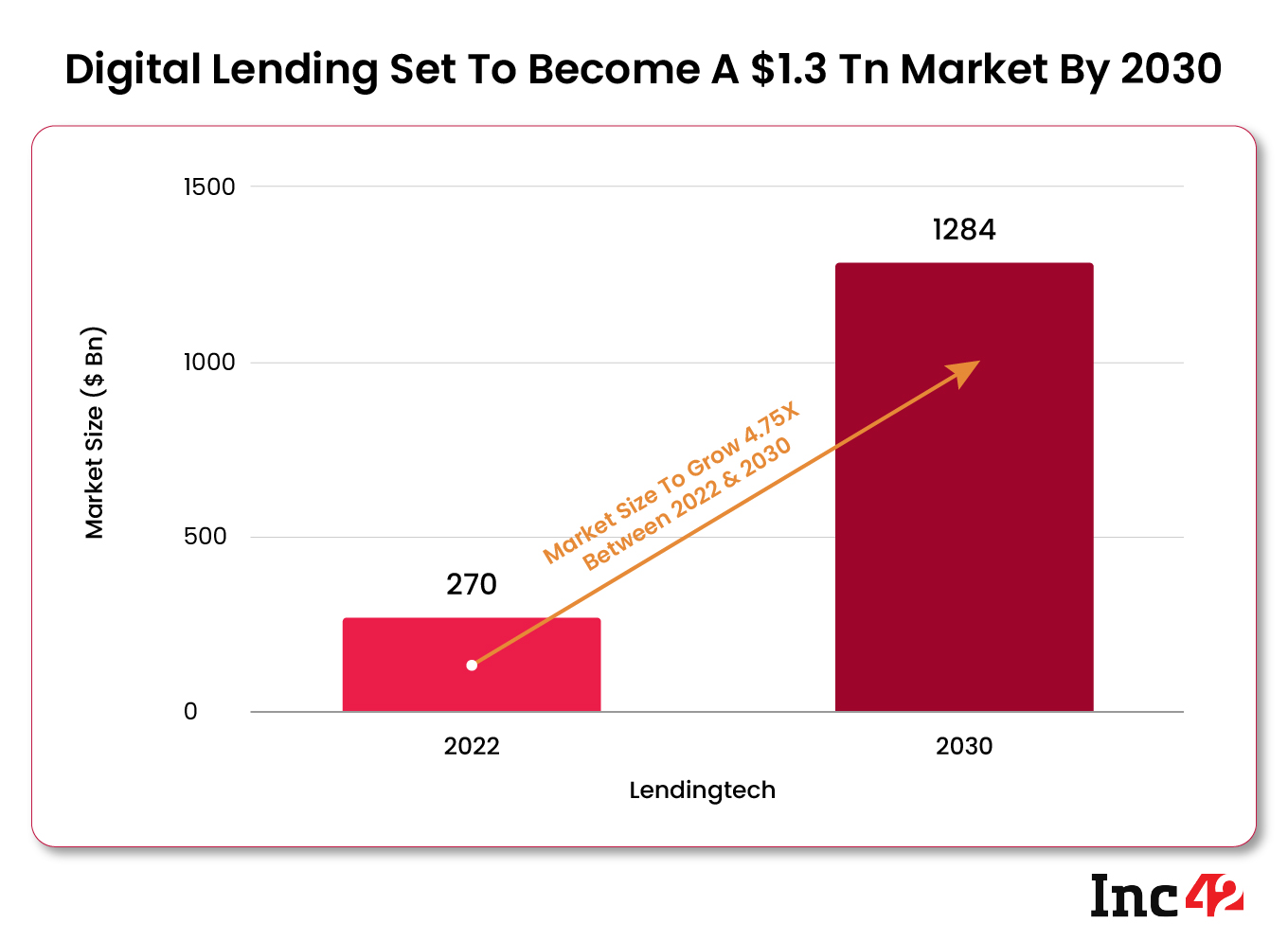

The digital lending market size is set to grow 4.75X to $1.3 Tn in 2030 from $270 Bn in 2022

Digital lending is set to account for 60% of the total Indian fintech market by 2030

Between 2014 and Q2 2022, digital lending startups raised $6.49 Bn in funding across 447 deals, accounting for about 28% of all fintech funding

Digital lending in India is expected to become a $1.3 Tn market opportunity by 2030. The digital lending market size is set to grow from $270 Bn in 2022 at a CAGR of 22% between 2022 and 2030, as per Inc42’s latest report ‘State Of Indian Fintech Ecosystem Q3 2022. InFocus: Neobanks’.

In essence, the total digital lending market is set to increase by almost 5X, driven by many favourable socioeconomic factors throughout the decade.

Data analysis indicates that digital lending is set to account for 60% of the total Indian fintech market by 2030. The increase in the proliferation of formal finance, growing per capita income and greater internet penetration, among others, will drive the growth in digital lending.

Moreover, the fintech segment is set to be on a steep growth trajectory in the coming decade. It is expected to take over major sectors such as enterprisetech, edtech and consumer services in terms of the number of soonicorns.

Overall, the fintech sector currently has 33 soonicorns, of which 39% are from the digital lending segment. The digital lending segment also counts two unicorns – Yubi (formerly CredAvenue) and Oxyzo.

Digital Lending In India: Funding Trends

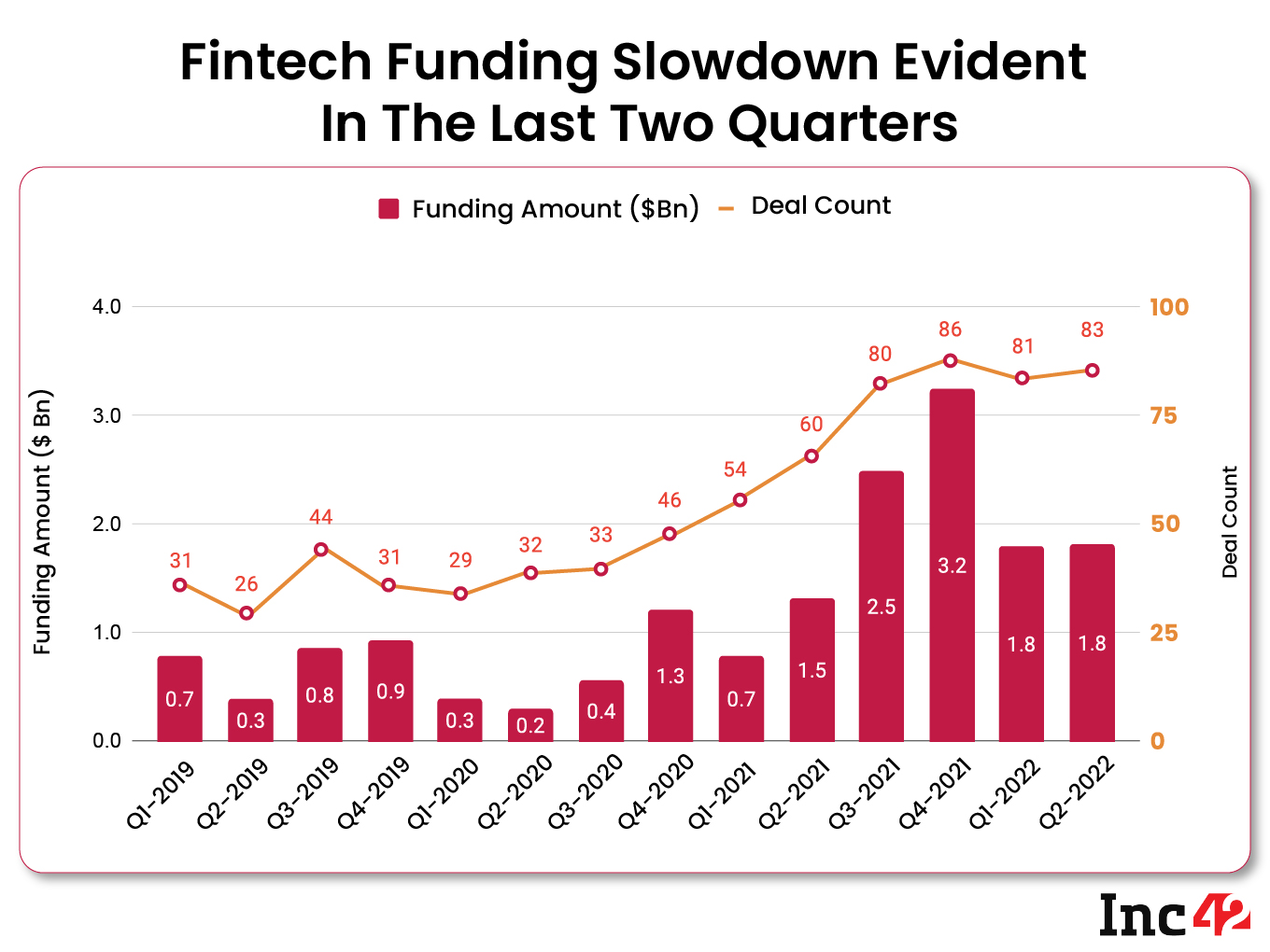

Funding amount and number of deals: Between 2014 and Q2 2022, the overall fintech ecosystem raked in $6.49 Bn funding across 447 deals.

Fintech Funding in Q2: The digital lending segment saw the highest fund inflow during Q2 2022 (April-June), securing $902 Mn across 28 deals. It accounted for 50.6% of the funding inflow in the fintech sector and 33% of the funding deals during the quarter.

Deal Spread Turns Minimal: Digital lending startups made up half of the top 10 fintech funding deals in Q2 2022, securing $340 Mn across five deals. The digital lending startups raised more than a third of the total funding through only 17% of the deals.

Fintech Undergoing Correction In 2022

With a funding slowdown being experienced by other sectors, the writing is on the wall for a correction in the fintech segment as well.

After a watershed year in 2021, which saw fintech startups raising $8 Bn across 280 deals, the funding momentum has slowed down. During the first three months of 2022, fintech funding fell by 44% and remained flat in Q2 2022.

The number of funding deals remained almost constant during Q4 2021 and the first two quarters of 2022, representing a fall in average ticket size in the sector. Besides the negative investor sentiment globally, a rapid change in the regulatory landscape within India’s fintech ecosystem is also behind the decline in funding.

Changing Digital Lending Regulatory Landscape

In June, the Reserve Bank of India (RBI) banned fintech companies without a banking licence from loading credit lines into their prepaid payment instruments (PPIs), sending a shockwave across the digital lending ecosystem.

The move resulted in many companies such as slice, One Card, Jupiter and Kreditbee changing their business models to comply with the new regulations.

To further boost the United Payments Interface (UPI), the National Payments Corporation of India (NPCI) is working to link credit cards with the real-time payment system.

The process is currently in its pilot phase, with RuPay Credit Cards being linked with UPI first. It is likely to include a 2% merchant discount rate, opening the avenues for the much-needed monetisation from UPI.

Last month, the RBI issued digital lending guidelines based on the recommendations of a working group to mitigate the concerns surrounding the lending ecosystem.

These concerns include engagement of third parties, misselling, data privacy breaches, unfair business conduct, high interest rates and unethical recovery practices. The digital lending guidelines were, therefore, issued to protect borrowers.

The fintechs and NBFCs have till November 30 to comply with the new guidelines.

Fake Digital Lending Apps And How Govt Is Tackling Them

The investigation by the Enforcement Directorate (ED) of the illegal lending apps has revealed the modus operandi of these apps.

According to the agency, the fake lending apps form a partnership with defunct non-banking financial companies (NBFCs) to obtain the NBFC licence required to start a digital lending business. The NBFCs are also used to create virtual merchant IDs with payment aggregators to help these apps send and receive money.

The apps acquire customers and issue high-interest loans, coupled with exorbitant processing fees. Most of these fraudulent apps are also known to illegally access personal data such as contacts. During recovery, these apps threaten public humiliation if the borrower fails to return the money, which has already resulted in several suicides.

Lastly, the proceeds of crime are remitted out of India, usually to the owners of these apps based primarily in China or Hong Kong via cryptocurrencies.

The ED recently conducted searches at payment aggregators, seizing money belonging to these fake digital lending apps. The financial crimes agency is also looking at all the crypto exchanges working in India to trace the proceeds of crime.

Recently, Finance Minister Nirmala Sitharaman chaired a high-level interdepartmental meeting to discuss the increasing threat of fake apps. Following the meeting, the RBI was asked to build a ‘whitelist’ of digital lending apps and the Ministry of Electronics and IT (MeitY) was asked to ensure only the whitelisted apps are available for download.

The Future Of Digital Lending

The reason why digital lending is the biggest opportunity within India’s fintech landscape is simple – low penetration of formal finance. Credit card proliferation in the country currently stands at just around 5.5%, as per the RBI. However, the demand for credit has never been higher in the country.

At Inc42’s Fintech Summit 2022, Zerodha founder and CEO Nithin Kamath said that if there is someone to underwrite the risk, lending is the largest fintech opportunity in the country.

The move to link UPI with credit cards is also expected to increase the general appeal of having a credit card, which might push up its usage in the country.

Digital lenders are also using new technologies to streamline and digitise the whole workflow. According to Vinay Bansal, founder & CEO of Inflection Point Ventures, “Lending concepts have become more sophisticated as a result of technological advancements and changing customer requirements.”

One of the innovations in digital lending is peer-to-peer (P2P) lending which matches borrowers with potential lenders with little to no intervention by a financial institution, Bansal said.

He added that the low interest rates and easy funding process has made P2P funding a popular investor choice.

The government has also introduced the Account Aggregator (AA) system, which is also set to streamline workflows for fintechs and NBFCs. Echoing the same, Infosys Chairman Nandan Nilekani recently said, “When the AA system is applied to credit and lending, it will make lending as simple as making a payment.”

While maximising the potential of digital lending would involve navigating through the ever-changing regulatory landscape, there is no doubt that there is enough demand to achieve scale rapidly.

“Digital lending will only continue to grow in the coming years as fintech revolutionises industries,” Bansal said. “Digital lending startups are taking advantage of opportunities to expand their activities, and have a better reach to types of clients, both, in terms of funding and product offered,” he added.